.webp)

While corporate credit cards offer convenience and efficiency for businesses, managing them effectively can be a daunting task. Without proper oversight, corporate cards can lead to uncontrolled spending, fraudulent activities, and administrative headaches.

To help you out, we’ve crafted this guide to delve into the nitty-gritty of efficient corporate credit card management, explore some best practices, and provide you with insights on how to choose the right card issuer.

By the end of this guide, you’ll have a better idea of how you can optimize your company’s spending, enhance financial control, and regain some of that lost sanity.

What is Corporate Credit Card Management?

Corporate credit card management is the systematic process of managing and controlling the use of company-issued credit cards. It involves setting clear spending policies, monitoring card usage, reconciling statements, and ensuring compliance with financial regulations.

Effective management is crucial for maintaining financial health, optimizing cash flow, and preventing fraud.

Why is Corporate Credit Card Management Important?

Eliminating the "Data Detective" Work

For most finance teams, the end of the month isn't about strategy; it's about forensics. You spend days matching blurry receipts to line items on a bank statement, only to realize half are missing. Effective management turns this "Data Detective" work into an automated process, freeing your team for high-value analysis.

Preventing "Maverick Spend"

"Maverick spend" happens when employees purchase items outside of company policy—either by accident or intentionally. Without real-time oversight, you only discover these unauthorized charges when the bill arrives 30 days later. Real-time management lets you spot and stop these leaks as they happen.

Protecting the Company’s Credit & Capital

Your corporate card program is a direct reflection of your company's creditworthiness. Poor management can lead to late fees, maxed-out limits, and a damaged relationship with your bank. Proper oversight ensures you stay within your capital limits while maximizing the benefits of your credit line.

Also read:

10 Ways to Master Corporate Credit Card Management

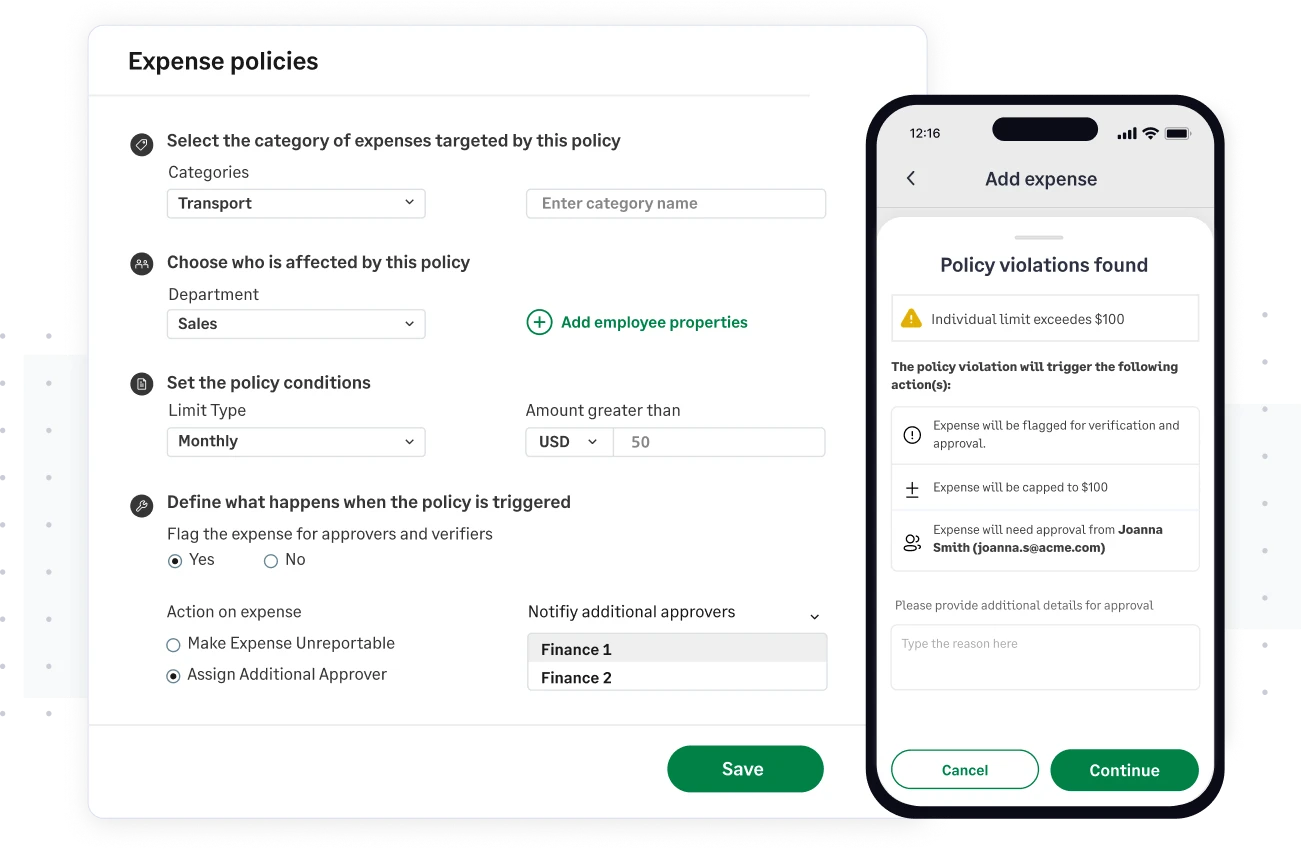

Establish Clear Spending Policies

Define what expenses are eligible for corporate cards, set spending limits, and outline approval processes. A well-documented policy serves as the ultimate "source of truth," leaving no room for ambiguity when an employee is about to swipe at a vendor.

Choose the Right Card Issuer

The ideal issuer should offer a balance of high credit limits, low interest rates, and a reliable customer service team that understands your business's specific needs. (More on why your local bank might be your best bet below).

Implement a Corporate Credit Card Expense Management Software

Utilize a credit card expense management software to automate expense tracking, track company card spending, and generate detailed reports. By choosing a platform that syncs directly with your existing bank cards, you eliminate the friction of manual data entry and ensure every transaction is accounted for.

Regularly Review and Update Policies

As your business evolves, revisit spending policies to ensure they remain relevant and effective. What worked for a small team of five may not be sufficient as you scale, making quarterly or bi-annual reviews essential to keep your controls tight.

Provide Comprehensive Employee Training

Educate employees about card usage, expense reporting procedures, and fraud prevention. Training shouldn't be a one-time event; instead, provide regular refreshers and clear documentation so every cardholder knows exactly how to handle a missing receipt or a suspicious charge.

Set Up Spending Alerts

Monitor card activity in real time and receive notifications for unusual or suspicious transactions. These instant notifications allow the finance team to act immediately on potential "maverick spend" or fraud rather than waiting for the end-of-month statement.

Reconcile Statements Promptly

Review and reconcile credit card statements to identify errors, unauthorized charges, and potential discrepancies. Prompt reconciliation ensures that your financial books are always accurate, making year-end tax preparation and internal reporting much less stressful.

Conduct Regular Audits

Perform regular audits to assess card usage, and compliance with policies, and identify areas for improvement. Beyond just spotting errors, audits help you identify spending patterns—like recurring subscriptions you no longer need—that can save the company significant money over time.

Leverage Rewards and Benefits

Maximize the value of your corporate card program by taking advantage of rewards and perks offered by the card issuer. Whether it’s cash back, airline miles, or lounge access, these benefits can significantly offset your travel costs and add a layer of value to your overhead expenses.

Foster a Culture of Accountability

Emphasize the importance of responsible card usage and encourage employees to report any issues promptly. When employees understand that corporate cards are a privilege and a shared responsibility, they are far more likely to adhere to policies and take ownership of their spending habits.

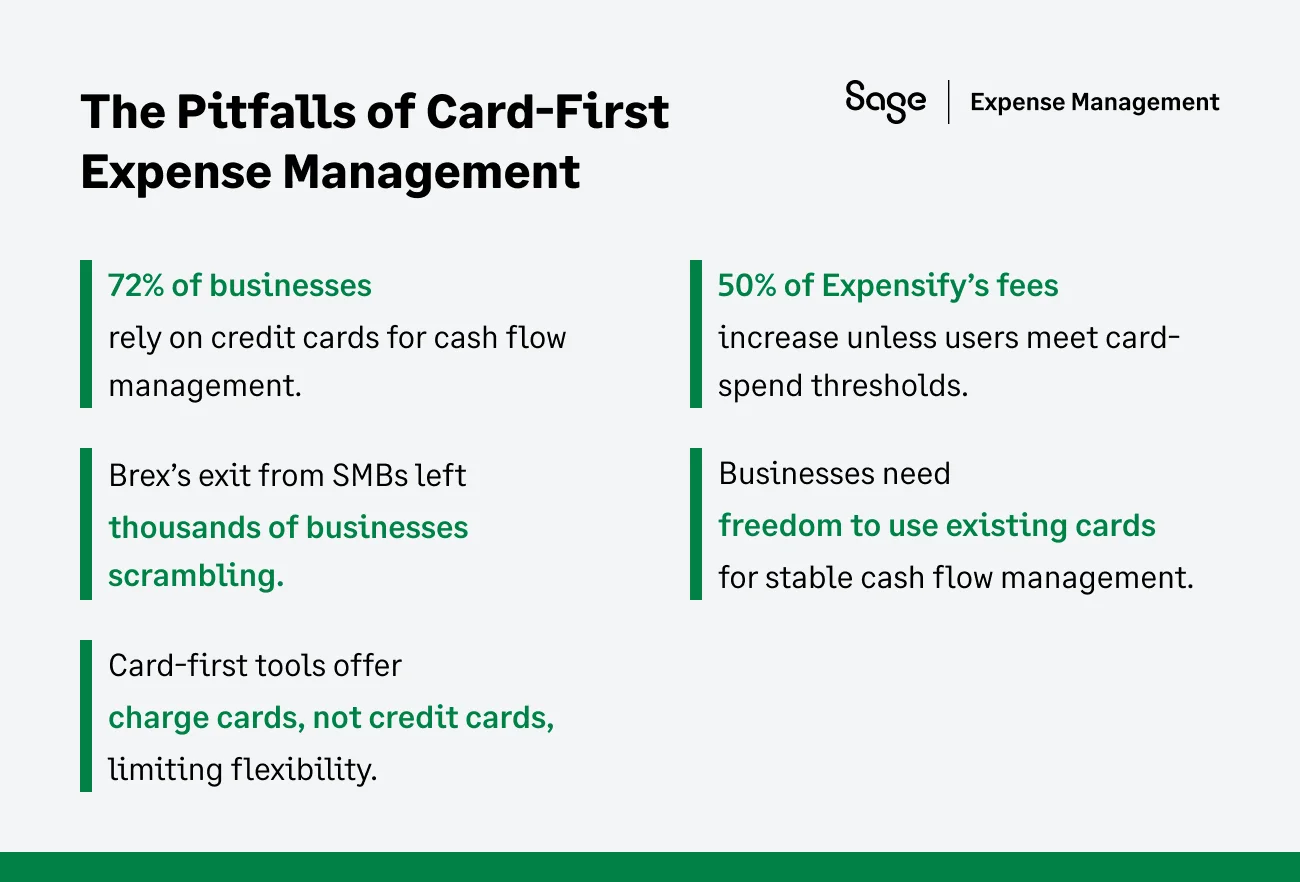

Bank-issued vs. Fintech-Based Corporate Credit Cards

Many modern businesses feel pressured to switch to "Fintech" cards (like Ramp or Brex) to get better software. However, for most SMBs, bank-issued cards are often the superior choice. Here’s why:

- The "fintech trap": Many fintech cards require a massive cash balance (often $75,000 to $250,000) just to qualify. If your cash flow dips, they can cut your limit overnight.

- The "bank advantage": Established banks offer higher credit limits based on your years of history, not just your current bank balance. They also offer lower interest rates and a broader range of financial products like term loans and lines of credit.

- Established trust: Banks are subject to more stringent regulations, offering a level of stability that venture-backed startups sometimes lack.

The bottom line: You shouldn't have to move your entire banking relationship just to get a good dashboard. With the right software, you can keep the bank cards you love and still get "fintech-level" control.

How to Manage Multiple Company Credit Cards?

While managing multiple corporate cards can be complex, here’s one of the easiest things you can do:

Centralize Corporate Credit Card Expense Management

Managing cards across different departments (like Sales, Marketing, and Ops) can lead to fragmented data. By centralizing your card management into one dashboard, you get a "God-view" of all spending. You can see who is swiping, where they are swiping, and if they’ve attached a receipt—all in one place.

Syncing with the Source of Truth

Your card data shouldn't live in a silo. It needs to flow directly into your accounting software (like QuickBooks, NetSuite, or Sage Intacct). Automated syncing ensures that every reconciled transaction is pushed to your general ledger with the correct GL codes, eliminating manual data entry.

Why Sage Expense Management (formerly Fyle) is the "Best of Both Worlds"

Sage Expense Management gives you the power of fintech software without making you change your bank.

- Keep your bank: We connect directly to your existing Visa, Mastercard, or Amex business cards.

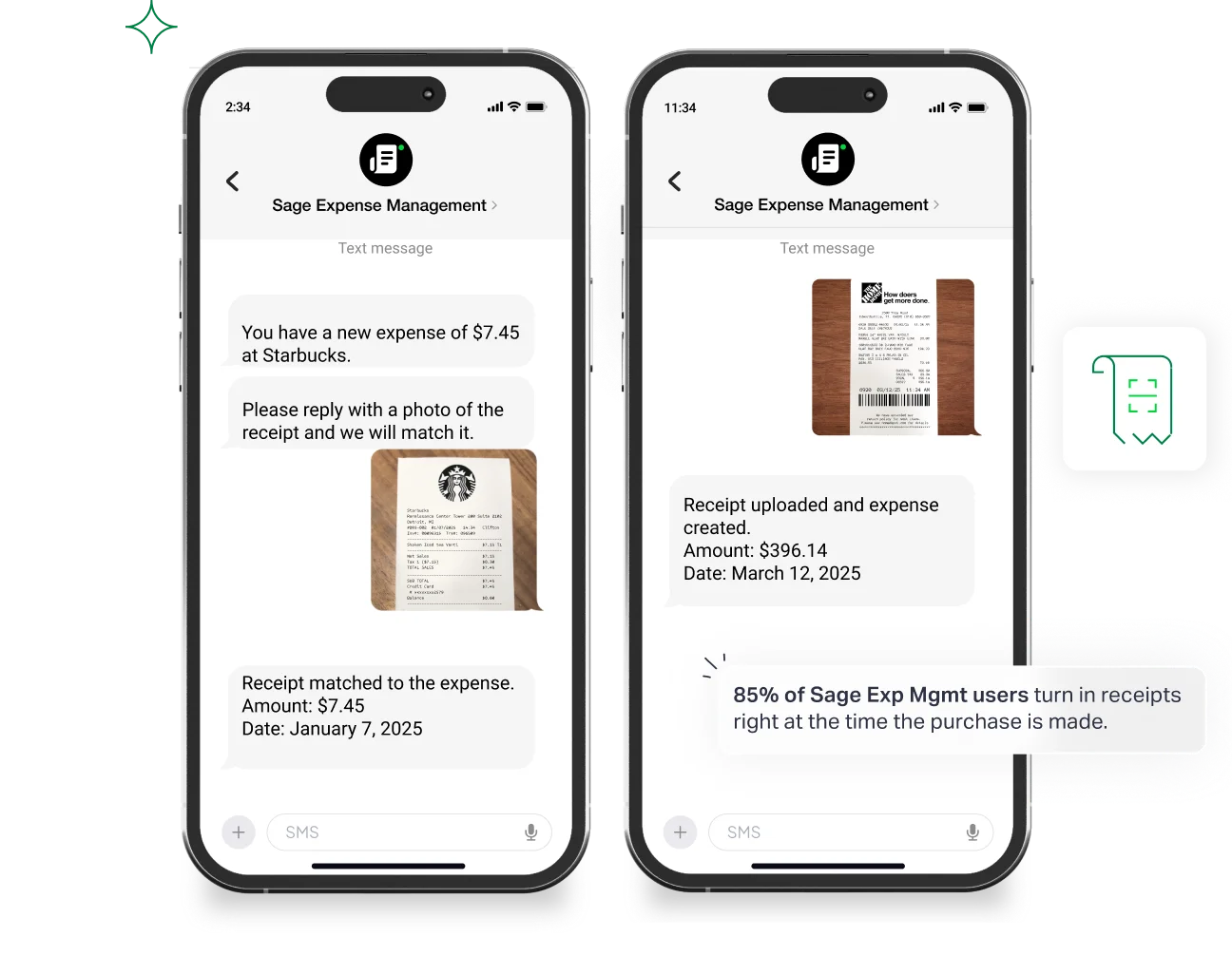

- Real-time visibility: Get an instant text notification the second a card is swiped—no more waiting 3 days for the bank feed to refresh.

- Text-to-submit receipts: Employees just reply to the text with a photo of the receipt. Our AI matches it to the transaction instantly.

- Automated compliance: Our policy engine flags out-of-policy spend before it reaches the finance team.

{{credit-card="/cta-banners"}}

FAQs Around Corporate Credit Card Management

How Do I Prevent Unauthorized Charges on a Corporate Credit Card?

Implementing robust security measures is crucial. This includes setting strong passwords, utilizing cardholder verification (CVV) codes, and enabling fraud alerts.

Regularly monitoring card activity and reporting suspicious transactions promptly can also help prevent unauthorized charges.

What Should I Do If I Find an Unauthorized Charge on my Corporate Credit Card?

Contact your card issuer immediately to dispute the charge. Gather all necessary documentation, such as receipts and transaction details. Work closely with your company's finance department to resolve the issue promptly.

How Can I Choose the Right Corporate Credit Card for My Business?

Consider factors such as annual fees, rewards programs, interest rates, and customer support when selecting a corporate credit card. Evaluate the card's alignment with your business's spending habits and industry-specific needs. Bank-issued cards often offer a wider range of features and benefits tailored to businesses of all sizes.

How Often Should I Reconcile Corporate Credit Card Statements?

Ideally, corporate credit card statements should be reconciled monthly to ensure accuracy and identify any discrepancies. However, for businesses with high transaction volumes, more frequent reconciliation may be necessary.

But with tools like Sage Expense Management, credit card transactions are automatically reconciled as soon as employee submit their receipts via text!

What are Some Common Corporate Credit Card Fraud Red Flags?

Common red flags include unauthorized charges, unusual purchase amounts, transactions in unfamiliar locations, and discrepancies between receipts and card statements. Be vigilant and report any suspicious activity immediately.

How Do I Handle Card Management for Employees Who Leave?

You should cancel the card the moment their termination is processed. Sage Expense Management can sync with your HR platform (like BambooHR or Rippling) to automatically flag or deactivate users when they leave the company.

Can I Issue Virtual Cards for One-Time Vendor Payments?

Absolutely. Virtual cards are a best practice for managing SaaS subscriptions or one-time vendor payments. They allow you to set a specific limit for one vendor, ensuring they can't overcharge you or compromise your main credit line.

Does Switching to a Credit Card Expense Management Platform Mean I Have to Change My Bank?

With Sage Expense Management, the answer is an emphatic No. We work with your existing cards, so you keep your rewards, your credit line, and your bank relationship intact.