They say an accountant’s job is never done, and for many, the monthly ritual of the month-end close process is a prime example. This critical task is far more than just crunching numbers—it’s about ensuring the financial health of the entire business.

A month-end close can be a stressful, time-consuming race against the clock, with accountants navigating a river of invoices, expense reports, and receipts. But it doesn't have to be. By understanding the core steps and adopting a few key strategies, you can transform this chaotic monthly grind into a disciplined, efficient, and even routine process.

This guide is your master resource for conquering the month-end close. We'll demystify the process, provide a comprehensive checklist, and share actionable tips to help you save time, reduce errors, and reclaim control of your financial operations.

What Is A Month-End Close?

The name is fairly self-explanatory: at the end of each month, accountants meticulously review all financial activity—money in, money out, and everything in between. The primary goal is to ensure your financial records are accurate, consistent, and fully substantiated.

While the specifics of the process can vary widely between businesses, the core objective is universal: to create a clear, comprehensive snapshot of your company’s financial health for a specific period. This sets the stage for accurate reporting, smarter decision-making, and a smoother annual close.

A streamlined month-end close is a sign of a healthy, disciplined finance department. It’s about more than just numbers; it’s about a rhythm that keeps your business running smoothly.

What Are The Steps In The Month-End Close Process?

A company’s month-end close can get pretty granular, but it always revolves around a predictable, sequential set of tasks. Here are the core elements you’ll need to hit upon every month:

- Collect data and documents: Gather all invoices, expense reports, receipts, bank statements, and other financial records from the past month. The more complete this is from the start, the faster the close.

- Combine the parts of accounting: Integrate all financial information from different sources into one central system or ledger.

- Reconcile data against records: Meticulously compare bank statements, general ledgers, and other accounts to identify and resolve any discrepancies.

- Examine inventory and fixed assets: Review inventory levels, account for any spoilage or breakage, and track the estimated depreciation of fixed assets. This ensures your balance sheet is accurate.

- Consult with team members: Reach out to sales, HR, operations, or other departments to gather any missing information, like final sales figures or outstanding invoices.

- Draft financial statements: Create key financial reports, including the income statement (profit and loss), balance sheet, and statement of cash flows.

- Review statements with the team: Double-check all drafted statements for accuracy, catching any errors before they are finalized.

- Prepare for the next closing: Use insights from the current month to refine the process for the future, making the next close even more efficient.

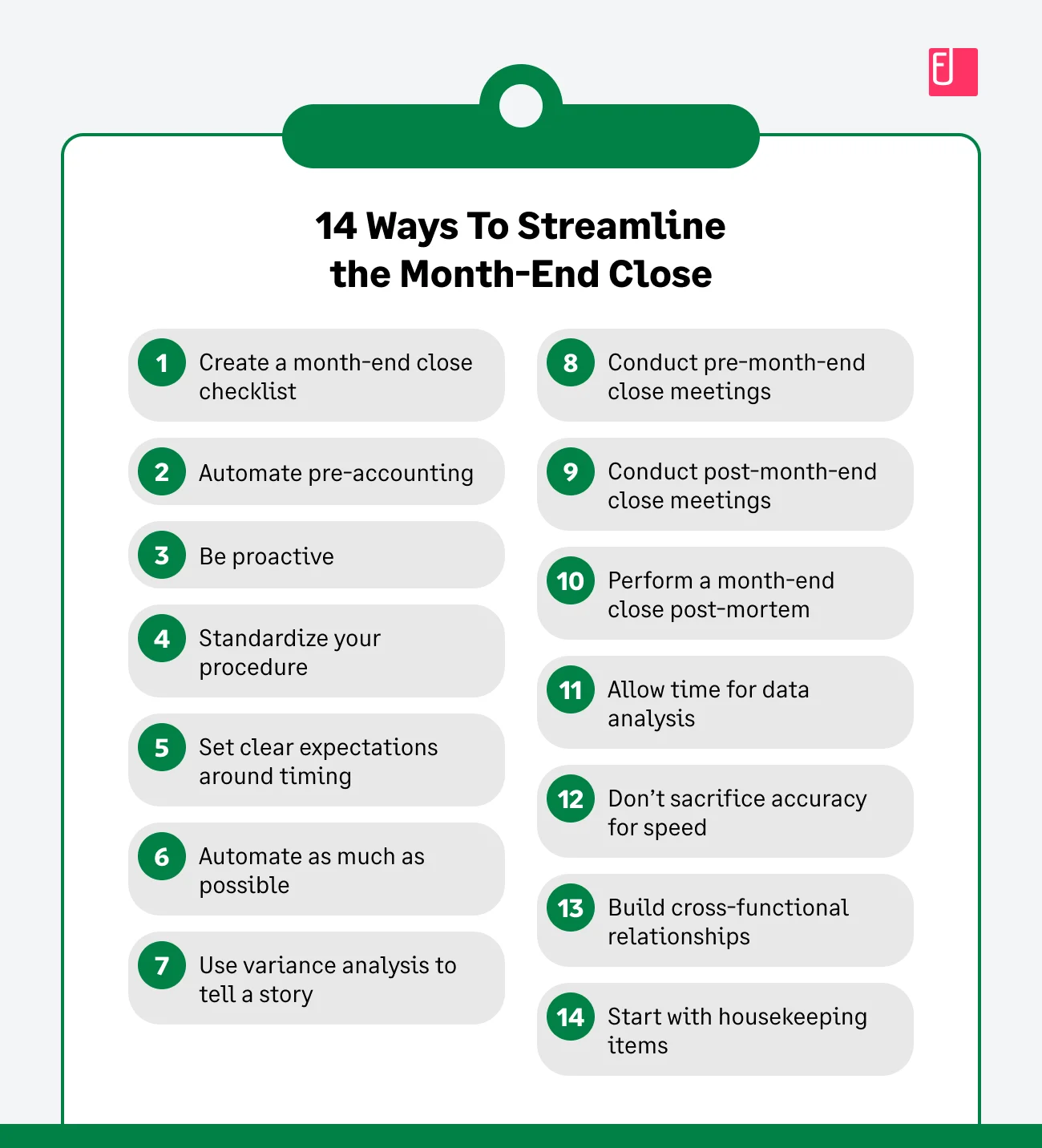

14+ Accountant-Approved Tips to Streamline Your Month-End Close

The month-end close is more than a checklist; it's a rhythm. The more proactive and collaborative you are, the smoother it gets. Here are some of the best practices that can help you reclaim days from your close process.

Before and During the Month-End Close

- Create a month-end close checklist: A checklist is your greatest ally. It standardizes your procedure, ensuring no task is forgotten and that the process is repeatable and efficient.

- Automate pre-accounting: Don’t wait until the last minute. Automate tasks like expense reporting and receipt collection throughout the month. This ensures you have all the necessary documents ready to go on day one of the close.

- Be proactive! Adopt a forward-thinking mentality. Instead of letting the close sneak up on you, be organized in advance by chasing up receipts and double-checking manual work during the month to eliminate human error.

- Standardize your procedures: Inconsistent documentation can be a real headache. Set clear procedures for managing expenses, invoicing, and data entry. This reduces inconsistencies and prevents accidental duplicate documents from slipping through the cracks.

- Set clear expectations around timing: Everyone involved needs to know their role and the deadlines. Setting clear expectations for your team prevents confusion and delays.

- Automate as much as possible: The less manual work you do, the faster the close. Look for opportunities to automate repetitive tasks like journal entries, reconciliations, and expense reporting.

- Use variance analysis to tell a story: Once the books are closed, compare actual performance against your budget or forecast. This helps you identify trends, explain variances, and provide leadership with a clear story of the month’s performance.

- Conduct pre-month-end close meetings: Hold a brief meeting a few days before the end of the month to confirm everyone is on track and has everything they need.

After the Month-End Close

- Conduct post-month-end close meetings: This is where the real learning happens. Use these meetings to identify bottlenecks, discuss what went well, and develop strategies to improve the timeline for the next month.

- Perform a month-end close post-mortem: Analyze where delays occurred. Was it waiting for a specific report? A complex reconciliation? This helps you pinpoint weak spots and find solutions.

- Allow time for data analysis: Once the books are closed, your job isn't done. Use the clean data to conduct in-depth analysis, providing strategic insights to your leadership team.

- Don’t sacrifice accuracy for speed: Standardizing your close process isn't just about speed; it’s about reducing risk. A repeatable checklist and clear procedures help your team catch errors before they become a bigger problem.

- Build cross-functional relationships: The month-end close isn’t just a finance task. Partner with operations, IT, and HR to ensure data flows smoothly across the entire organization.

- Start with housekeeping items: Once the month begins, clear out old tasks. Reconcile bank accounts, chase overdue invoices, and get a head start on preparing for the next close.

Month-End Close Checklist: Key Areas to Cover

A comprehensive checklist is the backbone of an efficient month-end close. Here's a breakdown of the key areas to cover every month:

1. Cash & Bank Reconciliation

This is typically the first and most critical step. It involves comparing your company's internal cash records (the General Ledger) with the bank's records (bank statements).

- What to do: Meticulously reconcile all bank accounts, credit card statements, and any petty cash funds. This process verifies that every transaction—from a wire transfer to a small employee expense—has been accurately recorded.

- Why it matters: It helps you identify and resolve discrepancies, such as uncashed checks, bank errors, or fraudulent activity, ensuring your cash balance is accurate. You should also adjust for any outstanding transactions that have been recorded in your books but have not yet cleared the bank.

2. Revenue & Receivables

This step focuses on all the money owed to your company.

- What to do: Record all income that was earned during the month. Review your accounts receivable aging reports to identify which customers owe you money and for how long. Actively chase up any outstanding invoices to improve cash flow.

- Why it matters: It ensures your revenue is accurately recognized according to accounting principles. By keeping a close eye on receivables, you can also manage your cash flow more effectively and identify potential issues with customer payments.

3. Expenses & Payables

This section is dedicated to all the money your company owes to others.

- What to do: Record and reconcile all expenses and vendor bills. This includes reviewing expense reports submitted by employees and ensuring all vendor invoices have been processed correctly. Review your accounts payable aging reports to manage your cash outflows and resolve any discrepancies.

- Why it matters: Accurate tracking of expenses and payables is vital for creating an accurate income statement and balance sheet. It ensures you have a true picture of your company's short-term financial obligations and helps you manage relationships with vendors and suppliers.

4. Accruals & Liabilities

This step is for expenses and income that have been incurred but for which no invoice or payment has been made yet.

- What to do: Accrue for expenses like payroll (if the pay period ends after the month's close), taxes, loan interest, and any significant unpaid vendor expenses. Conversely, record any accrued revenue for work completed but not yet billed.

- Why it matters: Accruals are essential for adhering to the accrual basis of accounting, which requires you to recognize revenue and expenses when they are earned or incurred, not when the cash is exchanged. This provides a more accurate view of your company's profitability for the period.

5. Assets & Inventory

This involves updating the value of your company's long-term and short-term physical assets.

- What to do: Update depreciation and amortization schedules for all your fixed assets (e.g., equipment, vehicles). Reconcile inventory counts and values to ensure your records match the physical stock, accounting for any spoilage or breakage.

- Why it matters: This ensures your balance sheet reflects the true value of your assets. Accurate inventory and fixed asset data is critical for cost of goods sold calculations, profitability analysis, and making informed decisions about future investments.

6. Intercompany & Prepaids

This is particularly important for businesses with multiple legal entities or subsidiaries.

- What to do: Match intercompany transactions to ensure that all financial activity between related entities is properly reconciled. Eliminate any duplicate entries that might have occurred during data transfer. Also, review and amortize any prepaid expenses (e.g., insurance premiums, rent) that were paid in advance.

- Why it matters: Proper intercompany reconciliation is crucial for accurate consolidated financial statements. It prevents the overstatement or understatement of assets, liabilities, and equity, giving you a clean, reliable picture of the parent company's finances.

7. Payroll

This is a critical, and often sensitive, part of the close process.

- What to do: Record all employee compensation, bonuses, and reimbursements for the period. This includes ensuring all deductions for taxes and benefits are accurately captured.

- Why it matters: It ensures that your income statement accurately reflects the company's labor costs and that all employee-related liabilities are correctly stated on the balance sheet. It is also essential for compliance and maintaining accurate records for both the business and its employees.

8. Reporting & Review

This is the final, executive-level stage of the close.

- What to do: Reconcile all balance sheet accounts to ensure everything balances. Prepare the final versions of your key financial statements: the income statement, balance sheet, and statement of cash flows. Maintain a close schedule or dashboard to track the progress of each of these tasks.

- Why it matters: This step produces the final, authoritative financial reports that are used by leadership for decision-making. It is the culmination of all the work done throughout the month and serves as the official financial record for the period.

Why The Month-End Close Matters

For any company accountant, the month-end close process is a simple fact of life. To keep everything clear, you’ve got to wade through a river of invoices, wage slips, and employee receipts. But why is it so important?

It Ensures Your Records Are Accurate And Up-To-Date

One of an accountant’s main responsibilities is to monitor the business's financial stability. Without them, you’ll be stuck guessing. And even small errors or inconsistencies will cause your assessments to become less accurate over time.

And, as noted, it’s about avoiding legal issues. But not just for the business. Remember that accountants can be held liable for negligence, even if they aren’t directly responsible. So, it’s about keeping yourself covered too.

It Helps Organize Tax Returns And Your Annual Close

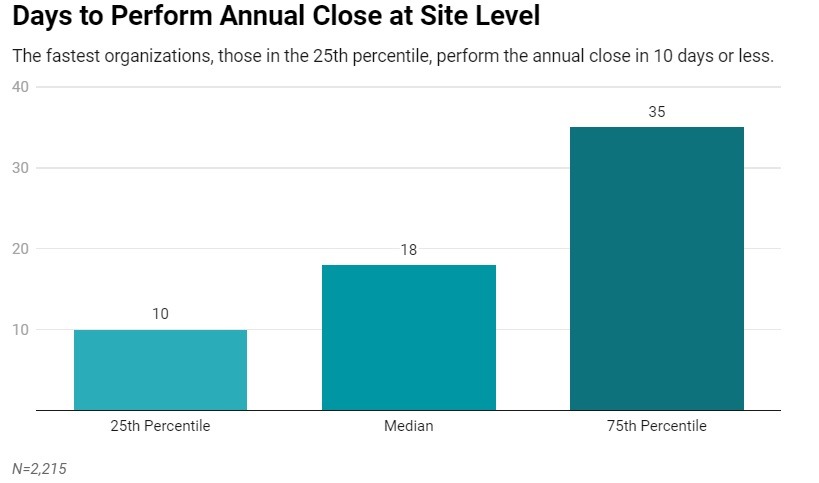

According to APQC findings, the median year-end close time for businesses is 18 days. Those in the 75th percentile took over a month (35 days) to complete it. Only those in the 25th percentile could complete it in 10 days or less.

In other words, it’s a very drawn-out, time-consuming process. On top of that, you’ve got things like tax returns and all the other end-of-year loose ends to tie up. However, an accurate month-end close process can help to expedite things.

A Monthly Opportunity To Evaluate Areas Of Improvement

Your month-end close is also a great opportunity for organizational self-reflection. Financial efficiency, after all, is another of an accountant’s responsibilities. Going through the paperwork every month may be dull. But it’ll help you identify problem areas, like unnecessary expenditure, wastage of utilities (gas, electricity, internet, etc.), or inventory.

What Information Does Accounting Need for Month-End Close?

Accountants typically need the following info for the month-end close:

- Sales figures: How much money came in?

- Bank details: What's the cash situation?

- Inventory count (if relevant): How much stock is on hand?

- Petty cash sum: How much small-dollar spending happened?

- Financial reports: The overall financial picture.

- Balance sheets: What's the company's worth at this point?

- Value of fixed assets: How much are long-term investments worth?

- Income and expense details: Where did money come from and go?

- General ledger: The master record of all financial transactions.

How Long Does the Month-End Close Process Typically Take?

The average month-end close process typically takes between 5-10 days.

The time it takes to complete the process will depend on several factors, including the size of the company, the volume and complexity of transactions that need to be recorded and reconciled, and the accounting systems used.

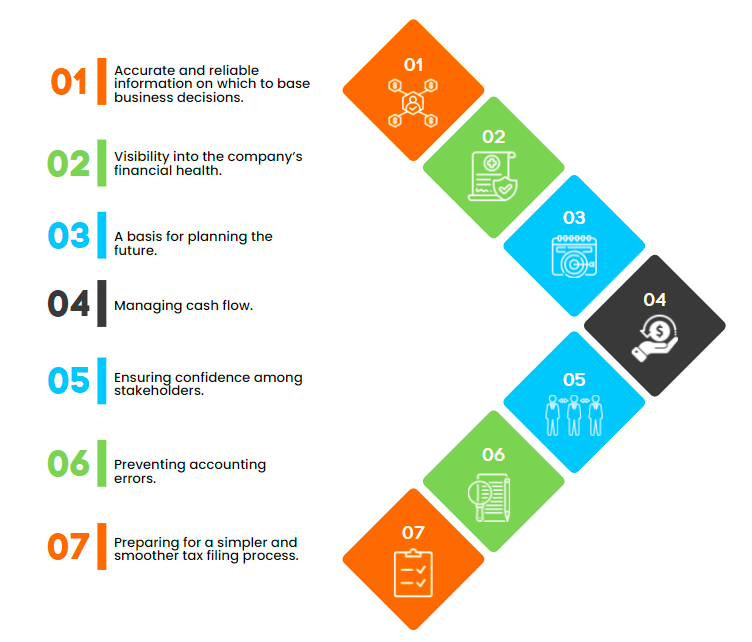

Why Is It Important to Optimize the Month-End Close?

Optimizing the month-end close is important for several reasons, including:

- Getting financial numbers into the hands of leadership sooner can help them make better decisions about the business.

- Better discipline and more structure can help ensure that the process is completed accurately and efficiently.

- Improved controls can help reduce the risk of errors and fraud.

- More visibility into the company's financial performance, which can help to identify areas for improvement.

- Reduced risk by ensuring that the financial statements are accurate and timely.

What Are Some Common Challenges in a Month-End Close Process?

Here are some of the most common challenges faced by businesses in the month-end close process:

Data-related challenges

- Inaccurate data: Manual data entry, missing information, and inconsistent formats can lead to errors in financial statements and audit issues.

- Lack of real-time data: Reliance on outdated or incomplete data hinders timely and accurate reporting.

- Discrepancies: Reconciling accounts between different departments or systems can be time-consuming and prone to errors.

Process-related challenges

- Manual processes: Repetitive tasks like journal entries, reconciliations, and reporting consume valuable time and resources.

- Lack of standardized procedures: Inconsistent workflows across teams and departments lead to confusion and delays.

- Limited visibility: Without clear communication and tracking, monitoring progress and identifying bottlenecks is difficult.

Resource-based challenges

- Time pressure: Tight deadlines put immense pressure on accounting teams, leading to stress and burnout.

- Global teams and time zones: Coordinating across different locations and time zones adds complexity to the process.

- Lack of training: Inadequate knowledge about specific tasks or systems can slow down the process and increase errors.

Technology hurdles

- Outdated software: Outdated systems lack automation, integrations, and real-time capabilities, hindering efficiency.

- System crashes and glitches: Technical issues during peak periods can cause significant delays and disruptions.

- Security concerns: Data security breaches can have severe financial and reputational consequences.

Tips For A Faster Month End Close

Before you go, we wanted to give you some parting advice. Your month-end close process might be able to save you some time in the long run. But even a monthly close can be time-consuming by itself. You’re looking at several days when accountants must focus on it over most other duties.

So, here are our tips for running your month-end close more efficiently.

Document And Back Up As You Go

Documentation is at its most inconvenient when you have to do it retroactively. And, sometimes, things get corrupted or accidentally deleted. So the best way to save yourself a headache is to incorporate a documentation and back-up process into your workflow.

The first thing you’ll need is a checklist. You’ll refer back to it as part of your month-end close process. But, in the meantime, it’ll ensure you don’t miss anything during the month.

Say you finish an expense report. You quickly check it off the list, save it, and then save it again (this time on the cloud). All that shouldn’t even take a minute. But it can save you hours of frustration down the line if things go wrong.

Standardize Your Procedure

People might go about managing their expenses in different ways. And you might think this isn’t an issue, so long as the information is set down. But this can be a real sleeper headache for accountants if left unchecked.

If people take different approaches to financial documentation, it leaves room for inconsistencies. A missing date here or different invoice numbering there. All this makes it easier for stuff to slip through the cracks. Or you might end up wasting time with accidental duplicate documents.

So, figure out the best accounting procedure for your company. Then communicate it clearly.

How Sage Expense Management (Formerly Fyle) Can Help Speed Up Your Month End Close

What’s the one thing you can do to ensure your month-end close is a breeze?

Automating your expense management with the Sage Expense Management platform. Why?

Because with us, you no longer have to chase your employees for receipts. Your receipts come to you. How?

Real-Time Purchase Alerts and Text Message Receipt Collection

Whether it's a credit card swipe or a reimbursement, you can snap a picture and text your receipts to us. We will automatically check for a matching card expense and instantly match it with the transaction.

Plus, we integrates with all major credit card networks, so you get real-time spend alerts right after their card is swiped. Employees just need to reply to this message with a picture of the receipt, and it’s automatically matched!

Accountants rejoice! Our platform speeds up your receipt collection by 5x, eliminating endless emails and reminders.

Our text-to-submit magic ensures you have complete, organized records at your fingertips making closing books a breeze.

There’s more!

Real-time Spend Visibility

Our CoPilot feature is a game-changer for accountants. See every employee's credit card expense in real-time, sliced and diced by category, merchant, project, employee, or department. No more digging through spreadsheets! This crystal-clear view empowers you to:

- Spot risks instantly: Identify suspicious activity before it becomes a problem.

- Boost efficiency: Pinpoint areas for cost optimization and streamline operations.

- Curb overspending: Proactively address potential budget breaches.

Our platform doesn't just save time; it equips you with the insights needed for a smoother, faster month-end close.

Making The Most Of Your Month-End Close

Ultimately, the key to a stress-free month-end close is to stop letting the process sneak up on you. By taking the time to get organized in advance, you can transform this monthly chore from a time-consuming headache into a streamlined and efficient process.

This is where the power of partnership comes in. Our innovative technology and Sensiba's deep accounting expertise work in tandem to give you a truly seamless solution.

While the Sage Expense Management platform automates the grunt work—like chasing receipts and reconciling accounts in real-time—Sensiba helps your business design a scalable, disciplined close process that's right for you. Together, we empower your team to spend less time worrying about paperwork and more time working constructively to help your business keep growing.