.webp)

Businesses generate significant expenses that can be challenging to track. If combined with poor bookkeeping, this can make running your business more complicated than needed. But there's another reason you need to organize your business expenses: figuring out your tax deductions.

To reap the benefits of business tax write-offs, you must account for all the business expenses incurred by your company. Then, you can deduct these expenses from your income, lowering your tax liability.

But where does one start?

This article covers everything you need to know about business expenses–categorizing them, which ones are tax-deductible, and why you need business expense categories.

In addition, it is a good starting point to understand how to organize your spending to maximize your tax deductions.

What Are Tax-Deductible Business Expenses?

A tax-deductible business expense is a cost incurred by your organization that can be subtracted from your total revenue to lower your taxable income. However, "spending money on the business" doesn't automatically qualify as a deduction. To satisfy the IRS, an expense must pass a specific three-part test: it must be ordinary, necessary, and reasonable.

- Ordinary expenses are those that are common and accepted in your specific trade or industry.

- Necessary expenses are those that are helpful and appropriate for your business to function.

- Reasonable expenses are those where the amount spent is not lavish or extravagant under the circumstances.

For example, a construction firm can deduct the cost of heavy machinery (ordinary) to complete a contract (necessary), provided they aren't paying five times the market rate for that rental (reasonable).

Distinguishing Between COGS, CapEx, and Operating Expenses

The IRS requires you to distinguish between different types of costs because their impact on your tax return varies. Misclassifying these is a primary trigger for audit adjustments.

- Cost of Goods Sold (COGS): These are the direct costs of producing the products your business sells. This includes raw materials and the direct labor required to manufacture goods.

- Capital Expenditures (CapEx): These are investments in assets that provide value for more than one year, such as vehicles, machinery, or buildings. You generally cannot deduct the full cost of these in a single year; instead, you recover the cost over time through depreciation or amortization.

- Operating Expenses (OpEx): These are the day-to-day costs of keeping the business running that are not directly tied to production, such as rent, utilities, and marketing.

Common Examples of Deductible Expenses

- Salaries and wages paid to employees for services actually performed.

- Rent or lease payments for the commercial space where you conduct business.

- Utilities including electricity, water, and business-grade internet service.

- Depreciation on tangible assets like equipment and vehicles used for business purposes.

- Interest on business loans or lines of credit used to fund operations.

- Taxes and licenses such as state franchise taxes or professional permits.

Before you file, it is important to review IRS Publication 535, which details the general rules for business deductions. In 2026, many businesses are also utilizing the de minimis safe harbor election, which may allow you to deduct smaller asset purchases (typically under $2,500) immediately rather than capitalizing them.

What Are Business Expense Categories?

Business expense categories are a structured taxonomy used to classify every dollar leaving your firm. They serve as the mapping system for your Chart of Accounts, ensuring that a software subscription doesn't get lost in a generic "miscellaneous" bucket. By assigning a specific label to each transaction, you transform raw bank data into actionable financial intelligence.

In a sophisticated environment, like the framework used at Harvard, these categories are often linked to specific "Object Codes." For example, a "Security Deposit" is coded differently (Object Code 0550) than "Rent" (Object Code 7230) because one is a refundable asset and the other is a consumed expense.

Why Do You Need Business Expense Categories?

The IRS defines business expenses simply as "the costs of carrying on a trade or business." However, for a Finance Director or Controller, these categories are the primary lever for maintaining the company's "economic reality."

Deduction Maximization and Tax Strategy

Categorization is your first line of defense during an audit. The IRS requires you to prove that an expense is "ordinary and necessary" for your industry. Without clear categories, you risk missing out on significant write-offs—such as the 100% deduction for employee holiday parties versus the 50% limit on standard business meals.

Strategic Spend Visibility

You cannot optimize what you cannot see. Properly categorized data allows you to:

- Identify spend leakage: Spot departments that are over-budget on "Software" or "Taxis" before the end of the quarter.

- Inform future bidding: Use historical "Job Costing" categories to ensure your next project quote is profitable.

- Document for stakeholders: Provide investors or lenders with a clean view of your burn rate and gross margins.

Audit Readiness and Documentation

IRS Publication 463 mandates "adequate records" for travel and gift expenses. Certain categories have higher bars for proof than others. For instance, while a meal under $75 may not require a receipt, every "Lodging" expense requires an itemized folio regardless of the cost. Categorizing these correctly at the source ensures you have the right "documentary evidence" linked to the right bucket.

Eliminating the "Latency Trap" with Automation

Sorting expenses manually into these categories often leads to a 30-day "visibility gap." By the time an employee submits a manual report, the data is already too old to influence decision-making.

An automated expense management software bridges this gap by using Merchant Category Codes (MCC). When an employee swipes their card at a hotel, the software instantly identifies the MCC, assigns it to the "Lodging" category, and triggers a text prompt for the receipt—all before the employee even checks out.

41 Essential Business Expense Categories

If you’re making a list of business expense categories for the first time or simply need a reminder, here are the most common types you might want to include:

1. Utilities

For those operating out of a commercial space, utility costs are generally fully deductible. This includes electricity, water, internet, phone, sewage, and trash pickup.

- Record these based on the month of consumption, not the date the bill arrives.

- Prorate internet and phone bills if you operate from a home office, deducting only the business-use portion.

- Categorize these as operating expenses (OpEx) to keep your "occupancy costs" clearly defined.

2. Rent or Mortgage Costs

Payments for the space where you conduct business are primary occupancy expenses.

- Rent payments: These are fully deductible in the month the space is used. If you pay for March in February, the payment sits as a prepaid asset) until March 1.

- Mortgage interest: If you own your business premises, you can deduct the interest portion of your mortgage payments.

- Principal payments: Unlike interest, the principal portion of a mortgage payment is not deductible; it increases your equity in the asset.

- Capitalization rules: In some specific scenarios, interest must be capitalized rather than deducted immediately.

3. Office Supplies and Office Assets

The IRS makes a critical distinction here between items you "use up" and items you "keep".

- Office supplies: These are consumable items like stationery, paper towels, and cleaning supplies consumed within the tax year.

- De minimis safe harbor: Many SMBs use an election to immediately deduct asset purchases (like a new $1,200 laptop) that would normally require depreciation, provided the cost is under the $2,500 threshold.

- Capitalized assets: Large purchases like machinery, vehicles, and furniture must be capitalized. Their cost is recovered over several years through depreciation based on their MACRS recovery period.

- Freight and installation: Remember that the cost of getting an asset "ready for use" must be added to the asset's basis and capitalized rather than expensed.

(See IRS Regulations section 1.263A-2 for information on these rules. )

4. Bank Fees and Credit Card Charges

Ordinary and necessary fees charged on your business accounts are deductible.

- Service fees: This includes monthly maintenance, wire transfer fees, and overdraft protection costs.

- Processing fees: The transaction fees your business pays to accept credit card payments from customers are fully deductible.

- Interest vs. Fees: While bank service charges belong here, interest on a business line of credit should be categorized under a dedicated "Interest Expense" bucket for better visibility

5. Website Expenses

The cost of maintaining your digital storefront is deductible, but the timing depends on when the work was done.

- Operating costs: Monthly hosting, domain renewals, and ongoing maintenance fees are standard operating expenses.

- Design and development: Fees for web designers or new templates are generally deductible.

- Pre-launch costs: Significant design costs incurred before the business officially begins operations are treated as startup costs and must be amortized over 15 years

Note: Significant costs incurred in creating a website, especially before business operations begin, might need to be treated as startup costs and amortized rather than deducted immediately.

6. Software Expenses

As most business tools move to subscription models, software is now a primary category for modern firms.

- Cloud-based subscriptions: CRM, accounting, and project management tools (SaaS) are deductible in the period the service is provided.

- Annual vs. Monthly: If you pay for an annual subscription in June, you should recognize 6 months of expense in the current year and 6 months as a prepaid asset for the following year.

- Bundled software: If software is included in the price of hardware (like a pre-installed OS), it is treated as part of the hardware asset and depreciated.

7. Printing Expenses

This category is often overlooked but essential for firms that rely on physical documentation or marketing.

- Consumables: Paper, ink, and toner used for business-related documents are deductible.

- Equipment maintenance: Repairs to office printers and copiers are recognized in the period they occur to keep the machines in working order.

8. Postage And Shipping

Categorizing shipping correctly is vital for maintaining accurate gross margins.

- Operating postage: Mailing invoices, marketing materials, and business correspondence belongs in your operating expenses.

- Freight-in: Shipping costs for raw materials or inventory you intend to sell should be included in your Cost of Goods Sold (COGS) calculation.

- Packaging supplies: Boxes and tape used for shipping products are deductible as business supplies.

9. Employee Salaries

Managing this category requires moving beyond simply recording a net pay amount; it involves documenting the justification for the compensation and ensuring the timing of the expense matches the work performed.

Test 1: The Reasonableness Test

The IRS evaluates whether the pay is appropriate for the value provided to the business. Factors that influence this determination include:

- Job duties: The nature, scope, and complexity of the work performed..

- Workload: The actual volume of work handled and the specific level of responsibility..

- Business complexity: The intricacy and operational demands of the specific business..

- Time commitment: The amount of time the employee dedicated to their role..

- Cost of living: The prevailing living expenses in the geographical area where the work is done..

- Employee performance: The specific skills, experience, and accomplishments of the individual..

- Compensation equity: The employee’s pay relative to the company’s overall profitability and distributions to shareholders..

- Company pay policy: The established pay structure and internal compensation guidelines..

- Pay history: The employee’s individual salary progression over the course of their tenure..

Test 2: For Services Performed

You must be able to prove that the payments were made for business-related services that were actually completed.. This prevents companies from using "salary" as a way to hide personal gifts or non-deductible payments..

- Compensation types. This category includes base wages, bonuses, commissions, vacation allowances, and non-cash fringe benefits..

- Accrued payroll. If employees work during the final week of a quarter but aren't paid until the next month, you must record an "accrued salaries" liability.. For example, if June 30th falls on a Wednesday, a portion of the biweekly payroll—representing the work done in June—must be accrued in that fiscal year to ensure accurate reporting..

- Termination costs. Severance, outplacement fees, and training costs for terminated employees are accrued if the notice was provided before the quarter-end..

- Extra/additional compensation. Significant bonuses or stipends paid after the fiscal year ends but relating to the prior year's performance must be recorded as an accrual at year-end.

10. Employee Training and Education

Investing in your team’s skills is deductible, provided the education relates to their current role.

- Skill maintenance: Seminars, courses, and in-house programs that improve an employee's performance in their existing job are deductible.

- New career paths: Education that qualifies an employee for a new trade or business is generally not a deductible business expense.

- Assistance programs: Reimbursements through a qualified educational assistance program are deductible and often provide tax benefits for the employee as well.

11. Employee Benefit Programs

Investing in your team’s well-being is deductible, provided the programs meet specific IRS requirements for non-discrimination. This category allows you to subtract the costs of maintaining various welfare plans from your taxable income.

- Health and accident plans: Premiums for medical and dental insurance paid for employees are generally deductible.

- Adoption assistance: Costs associated with helping employees through the adoption process can be claimed as a business expense.

- Dependent care assistance: Contributions to help employees manage childcare or eldercare are deductible within specific annual limits.

- Life insurance: Premiums are deductible if the policy covers officers or employees, provided the company is not a direct or indirect beneficiary.

- Insurance accruals: For policies managed directly by your business units rather than a central office, you should record accruals based on the number of days in the policy period that fall within the current fiscal year.

12. Employee Reimbursements

How you handle employee reimbursements determines whether the money is treated as a deductible business expense or taxable wages for the employee.

- The Accountable Plan: To ensure reimbursements are tax-free, you must use an IRS-approved "Accountable Plan". This requires employees to substantiate expenses within a "reasonable period" (usually 60 days) and return excess funds within 120 days.

- Non-Accountable Plan: If your plan does not require substantiation or the return of excess funds, the IRS treats these payments as taxable wages reported on Form W-2.

- Accrual logic: If an employee incurs an expense in one quarter but isn't reimbursed until the next, the expense should be recognized in the period it was incurred to maintain financial visibility.

Also Read

13. Work Opportunity Tax Credit (WOTC)

The Work Opportunity Tax Credit (WOTC) is a federal tax credit available to employers who hire individuals from certain targeted groups who have faced significant barriers to employment. Some of these groups include:

- Veterans

- Recipients of Supplemental Nutrition Assistance Program (SNAP) benefits

- Recipients of Supplemental Security Income (SSI) benefits

- Young people ages 16-24 who are not in school or working

- Ex-felons

You can claim a credit of up to $2,400 for each eligible employee you hire. The credit is equal to 40% of the first $6,000 of qualified wages paid to or incurred on behalf of an individual who:

- Are in their first year of employment;

- Are certified as being a member of a targeted group; and

- Perform at least 400 hours of services for that employer

14. Employer Credit for Paid Family and Medical Leave

The Employer Credit for Paid Family and Medical Leave encourages businesses to offer paid leave to employees for family or medical reasons.

- Credit amount: The credit can reach 100% of the wages paid to eligible employees on leave, with a cap of $5,112 per employee per year.

- Sunset clause: While highly beneficial, it is important to note that this credit was scheduled to expire for wages paid after December 31, 2025, unless extended by 2026 legislation.

15. Business Trip Expenses

Travel expenses are deductible when they are directly related to your trade or business, but the IRS applies strict boundaries to prevent personal use from being written off.

- The "Tax Home" rule: Travel must be away from your tax home—the general area where your main place of business is located.

- The "Sleep or Rest" rule: You are only considered to be traveling away from home if your duties require you to be away longer than an ordinary day's work and you require sleep or rest while away.

- Multi-purpose trips: If a trip is primarily for business, the airfare is fully deductible; however, costs for personal side-trips or extra vacation days are not.

- The 50% meal limit: Most business meals are only 50% deductible, requiring detailed logs of the time, place, and business purpose.

Remember that meal expenses are generally only 50% deductible. Detailed records proving the amount, time, place, and business purpose are crucial.

16. Business Gifts

Giving gifts to clients or employees is a recognized business practice, but the IRS imposes a specific "per-person" cap to limit abuse.

- The $25 limit: You can only deduct up to $25 per recipient, per year.

- Incidental costs: Packaging, engraving, and mailing costs generally do not count toward the $25 limit unless they add substantial value to the gift.

- Promotional exceptions: Items costing $4 or less with your company name permanently imprinted are not subject to the $25 limit.

17. Car Expenses (Standard Mileage vs. Actual Costs)

When using a car for business, you have two primary options for calculating your deductible expenses: the standard mileage rate or actual car expenses.

- Standard Mileage Rate: For 2026, the rate is 72.5 cents per mile. This method is a simplified way to track car expenses, but if you choose it, you cannot deduct actual expenses, such as gas, repairs, and insurance.

- Actual Car Expenses: This method requires you to track all costs associated with your vehicle, including gas, oil, repairs, insurance, and depreciation. You can then deduct the portion of these expenses that is directly related to business use, based on the percentage of business miles driven.

The IRS requires adequate records to prove your car's business use, including a log of business mileage, dates, destinations, and business purpose.

Also Read

18. Depreciation

Depreciation is a fundamental concept for businesses that own tangible assets expected to last more than one year. Instead of deducting the full purchase price immediately, depreciation allows you to systematically deduct portions of the asset's cost over its predetermined useful life or "recovery period." Think of it as accounting for the wear and tear or obsolescence of your business property over time.

Here's a breakdown of key points regarding depreciation:

- What Qualifies for Depreciation? Depreciation applies to tangible assets you own and use in your business or hold to produce income, such as buildings, machinery, equipment, furniture, and vehicles. The property must have a determinable useful life, meaning it wears out or loses value. Land itself cannot be depreciated. Inventory held for sale is also not depreciated.

- Purpose: It's the method for recovering the cost of assets that provide value to your business for longer than a single tax year.

- Depreciation System (MACRS): The primary method used for most property placed in service after 1986 is the Modified Accelerated Cost Recovery System (MACRS). MACRS assigns assets to specific property classes with defined recovery periods.

- Section 179 Deduction: This allows businesses to elect to treat the cost (or part of the cost) of certain qualifying property as an expense and deduct it in the year the property is placed in service, subject to dollar limits and business income limitations. This is an alternative to recovering the cost via yearly depreciation deductions.

- Special (Bonus) Depreciation Allowance: For certain qualified property (often new, but sometimes used, assets acquired and placed in service by certain dates), businesses may be able to claim an additional first-year depreciation deduction. The percentage for this allowance is currently phasing down (it was 100% for certain property, then 80%, and is 60% for property placed in service in 2024).

- Form 4562: This is the primary IRS form used to calculate and report depreciation deductions, including the Section 179 deduction and the special depreciation allowance.

- Listed Property: Special rules and stricter recordkeeping requirements apply to "listed property," which includes assets like passenger automobiles and property generally used for entertainment or recreation, due to their potential for personal use. For these assets, claiming depreciation often requires proving that business use exceeds 50%.

Calculating depreciation can be complex, involving factors like the asset's basis, the date it was placed in service, the applicable depreciation method, and the recovery period. Consulting IRS Publication 946, How to Depreciate Property, is highly recommended for detailed guidance.

19. Legal And Professional Expenses

Fees paid to professionals like lawyers, accountants, consultants, and tax preparers are deductible if they are ordinary and necessary expenses directly related to operating your business. This includes fees for tax advice and preparation of the business-related parts of your tax return.

Fees paid to acquire business assets or for work of a personal nature (like drafting a personal will) are generally not deductible as business expenses; acquisition costs are added to the asset's basis.

20. Taxes (Other than Business Taxes)

Beyond income, employment, property, and sales taxes already mentioned, other taxes directly attributable to your trade or business are deductible. This can include:

- Federal excise taxes (unless part of the cost of fuel or other items).

- State or local franchise taxes.

- Occupational taxes charged by a locality for the privilege of conducting business.

21. Business Insurance

Liability insurance, worker's compensation, disability, and other business-related insurance are deductible. However, commercial auto insurance is a bit more complex; if you use the vehicle solely for commuting, it doesn't count as a business expense. On the other hand, driving the car for business reasons but still using it for personal purposes will likely grant you a partial tax deduction.

Listed below are some other deductions you can make for premiums if you pay for the following kinds of insurance:

- Property and casualty insurance: Covers losses due to fire, theft, accidents, or other unforeseen events.

- Credit insurance: Protects against losses arising from unpaid customer debts.

- Health and medical insurance: Covers employees' medical expenses, including long-term care. For partnerships, premiums paid for partners are deductible as guaranteed payments.

- Liability insurance: Safeguards against legal claims resulting from damages or injuries caused by your business activities.

- Malpractice insurance: Protects healthcare professionals against claims of professional negligence leading to patient harm.

- Workers' compensation insurance: Mandatory insurance that covers employee injuries or illnesses arising from work-related activities.

- Unemployment insurance contributions: Deductible if considered taxes under state law.

- Overhead insurance: Covers business expenses incurred during prolonged disability due to personal injury or illness.

- Vehicle insurance: Covers business vehicles for liability, damages, and other losses. If a vehicle serves both personal and business purposes, only the portion attributed to business use is deductible. If using the standard mileage rate for vehicle expenses, no insurance premium deduction is allowed.

- Life insurance: Deductible if covering officers or employees, provided you are not a direct or indirect beneficiary.

- Business interruption insurance: Compensates for lost profits due to temporary business disruptions.

22. Bank Service Charges

Beyond general bank fees (#4), this can include specific service charges like fees for check printing, stop-payment orders on business checks, wire transfer fees for business payments, and fees for maintaining a business line of credit. Interest paid on a business line of credit is deductible as interest expense.

23. Internet Expenses

The cost of internet service used for your business is a deductible utility expense. If you have internet service at your business location, the entire cost is generally deductible. If you work from a home office and use the same internet service for both business and personal use, you must allocate the cost and deduct only the portion attributable to business use.

24. Continuing Education

Education expenses are deductible if they maintain or improve the skills required for your current job.

- Seminars and courses: Registration fees, books, and materials for industry-specific training are fully deductible.

- Qualified Educational Assistance Programs: You can reimburse employees up to a certain threshold for education expenses tax-free, and the business can deduct those payments as a benefit.

- Career shifts: Education that prepares you or an employee for a new career or trade is generally not a business deduction.

For information, read the IRS’s Frequently asked questions about educational assistance programs.

25. Dues And Subscriptions Expense

Keeping up with industry trends through professional associations and journals is a recognized operating cost.

- Professional organizations: Dues paid to groups like bar associations, medical societies, or trade boards are deductible.

- Trade journals: Subscriptions to technical or professional magazines related to your field are deductible.

- Social clubs: Dues for country clubs, airline lounges, or golf clubs are generally non-deductible, even if you use them for business networking.

26. Credit And Collection Fees

If you use the accrual method of accounting, you sometimes have to deal with money you were owed but will never see.

- Bad debt deduction: If an account receivable becomes truly uncollectible, accrual-basis taxpayers can deduct it as a bad debt.

- Collection agency fees: The cost of hiring a firm to chase down outstanding invoices is a deductible professional service.

- Cash-method limitation: If you use cash accounting, you cannot deduct uncollected revenue because it was never recorded as income in the first place.

27. Medical Expenses

Self-employed individuals have a specific path for deducting health insurance that is different from a standard business expense.

- Schedule 1 (Form 1040): Premiums for medical, dental, and qualified long-term care insurance for you and your family are typically an "adjustment to income" rather than a Schedule C deduction.

- The 27-year-old rule: Your coverage can include children under age 27, even if they aren't your legal dependents.

- Subsidized plan trap: You cannot take this deduction for any month you were eligible to participate in a subsidized plan through a spouse's employer.

28. Licenses And Permits

These are the government "gatekeeper" costs required to keep your doors open.

- Annual renewals: Standard renewal fees for professional or state operating licenses are deductible in the year they are paid.

- Long-term licenses: If a license grants rights over a multi-year period, the IRS may require you to amortize the cost over several years rather than expensing it at once.

29. Maintenance And Repairs

This is a critical area where many businesses make mistakes. You must distinguish between "fixing" and "improving."

- Deductible repairs: These are costs that restore an asset to its original condition without adding value. Examples include fixing a leak, repainting, or changing the oil in a company vehicle.

- Capital improvements: These are costs that "better" the property or prolong its life, like replacing an entire roof or rewiring a building. These must be capitalized and depreciated.

- The "Character" test: If the asset performs the same function as before the work, it’s a repair; if it does more or lasts longer, it’s an improvement.

30. Telephone

Managing communication costs requires a clean split between personal and professional use.

- Dedicated business lines: The full cost of a dedicated office line or a second phone line in your home is deductible.

- First landline rule: You generally cannot deduct the basic cost of the first landline in your home, even if you use it for business.

- Cell phone business use: You can deduct the percentage of your cell phone bill that corresponds to your actual business use.

31. Startup Expenses

Getting a new business off the ground involves various costs incurred before you officially open your doors or begin active operations. These pre-opening expenses fall into two main categories: startup costs and organizational costs. The IRS allows you to deduct a portion of these costs immediately and amortize (deduct over time) the rest.

What are Startup Costs?

These are costs paid or incurred for either:

- Creating an active trade or business.

- Investigating the creation or acquisition of an active trade or business.

What are Organizational Costs?

These are costs specifically related to forming a corporation or a partnership.

Deductibility Rules for Startup Expenses

Generally, these are capital expenses. However, you can elect to:

- Deduct up to $5,000 in business startup costs AND

- Deduct up to $5,000 in organizational costs

- This deduction applies to the tax year in which your active trade or business begins.

- Important Limit: The $5,000 deduction for each category is reduced (dollar-for-dollar) by the amount your total startup or organizational costs exceed $50,000, respectively.

- Any remaining costs above the initial $5,000 deduction must be amortized (deducted in equal parts) over 180 months (15 years), starting with the month the business begins.

Qualifying Startup Costs

To qualify for the deduction/amortization, a startup cost must meet both these tests:

- It would be deductible if paid or incurred to operate an existing active trade or business in the same field.

- It is paid or incurred before the day your active trade or business begins.

Examples of Deductible Startup Costs Include

- Market Research: Analysis or surveys of potential markets, products, labor supply, transportation facilities, etc.

- Opening Promotion: Advertising for the business's launch.

- Employee Training: Salaries and wages for employees being trained before opening, and their instructors.

- Business Development: Travel and other necessary costs to secure prospective distributors, suppliers, or customers.

- Professional Services: Salaries and fees for executives, consultants, legal, and accounting services related to starting the business.

Costs NOT Considered Startup Costs

Deductible interest, taxes, and research & experimental costs are not treated as startup costs and follow their own deduction rules.

Investigating vs. Acquiring

Costs incurred during a general search or preliminary investigation of whether to create or purchase a business qualify as startup costs. However, costs incurred in the attempt to acquire a specific business (like drafting purchase agreements after deciding to buy) are capital expenses related to the acquisition and cannot be deducted/amortized as startup costs.

Remember to make the election to deduct/amortize these costs on the tax return for the year your business begins active operations. Form 4562 is used for amortization. Consult IRS Publication 535 for full details on startup and organizational costs.

32. Depletion

If your business involves the extraction of natural resources such as timber, minerals, or oil and gas, you recognize the exhaustion of these assets through depletion.

- Cost depletion. This method allocates the basis of the resource over the total number of units expected to be extracted.

- Percentage depletion. This method applies a fixed percentage to the gross income from the property, though it is subject to specific IRS limitations based on the resource type

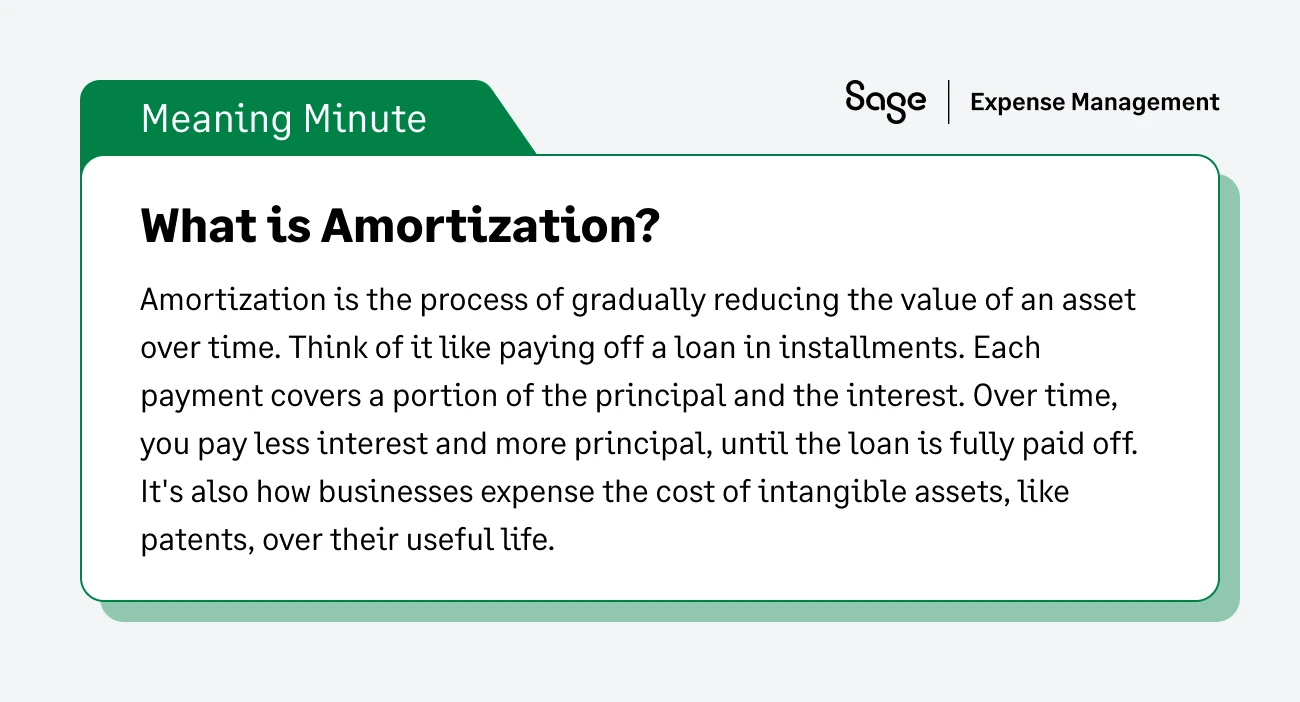

33. Amortization

Amortization is the process of gradually expensing the cost of intangible assets over a set period, mirroring how depreciation works for physical items.

- Section 197 intangibles. Assets like goodwill, patents, copyrights, customer lists, and franchises are typically amortized over a 15-year period.

- Software development. While cloud-based subscriptions are operating expenses, significant costs for developing proprietary software may need to be capitalized and amortized.

- Lease acquisition. Fees paid to secure a business lease are often amortized over the life of the lease agreement rather than being expensed immediately.

34. Bad Debts (Non-Credit Sale Related)

A business bad debt is a loss from a debt that becomes worthless and was created or acquired in your trade or business.

- Accrual method requirement. To deduct a bad debt from a credit sale, you must have previously included that amount in your income.

- Proof of worthlessness. You must demonstrate that you have taken reasonable steps to collect the debt and that it is truly uncollectible.

- Non-credit sale debts. This includes loans made to suppliers, clients, or employees for legitimate business reasons that are not repaid.

35. Moving Expenses (Business Assets vs. Personal Relocation)

The deductibility of moving costs depends strictly on whether you are moving assets or relocating yourself.

- Business asset relocation. The cost of moving machinery, inventory, or equipment from one business location to another is generally a deductible operating expense.

- Installation of new assets. Costs to move and install newly purchased machinery are not deducted immediately; they are added to the asset’s basis and capitalized.

- Personal relocation suspension. For tax years 2018 through 2025 (and likely 2026 pending legislation), the deduction for personal moving expenses is suspended for most taxpayers except for active-duty military moving due to a permanent change of station

36. Charitable Contributions (Business Context)

Charitable giving is typically a personal deduction, but it can be a business expense if it functions as a strategic marketing effort.

- Direct business relationship. A payment to a charity is deductible as a business expense if there is a reasonable expectation of a financial return, such as sponsoring an event to prominently display your brand.

- Corporate rules. Corporations have specific limits and rules for direct charitable contributions that differ from those of sole proprietorships or partnerships

37. Child And/Or Dependent Care

Personal childcare is not a business deduction, but providing care for your employees is a valid business expense.

- Employer-provided facilities. Costs for providing or paying for qualified childcare for employees are deductible business expenses.

- Tax credits for employers. You may also be eligible for a specific tax credit for employer-provided childcare facilities using Form 8882.

38. Employee Benefit Programs (Other than Health/Pension)

Beyond health and retirement, many other benefit programs provide valid tax write-offs for the employer.

- Group-term life insurance. Premiums for up to $50,000 of coverage per employee are generally deductible.

- Assistance programs. This includes adoption assistance and dependent care assistance programs, provided they follow IRS contribution limits.

- Welfare benefit funds. Contributions to these funds are deductible but are subject to strict oversight and limits

39. Marketing Expenses

Marketing and advertising costs are deductible if they are reasonable and directly related to your business activities.

- Digital and print media. This covers online ads, search engine marketing, commercials, and traditional print efforts.

- Institutional advertising. Costs for "goodwill" advertising to keep your name in front of the public are deductible if they relate to future business you reasonably expect to gain.

- Lobbying exclusion. Expenses incurred to influence legislation or participate in political campaigns are not deductible.

40. Foreign Earned Income

Operating internationally introduces specific tax deductions related to foreign obligations.

- Foreign tax credit. You can often choose between taking foreign income taxes as a deduction or a credit, with the credit usually being more financially beneficial.

- Real property taxes. Taxes paid on business property located in a foreign country are fully deductible

For more details on these, see Publication 54. For information on the foreign tax credit, see Publication 514.

41. Manufacturing Or Raw Materials

This category is distinct from office supplies and is a primary component of your Cost of Goods Sold (COGS).

- Raw materials. This includes the cost of all physical components that become part of a product you manufacture or sell.

- Production supplies. Consumables used directly in the manufacturing process are included here.

- Inventory accounting. For many businesses, these costs are deducted when the materials are actually used or sold rather than when they are purchased.

For more information, see Cost of goods sold—chapter 6 of Pub. 334.

How To Categorize Expenses for Your SMB or Startup

Structuring your expenses isn't just a tax-time chore; it is the process of building a high-fidelity map of your business's financial health.

To move away from the "latency trap" of manual bookkeeping, follow this four-step workflow to ensure your books are always audit-ready and strategically useful.

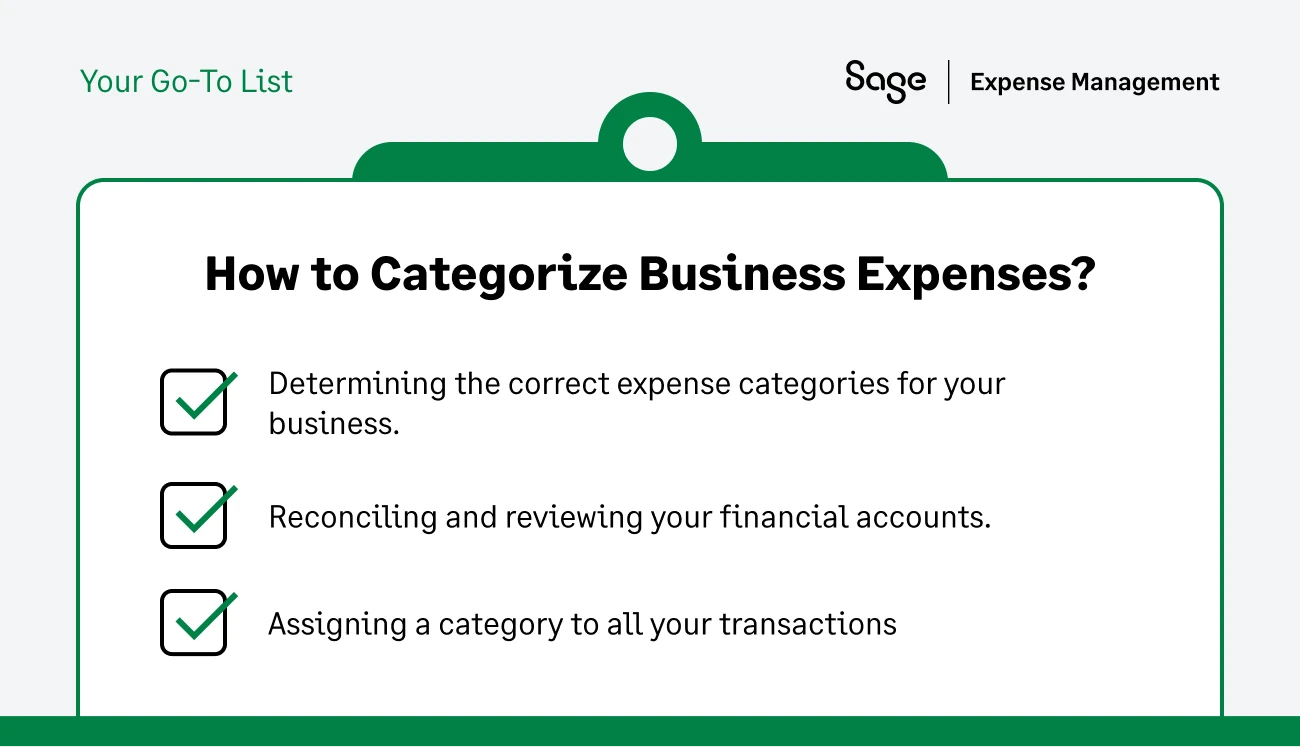

Step 1: Determine Expense Categories For Your Business

Your Chart of Accounts (COA) is the blueprint of your business. Categorization must be tailored to your specific industry to provide meaningful insights.

- Identify your high-velocity buckets: A SaaS company will prioritize digital services and software subscriptions, while a physical retailer must focus on storage and shipping.

- Use professional "Object Codes": Move beyond generic names by assigning specific numerical codes to categories, such as using Object Code 0540 for prepaids and 2191 for accruals to distinguish between what you own and what you owe.

- Align with your revenue model: Ensure your expense categories mirror the revenue they support so you can accurately calculate your gross margins.

Step 2: Reconcile And Review Your Financial Accounts Regularly

Waiting 30 days for a bank statement to appear is a recipe for data "leakage."

- Connect at the source: Use an expense platform that connects to your existing Visa or Mastercard via direct integrations.

- Monitor liabilities as they happen: Real-time feeds allow the finance team to see a "swipe" the second it occurs, rather than waiting for it to clear the bank 48 hours later.

- Eliminate bank switching: Look for "card-agnostic" solutions that provide this automation without forcing you to move your credit lines or change your banking relationship.

Step 3: Assign A Category To All Transactions

Categorizing an expense correctly requires understanding when the value is consumed, not just when the bill is paid.

- Distinguish between OpEx and CapEx: Assign day-to-day costs (like marketing) as operating expenses, but ensure larger assets (like machinery) are categorized as capital expenditures for depreciation.

- Capture accruals and prepaids: If you pay for an annual insurance policy in January, categorize it as a "prepaid asset" and recognize the expense proportionately throughout the year.

- Identify the business purpose: Every assigned category should be backed by a clear "why" to satisfy the IRS's "ordinary and necessary" requirement.

Step 4: Keep a Digital, Audit-Ready Trail for All Receipts

The IRS requires "documentary evidence" to support your deductions. For a receipt to be considered "adequate," it must be digitized and linked directly to the categorized transaction.

- Ensure four-point verification: Every digital record must show the vendor's name, the date of purchase, an itemized description, and the total amount paid.

- Automate the receipt chase: Use conversational AI that texts employees the moment a card is swiped, allowing them to reply with a photo of the receipt before they even leave the store.

- Centralize the repository: Store all digitized proof in a secure, searchable location so that pulling documentation for a tax audit becomes a one-click task rather than a "shoebox" scavenger hunt.

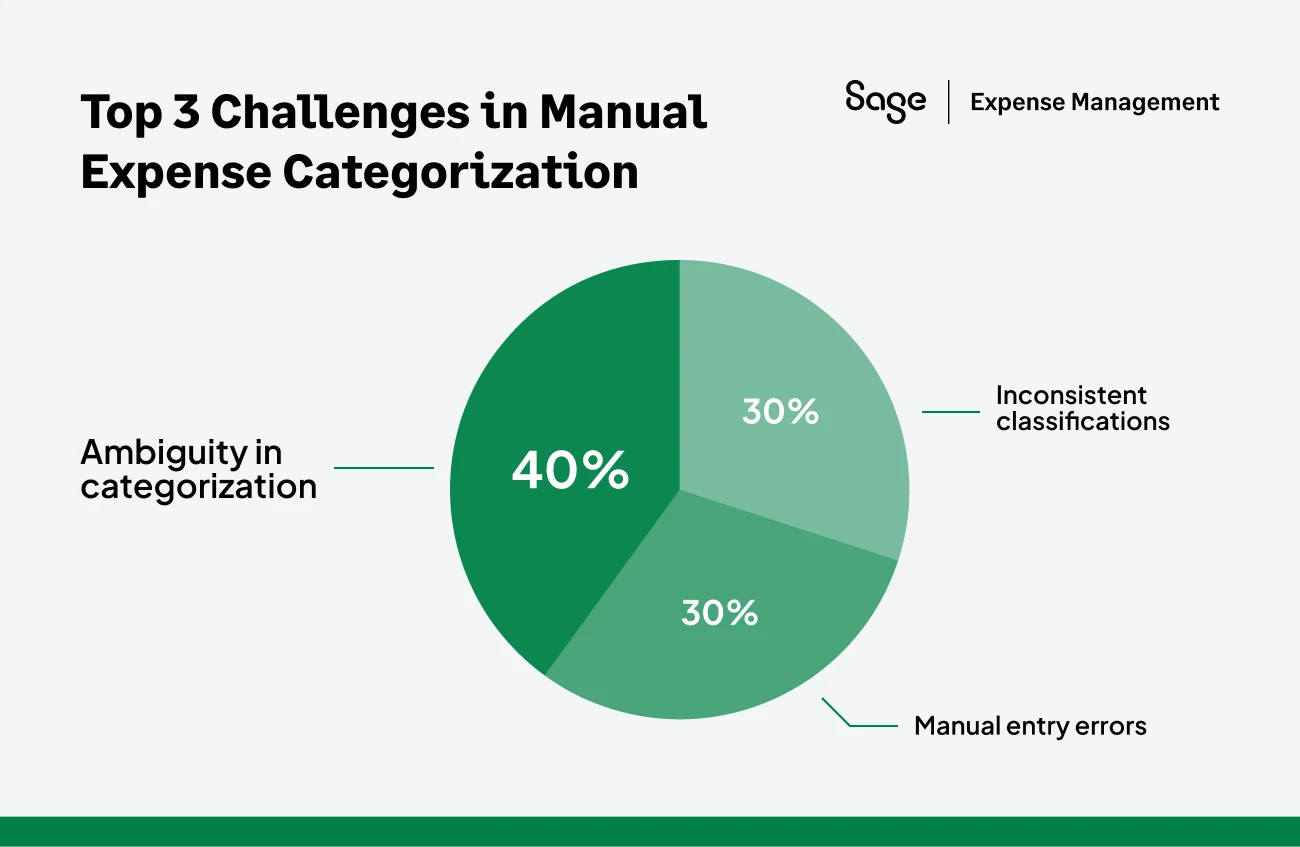

The Problems with Manual Expense Categorization

Manually managing business expenses is a tedious and time-consuming process that can cost your business thousands of dollars and countless hours every year. This "dark side" of manual expense management is exactly what a modern finance team is trying to avoid.

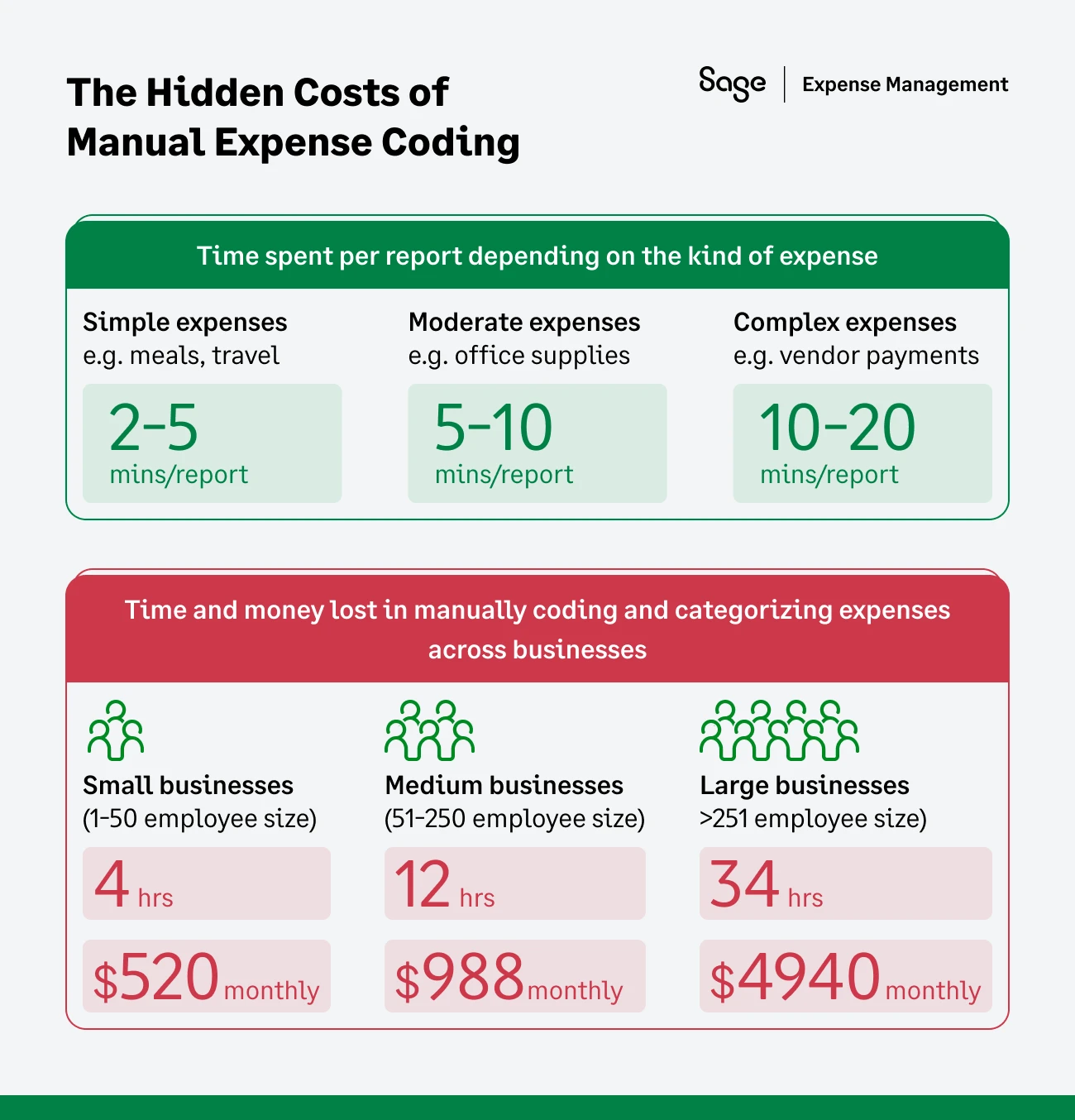

The Hidden Costs of Manual Data Entry

According to internal research, processing a simple travel or meal expense takes 2-5 minutes of manual labor, while complex vendor payments or multi-line reimbursements can drain 10-20 minutes per report.

When these small increments are scaled across an organization, the financial drain is substantial:

- Small businesses (1-50 employees) lose an average of 4 hours and $520 every month to manual coding alone.

- Mid-market companies (51-250 employees) see this jump to 12 hours and nearly $1,000 per month.

This time isn't just "lost"—it is time that could have been spent on high-impact financial analysis, budgeting, or cost optimization.

The Financial Risk of Errors and Fraud

A manual process is a structural vulnerability. Without real-time oversight, your business is susceptible to both honest human error and intentional fraud. From transposing a digit on an invoice to selecting the wrong "Object Code" for a prepaid asset, manual entry is prone to mistakes that skew your financial statements.

More critically, companies without automated guardrails face a median loss of $140,000 annually from expense fraud. This fraud typically manifests in four ways:

- Expense inflation: Padding receipts or adding "buffer" to a claim accounts for 25-50% of fraudulent activity.

- Personal use: Using the corporate card for non-business purchases makes up 15-30% of fraudulent claims.

- Duplicate submissions: Submitting the same digital and physical receipt multiple times is a common issue in 10-20% of cases.

- Mileage falsification: Overstating distances traveled accounts for 5-15% of fraudulent claims.

The Headache of Lost Productivity

The "receipt chase" is the bane of every financial controller’s existence. Employees are hired for their primary roles—not to be junior accountants—which makes collecting documentation feel like "pulling teeth."

This creates a cycle of inefficiency:

- Delayed month-end close: Chasing missing documentation for a travel lodging folio (required by IRS 463) can delay your reports by days or weeks.

- The shoebox problem: Scrambling to organize "shoeboxes of fading paper" during an audit is not a viable strategy; it is a high-stress administrative burden that damages team morale.

- Lack of audit-readiness: If an expense lacks "documentary evidence" like the vendor name, date, and amount, the IRS can disallow the deduction, leading to fines and penalties.

By the time a manual report is finally approved, the data is already too old to influence the business's current spending trajectory. You aren't managing your expenses; you are simply archiving them.

How Sage Expense Management Simplifies Expense Categorization

You don't need more manual labor to fix a broken process; you just need to meet employees where they already are. Sage Expense Management (SEM) is designed to solve the "latency trap"—the 30-day visibility gap created by traditional bank statements—by capturing spend data at the moment of the transaction.

Here is how SEM automates your categorization and ensures your books are always audit-ready.

Bridging the Visibility Gap with Real-time Purchase Alerts

Most expense software waits for a bank statement to appear, meaning your data is already 48 to 72 hours old by the time you see it. SEM connects directly to your existing business credit cards via real-time network feeds.

- Keep your existing bank: You get real-time automation without the administrative burden of switching your credit lines or moving your bank accounts to a new fintech card provider.

- Instant notifications: The second a card is swiped, you get a text message that notifies you of spend.

- Immediate awareness: Finance teams see expenses as they happen, allowing for more accurate month-end accruals for items like lodging or travel that haven't been reimbursed yet.

Receipt Capture that Meets IRS Documentary Evidence Standards

The IRS requires "documentary evidence" for all lodging and any expense over $75.

SEM uses conversational AI to ensure these records are collected before the employee even leaves the store.

- Conversational AI: Simply text a receipt to SEM, for a reimbursement or a credit card expense, our AI will match is to the right transaction.

- Automatic extraction: Our OCR technology extracts the "four-point verification" required by the IRS: vendor name, date, amount, and itemized description.

- Multi-channel submission: Employees can also submit documentation via Slack, Gmail, Outlook, or our mobile app, ensuring no receipt is left in a shoebox.

Automating the General Ledger with Merchant-based Rules

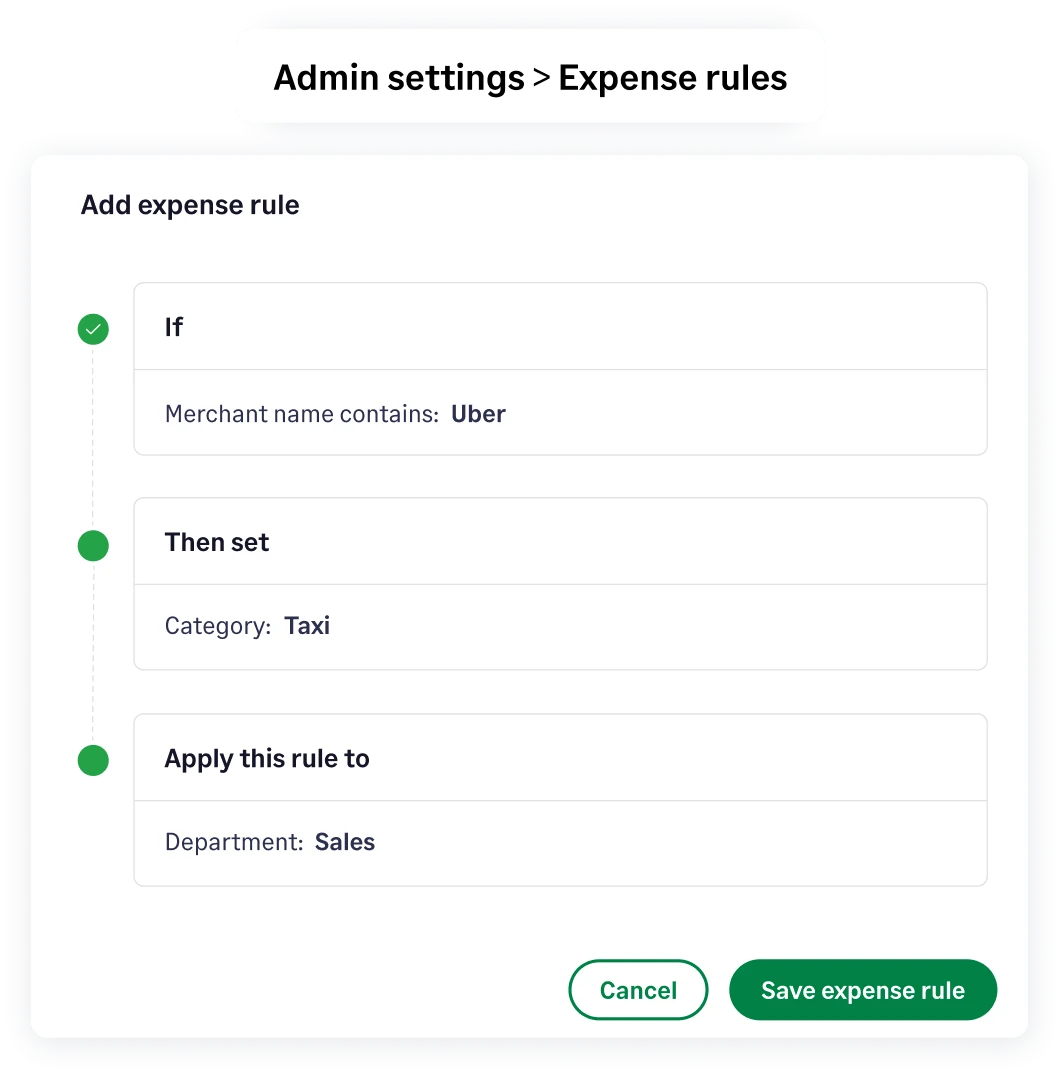

Assigning categories manually is a primary source of human error. SEM uses Merchant Category Codes (MCC) and custom rules to map every transaction to your Chart of Accounts automatically.

- Auto-fill categories: When a card is used at a hotel, the system identifies the MCC and automatically fills the "Category" field as Lodging.

- Custom business rules: You can pre-define rules that map specific merchants to your internal projects, departments, or "Object Codes." For example, if the merchant is "Uber," the system can automatically set the Category to "Taxi" and the Purpose to "Travel to Client Site."

- Bidirectional GL sync: Fully coded and approved expenses push directly into Sage Intacct, NetSuite, or QuickBooks. This ensures that "Prepaid Assets" and "Accrued Liabilities" are always recorded in the correct bucket on your balance sheet.

{{expense-coding-ai="/cta-banners"}}

FAQs Around Business Expense Categories

What can be Written Off as a Business Expense?

Any expense that counts as ordinary and necessary to conduct business can be deducted as a business expense.

What Can’t Be Written Off as a Business Expense?

Personal expenses, entertainment expenses, fines or penalties paid to a government for violating a law, illegal payments, and dues to various country clubs cannot be written off.

Can You Deduct Job Expenses?

Generally, you cannot deduct job-related expenses. However, if you have reimbursed your workers for relocation or other costs under an accountable plan, you can deduct the reimbursement as a business expense.

Is There a Small Business Start-Up Costs Tax Deduction?

Yes. You can elect to deduct up to $5,000 of business startup costs and an additional $5,000 of organizational costs in the year your business begins. Any costs exceeding $50,000 reduce the deduction.

Can I take The Standard Deduction and still Deduct Business Expenses?

Yes. Business expenses are deducted from your gross income to determine your adjusted gross income, while the standard deduction (or itemized deductions) is taken from your adjusted gross income. Therefore, you can take the standard deduction and still deduct your business expenses.

What are the Different Types Of Expenses?

There are three different types of expenses: fixed, variable, and periodic .

- Fixed expenses: Expenses that don’t change, such as rent or mortgage payments.

- Variable expenses: Expenses that change from month to month, like utilities.

- Periodic expenses: Expenses that happen occasionally, like for emergencies or business travel.

What Kind of Records Do I Need to Keep for Each Expense?

The IRS requires that you keep "adequate records" to substantiate all deductions. This includes receipts, invoices, and canceled checks. A receipt should clearly show the vendor's name, the date of purchase, a description of the item, and the amount paid. For car expenses, you need to keep a log of mileage, dates, and business purpose.

How Long do I Need To Keep my Tax Records?

The general rule is to keep records for 3 years from the date you filed the original return. However, you must keep records for 7 years if you claim a bad debt deduction or a loss from worthless securities. Records related to property should be kept indefinitely, or at least until the period of limitations expires for the year in which you sell or dispose of the property.

Can I Deduct Car Expenses If My Employer Reimburses Me?

You can only deduct expenses that you are not reimbursed for. If your employer's reimbursement plan is an accountable plan, the reimbursements are not considered taxable income, and you do not deduct the expense. If it is a non-accountable plan, the reimbursement is included in your taxable wages (Form W-2), and you may be able to claim a deduction for the expense as an itemized deduction.

.webp)