For any growing business, the corporate credit card is an essential tool for managing expenses, separating personal and business spending, and streamlining financial operations. But in a market now flooded with options from both traditional banks and new fintech startups, choosing the right program can be confusing.

Should you stick with a trusted name like Chase or American Express? Or should you jump on the bandwagon with a new fintech like Ramp or Brex? This decision isn't just about rewards and annual fees; it's about choosing a financial partner that will support your business's long-term growth.

This guide is designed to cut through the noise. We'll demystify the corporate card landscape, break down the pros and cons of traditional banks versus fintechs, and, most importantly, show you how to choose a program that offers both the financial stability you need and the modern features you want.

What is a Corporate Credit Card?

A corporate credit card program provides employees with cards for business spending. The liability for the card's balance typically falls on the company, not the individual employee.

These cards are designed for:

- Large Enterprises: Companies with established financial histories and significant credit needs.

- Spend Control: The programs often include features for setting spending limits, tracking expenses, and integrating with accounting software.

It’s essential to distinguish them from business credit cards, which are typically issued to small business owners with personal liability attached, making them more accessible to small businesses.

A Key Difference: Corporate vs. Business Credit Cards

- Corporate Card: Issued to a corporation; liability often rests with the company. These are for larger businesses and have stricter underwriting criteria.

- Business Credit Card: Issued to a small business owner; personal liability is often attached. This is the more accessible and common choice for freelancers and SMBs.

While the term "corporate card" is often used loosely to describe any card an employee uses for business, a business credit card is the more accessible and practical choice for the vast majority of small and mid-sized businesses. It offers the same benefits of separating business and personal expenses but with more flexible approval requirements.

Who Issues Corporate Credit Cards?

The market is generally divided into two main camps:

Corporate Cards from Traditional Banks

These are issued by long-standing financial institutions with established credit relationships.

- American Express Corporate Card

- Chase Ink Business Preferred Card

- Citi Commercial Card

Corporate Card from Fintech Tools

These are offered by modern financial technology companies like Ramp, Expensify, and others that often focus on an integrated software experience.

Also Read

How to get a Corporate Credit Card? (An Illustrative Example with Ramp)

Let’s use Ramp’s corporate card as a real-world example to illustrate why these types of cards, while modern and feature-rich, are often difficult for most small and mid-sized businesses (SMBs) to obtain. While the application steps themselves might seem simple, the underlying eligibility requirements present the real barrier.

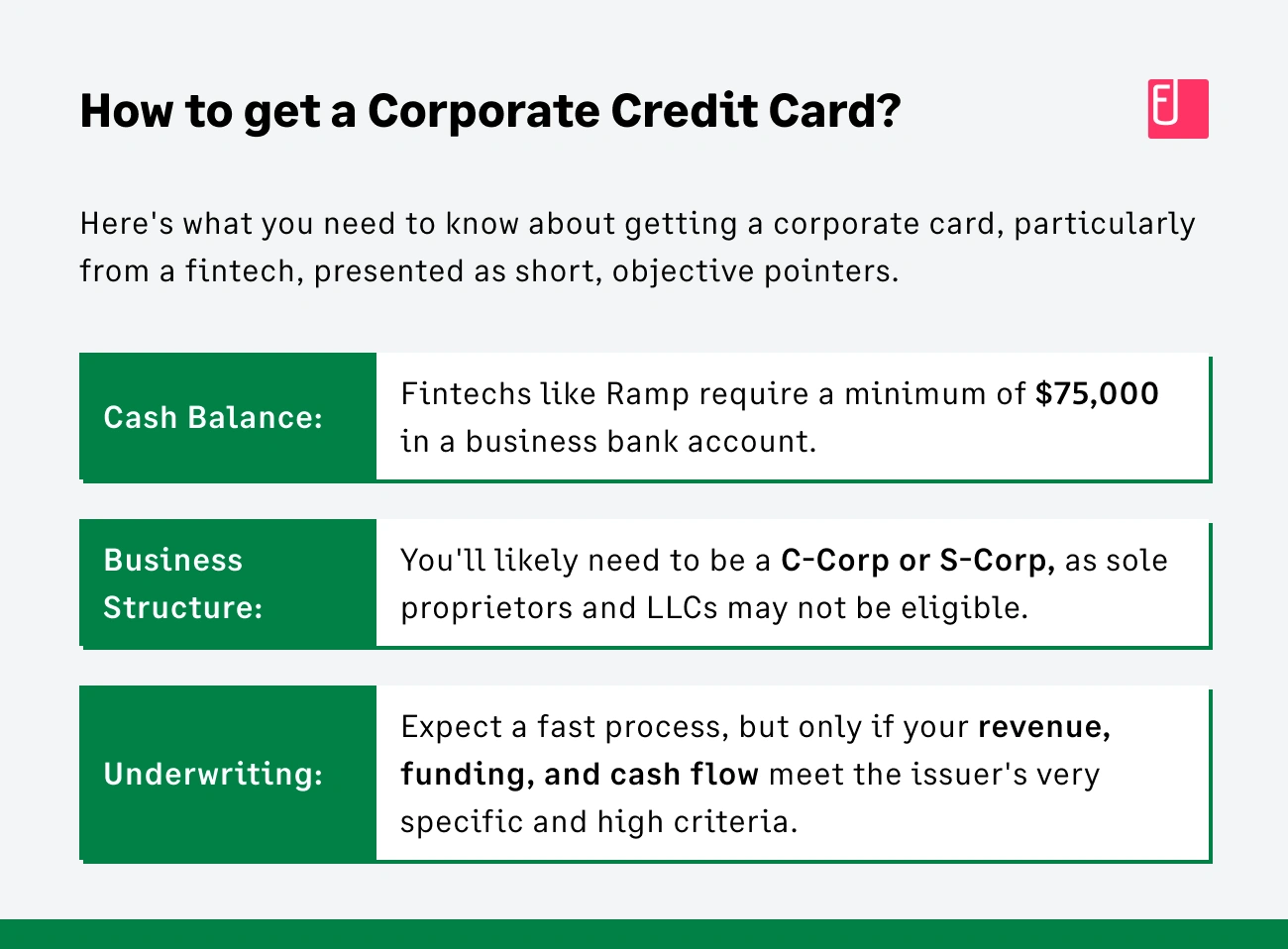

Check If You Meet The Minimum Cash Balance

For a large segment of SMBs, a significant hurdle is the requirement to have a substantial cash balance in a U.S. business bank account. For example, Ramp often requires a business to have at least $75,000 in cash. For a startup or a growing business with tight cash flow, this is a non-starter and immediately disqualifies them from the program.

Confirm Your Business Structure

Ramp and other fintechs often require a specific business structure. They typically serve corporations, such as C-corps and S-corps, and exclude a large portion of the market that operates as sole proprietorships or LLCs. This narrow focus immediately limits the accessibility of these cards to many entrepreneurs and small business owners.

Provide Extensive Financial Documentation

The underwriting process for these cards is often marketed as "fast," but that speed is contingent on meeting very high, very specific financial criteria. You'll be asked to provide detailed information about your business's revenue, funding, and cash flow. Unlike a traditional bank that may offer a small credit line to a business with less capital, fintechs use these high-bar metrics to assess risk, effectively locking out the average SMB.

How to Implement a Corporate Credit Card Program?

Once you've chosen the right card, a successful implementation is key. Here is a step-by-step guide to rolling out your new program:

- Choose the Right Card: Based on your needs, choose a bank-issued business credit card that offers competitive rates and a reward program that aligns with your spending habits.

- Establish a Clear Spend Policy: Before you hand out cards, create a clear, comprehensive spend policy that outlines what employees can and cannot spend money on.

- Communicate the Policy to Employees: Hold a meeting or send a company-wide email to ensure every employee understands the new policy and their responsibilities.

- Set up an Expense Management System: A card is just a tool. To get the most out of it, you need a system to manage the expenses. Set up a modern platform that automates the process of collecting receipts and reconciling accounts.

- Provide Proper Training: Train your employees on how to use the new card and the expense management system. Make it clear that using the system is a mandatory part of their job.

Benefits of Corporate Credit Cards

A corporate or business credit card, when used correctly, is invaluable for your business. It allows you to:

- Streamline Spending: Keep business and personal expenses completely separate, making accounting and tax preparation much easier.

- Improve Cash Flow: Use a line of credit for purchases, allowing you to pay for things without immediately drawing on your business bank account.

- Enhance Reporting: Use the card's transaction data to simplify expense tracking and reporting, giving you a clear picture of where your money is going.

- Earn Rewards: Earn cash back or points on business purchases, turning your daily spending into a profit center.

Why Fintech Corporate Credit Cards Don’t Work for Most Businesses

Despite their appeal, fintech corporate cards are not a viable option for the vast majority of small and mid-sized businesses. This is often due to a fundamental mismatch between the fintech's business model and the needs of a typical SMB.

Strict Underwriting Criteria

Fintechs often rely on venture capital funding and a business model that prioritizes rapid growth from high-value customers.

This leads them to set extremely strict underwriting criteria that many SMBs cannot meet. For example, to even qualify for a card, many fintechs require a business to have a cash balance of at least $75,000 in a U.S. business bank account and at least $250,000 in annual revenue.

This creates a paradox: the smallest, fastest-growing businesses—the ones who need modern spend control the most—are often the very ones who are immediately disqualified.

Business Model Mismatch and Pivots

The fintech business model is often built on serving a specific, high-growth market, but this strategy can be unsustainable for long-term customer relationships. As mentioned in a TechCrunch article, a prominent fintech like Brex, which initially targeted startups, made a strategic pivot to focus on enterprise clients because its model was not a sustainable fit for smaller customers.

This pivot left many small businesses without a financial partner, demonstrating the risk of relying on a fintech whose priorities may change. Other fintechs have faced similar challenges with customer acquisition and underwriting for the heterogeneous SMB market, often finding it more difficult and expensive than serving larger, more predictable clients.

Why Banks Hold an Advantage Against Fintechs

While fintechs have made a splash with their modern interfaces and features, traditional banks still hold the advantage in the corporate card space, especially for the small and mid-sized business (SMB) market.

Stability and Reliability

Traditional banks have been serving businesses for decades, building a foundation of trust and stability. They are not beholden to the same venture capital pressures as many fintechs, whose business models can change or even fail. This long-term reliability is crucial for businesses that need a financial partner they can grow with, as highlighted in a J.D. Power study that found small business satisfaction is highest when there's trust and a consistent financial relationship.

Accessibility

Banks offer a wider range of credit products with more flexible underwriting criteria, making them more accessible to a broader range of businesses, from freelancers to mid-market companies. Unlike fintechs that may require high cash balances or specific business structures, banks are more likely to approve a credit line for a business with a proven track record, even if their cash flow is tight.

Why Choose Business Credit Cards over Fintech Cards?

A More Accessible Solution

For the majority of small and mid-sized businesses, a traditional business credit card is a more accessible and suitable solution. It provides the credit you need to manage cash flow and make purchases without the strict, often exclusionary requirements of a fintech corporate card, which can be a non-starter for many businesses.

Leveraging Existing Relationships

For a business, building and leveraging a long-term relationship with a stable financial institution is invaluable. This relationship can lead to better interest rates, more flexible financing options as your business grows, and a deeper understanding of your business's needs from a partner that has a vested interest in your success.

Sage Expense Management (formerly Fyle) Works with any Business Credit Card

The core problem is that you need a modern expense management platform but you don't want to be locked into a fintech's strict requirements.

Sage Expense Management solves this by working with every business credit card. This allows you to use a card you can actually get approved for while still getting all the benefits of real-time spend control and automation.

Real-time Spend Control

Sage Expense Management gives your finance team real-time visibility and control over spending. The moment an employee swipes their credit card card, it notifies them to submit a receipt via text. This means you know exactly where your money is going as it's spent, not weeks later.

Automated Expense Management

Sage Expense Management's AI-powered expense reporting and receipt management automates the grunt work of reconciliation and ensures data accuracy. It eliminates the need for manual data entry and makes your books audit-ready at all times.

No Card Switch Needed

You get all of this without the friction, cost, and disruption of a new program. Sage Expense Management works with your existing cards, allowing you to get a modern expense management system without changing your banking relationship.

The Smarter Choice for Businesses

The best corporate card program isn't about the card itself; it's about the platform you use to manage it. By choosing a stable, traditional bank for your credit card and a modern, agile platform like Sage Expense Management, you get the best of both worlds.

This approach provides the long-term reliability and credit you need, while also offering real-time visibility and automated expense management. It's the smart choice for any business that wants to grow without the headaches of an outdated financial system.