.webp)

With over 50% of the world's population owning and using a mobile device, cell phone use has become second nature to most.

From checking emails and sending text messages to hosting video conferences, many professionals rely on cell phones as their mobile office. If you're a business owner running a successful company, chances are you have multiple employees using their mobile devices for work.

How much of that money are you required to pay back? What personal cell phone use is considered "work-related"? And how do you measure these factors? Here we'll break down the newest laws in cell phone reimbursement and how to guarantee both you and your employees are getting a fair deal.

What Is a Cell Phone Reimbursement?

A cell phone reimbursement is money an employer provides to employees to compensate them for using their personal cell phones for work-related purposes. This can include costs like monthly service plans, data usage, and even the phone itself in some cases.

Essentially, it’s a way for companies to acknowledge that employees are using their personal devices for business needs and to offset those expenses.

The rise of remote work and the increasing reliance on mobile technology have made cell phone reimbursements a standard perk for many employees. It’s a recognition that in today’s digital age, employees often blur the lines between personal and professional life, and their phones are essential tools for both.

The Importance Of A Clear Cell Phone Reimbursement Policy

A well-defined cell phone reimbursement policy is crucial for both employers and employees. For employers, it provides a clear framework for managing expenses, preventing disputes, and ensuring compliance with tax laws. For employees, it guarantees fair compensation for work-related phone usage and outlines expectations.

A clear policy can prevent misunderstandings about:

- What expenses are covered

- How reimbursements are calculated

- The required documentation for reimbursements

It also helps in maintaining a consistent approach across the company, ensuring equitable treatment for all employees.

Without a structured policy, employers risk potential legal issues, such as wage and hour disputes. Employees might feel undervalued or unfairly compensated, leading to decreased morale and productivity.

Are Cell Phone Reimbursements Taxable by the IRS?

The taxability of cell phone reimbursements can be a complex issue, but the good news is that the IRS offers clear guidance. Here’s a breakdown of what you need to know:

To summarise: Reimbursements for business-related cell phone use are generally considered non-taxable for employees, as long as they employer follows specific guidelines.

Also Read:

Key Factors for Non-Taxable Reimbursements

Substantial Non-Compensatory Business Reasons

The employer must have a legitimate business reason for requiring employees to use their personal phones, not just to provide a perk. Examples include:

- Need to contact employees for emergencies

- Requiring employees to be available to clients outside the office

- Facilitating communication across time zones

Accountable Plan

The employer should have a written cell phone reimbursement policy outlining the process for submitting and receiving reimbursements. Employees must be required to return any unused or excess funds.

Tax Treatment Breakdown

Working Condition Fringe Benefit

If the above conditions are met, the IRS considers the reimbursement's business-related position a working condition fringe benefit. This means it’s excluded from the employee’s taxable income.

De Minimis Fringe Benefit

The IRS also considers any minimal personal use of the phone as a de minimis fringe benefit, meaning its too small to be worth tracking for tax purposes. However, this applies only to truly minimal personal use.

Important Note: This guidance from Notice 2011-72 applies specifically to employer-provided cell phones or reimbursements. Don't assume the same rules apply to other types of fringe benefits.

Seeking Professional Help: While the IRS provides clear guidelines, consulting with a tax professional ensures your company's cell phone reimbursement policy fully complies with regulations and avoids potential tax penalties.

Laws for Cell Phone Reimbursement

Offering cell phone reimbursement isn't just about being a kind-hearted boss. There are actually laws surrounding what employees are entitled to when it comes to compensation for personal cell phone use. Some even compare it to unauthorized overtime.

These laws protect both employees and employers. Without a stipend, staff members can sue their employers for associated costs. On the other hand, employees may be liable for compromising secure company information.

While these laws vary from state to state, California is leading the way in this growing trend. These changes followed a controversial court case: Cochran vs. Schwan's Home Services.

The Cochran vs. Schwan's Home Services Case: A Landmark Decision

The landscape of cell phone reimbursement laws has been significantly influenced by the Cochran vs. Schwan's Home Services case. This landmark legal battle unfolded in California, a state at the forefront of employee protection in this area.

The Case

The lawsuit was a class-action suit filed by 1,500 customer service managers who claimed they were not reimbursed for expenses incurred while using their personal cell phones for work-related tasks. Essentially, employees argued that they were shouldering costs that should be borne by the company.

The Ruling

The California Court of Appeals sided with the employees, setting a precedent with far-reaching implications. The court determined that:

- Mandatory reimbursement: Even if an employer permits personal cell phone use for work, employees must be reimbursed for any expenses incurred for work-related activities.

- Reimbursement for unused minutes: A particularly controversial aspect of the ruling is that employees are entitled to reimbursement even if they have unlimited minutes or data. The rationale is that the company benefits from the employee's availability.

- Reasonable percentage: While the court-mandated reimbursement didn't specify a precise percentage, this ambiguity has created challenges for employers in determining a fair amount to pay.

Impact on Employers

This case has placed a considerable burden on employers, forcing them to carefully consider their cell phone reimbursement policies. The uncertainty around what constitutes a "reasonable percentage" has made it difficult to comply with the law without incurring excessive costs.

The Cochran vs. Schwan's Home Services case serves as a stark reminder that companies must have clear and compliant cell phone reimbursement policies to avoid legal repercussions.

Creating a Cell Phone Reimbursement Policy

With so many different laws and unclear expectations, how can companies create a compliant, reasonable cell phone reimbursement policy?

Some are even banning cell phones in the workplace to avoid the risk and complications associated with creating policies and stipends. The downside is that this could potentially impact employee productivity and company morale.

Instead of resigning yourself to being "damned if you do and damned if you don't," let's see how you can create a cell phone reimbursement policy that doesn’t speak debate but is reasonable and catered to the needs of your organization.

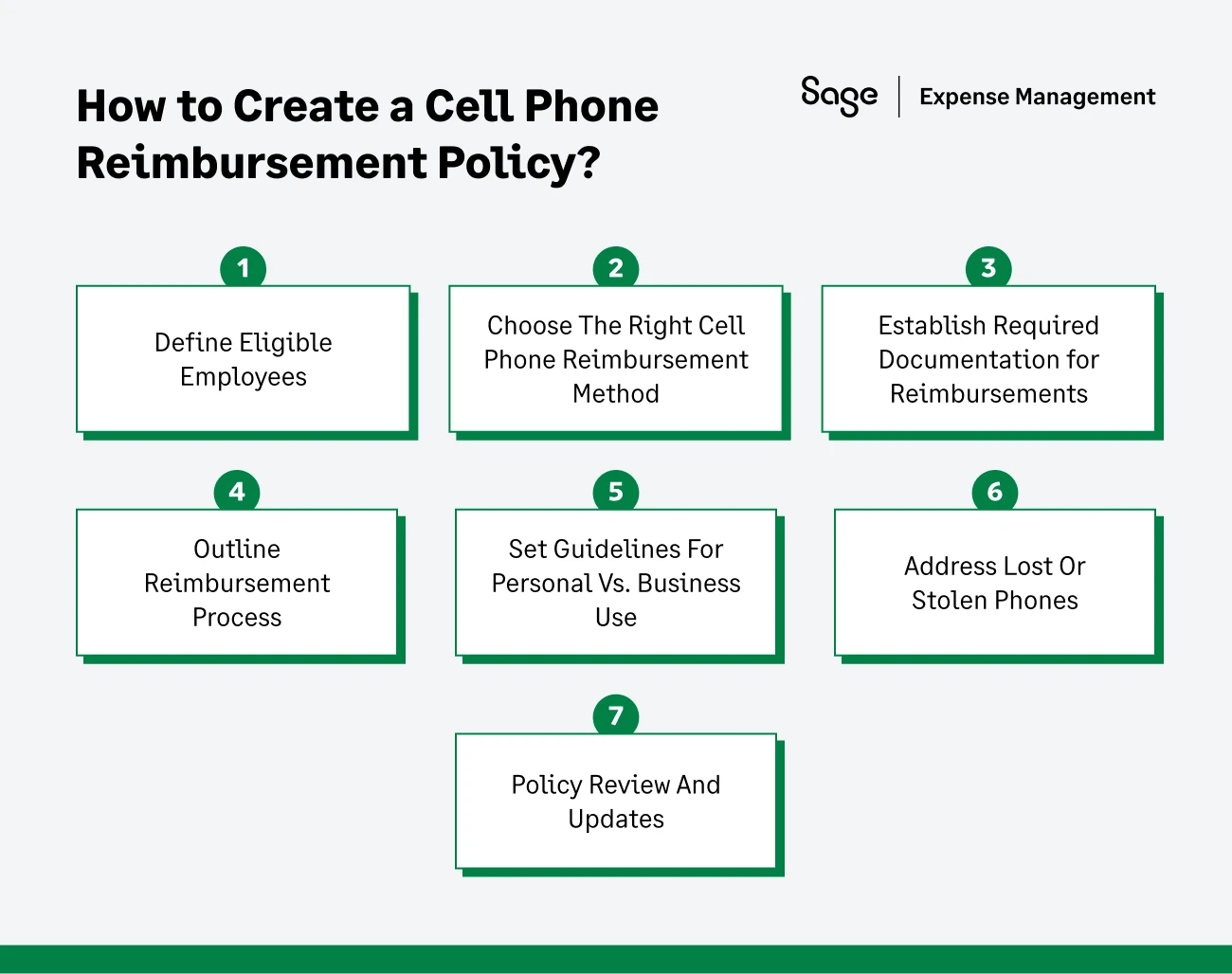

Define Eligible Employees

The first step in crafting your cell phone reimbursement policy is to determine who qualifies for reimbursement. Consider factors like job roles, departments, and level of responsibility. While it might seem fair to offer reimbursement to all employees, it’s essential to evaluate the actual business need for cell phone use.

For instance, sales representatives who spend a significant time on the road might have a stronger case for reimbursement than office-based employees.

Clearly outlining which employees are eligible will prevent misunderstandings and disputes down the line.

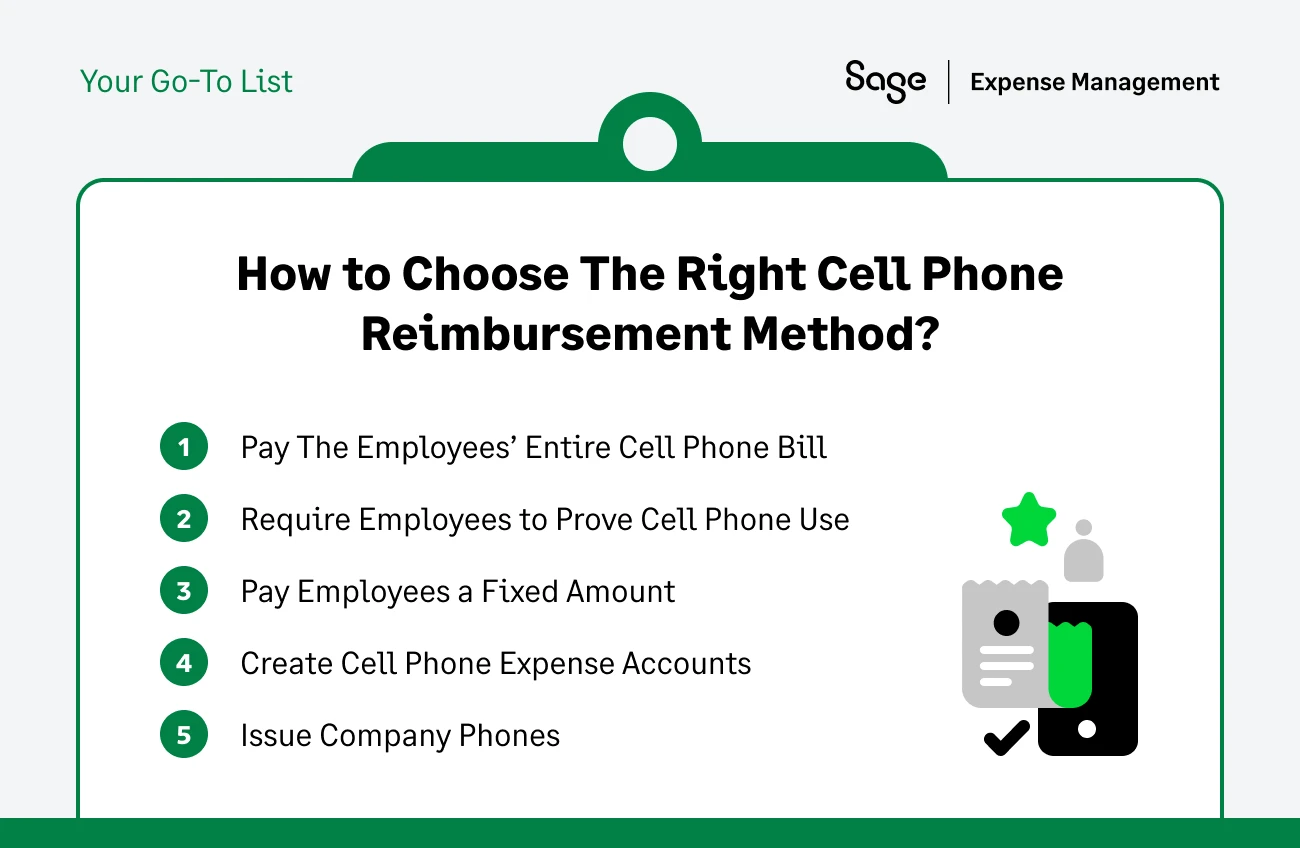

Choosing The Right Cell Phone Reimbursement Method

Once you’ve defined eligible employees, the next step is to decide on the reimbursement amount and how often it will be paid. Here are the different types of cell phone reimbursements:

Pay The Employees’ Entire Cell Phone Bill

While this is an unpopular solution for many employers, for some, it's more about peace of mind. By simply paying for your staff's cell phone bills, you're sidestepping any sticky legal issues or long, drawn-out debates over percentages.

Pros

- Simplicity: Easy to administer.

- Employee satisfaction: Employees appreciate the full coverage.

Cons

- High cost: This can be expensive for the company, especially with a large workforce.

- Lack of control: No oversight of phone usage.

Require Employees to Prove Cell Phone Use

The proof is in the pudding, and many employers want to see exactly what their employees are claiming as work-related expenses. In this situation, companies create a policy that requires staff to prove any work-related cell phone usage and expenses. As you can imagine, this approach gets quite tedious and time-consuming.

Pros

- Cost-effective: Employers pay only for business-related expenses.

- Accuracy: Ensures precise reimbursement.

Cons

- Time-consuming: Requires extensive documentation and tracking.

- Administrative burden: Increased workload for both employees and HR.

- Potential disputes: Disagreements may arise over what constitutes business use.

Pay Employees a Fixed Amount

Simply paying employees a fixed amount is a viable option for companies looking to cut administrative costs. But remember, employees must agree on this amount, and it should be clearly outlined in the policy.

Pros

- Simplicity: Easy to administer and budget.

- Predictability: Consistent costs for the company.

Cons

- Inaccuracy: This may not accurately reflect actual expenses.

- Potential for dissatisfaction: Employees might feel undercompensated.

- Legal risks: This could lead to legal issues if not structured carefully.

Create Cell Phone Expense Accounts

Expense accounts are commonplace in larger corporations that require employees to travel and network as part of their job description. Why not lump cell phone use under the umbrella of expense accounts?

This means employees are paid for their exact amount of work-related personal cell phone use — to the penny. This places responsibility on the employee.

Pros

- Accuracy: Precise reimbursement for actual expenses.

- Employee satisfaction: Employees are compensated fairly.

Cons

- Administrative burden: Requires detailed expense reports.

- Potential for fraud: Increased risk of false claims.

- Time-consuming: Requires careful review and approval of expenses.

Issue Company Phones

This is a popular option for a wide range of companies. Providing employees with a company cell phone means the expenses are already calculated.

Pros

- Cost control: Employer manages phone expenses.

- Data security: Better control over company data.

- Employee equipment: Provides necessary tools for work.

Cons

- High upfront costs: Purchasing phones for all employees can be expensive.

- Replacement costs: Risk of damage, loss, or theft.

- Employee preference: Some employees may prefer personal phones.

The optimal reimbursement method depends on various factors, including company size, budget, industry, employee roles, and administrative resources. To select the most suitable approach for your organization, it's essential to carefully consider the pros and cons of each option.

Also Read:

Establish Required Documentation for Reimbursements

To ensure accurate and fair reimbursements, it’s essential to establish clear documentation requirements. This might include:

- Detailed cell phone bills: These can provide evidence of expenses.

- Usage logs: Employees can track work-related calls, texts, and data usage.

- Receipts for phone-related purchases: This can cover accessories or phone upgrades.

Outline Reimbursement Process

A well-defined reimbursement process is crucial for efficient administration. Define clearly, the steps involved, including:

- How employees should submit reimbursement requests

- Required documentation

- The approval process

- Payment methods and timelines

Also Read:

Set Guidelines For Personal Vs. Business Use

Establishing clear guidelines for personal versus business cell phone use is essential to prevent disputes and ensure fair reimbursements. Consider the following:

- Define business use: Clearly outline what constitutes work-related phone use. This might include work-related calls, emails, texts, and data usage.

- Implement usage policies: Set expectations for personal phone use during work hours, such as limiting personal calls or texts.

- Consider phone monitoring: In certain industries or roles, monitoring phone usage might be necessary to protect sensitive company information. However, it’s crucial to balance monitoring with employee privacy concerns.

- Educate employees: Clearly communicate the policy to all employees, emphasizing the importance of distinguishing between personal and business use.

Address Lost Or Stolen Phones

Losing or having a phone stolen is an unfortunate reality. Your policy should outline the company’s stance on replacing lost or stolen phones:

- Employee responsibility: Make it clear that employees are generally responsible for replacing lost or stolen phones.

- Insurance coverage: Encourage employees to have insurance for their phones.

- Company-provided phones: If you provide company phones, outline the replacement process and any potential costs to the employee.

Policy Review And Updates

Cell phone technology and reimbursement practices have evolved over time. Your policy must be regularly reviewed and updated to ensure it remains relevant and compliant with changing laws and regulations. Consider conducting annual policy reviews or updating the policy when significant changes occur.

How to Successfully Implement Cell Phone Reimbursement Policy?

There's no one-size-fits-all approach to cell phone reimbursement for employees, and some businesses may decide to opt for a virtual business phone system with a virtual phone number instead. Virtual business phone systems often make the company's internal and external communications much easier.

Employers must protect their legal interests, as well as their integrity. Here are a few things to keep in mind when considering what type of cell phone reimbursement policy is best for your business:

Calculate Cost

As with most things in life, it comes down to money.

- Factor in all expenses: Consider the potential costs of each reimbursement option, including administrative overhead, potential employee dissatisfaction, and the overall financial impact on the company.

- Compare options: Weigh the costs and benefits of different reimbursement methods to determine the most financially viable solution for your business.

- Long-term perspective: Consider the potential future costs and benefits of each option when making your decision.

Sit down and crunch numbers before you settle on a solution.

Create an Easy to Understand Cell Phone Reimbursement Policy

Whatever expense reimbursement policy you craft, make sure the guidelines are abundantly clear.

- Clear and concise language: Use simple terms that are easy for employees to understand.

- Detailed guidelines: Outline specific expectations for eligible employees, reimbursement amounts, required documentation, and the reimbursement process.

- Employee access: Ensure the policy is easily accessible to all employees.

Also Read:

How Can Sage Expense Management (formerly Fyle) Help With Cell Phone Stipends?

In today's fast-paced world, everybody is dependent on phones for the majority of the day. It's no surprise that cell phone reimbursement has become a hot topic.

Yet, the question remains: How much of that is for personal use, and how much is work-related? Companies across the globe are trying to answer this question.

Here’s where we come in. Sage Expense Management can automate the entire expense reimbursement process, from creating clear expense policies to submitting expense claims to actually reimbursing your employees!

Schedule a demo today, and let's get started!

{{expense-reimbursement="/cta-banners"}}

FAQs Around Cell Phone Reimbursement

What are Bring Your Own Device (BYOD) Policies?

BYOD, or bring your own device, policies are becoming more common in work environments. Under these policies, many employers are paying anywhere from $30 to $50 per month toward employee cell phone bills. This figure varies depending on the company and the agreed-upon policy.

These payments are referred to as mobile stipends. Employers consider several factors when drafting accountable policies for candidate reimbursement and determining stipend amounts. Here are just a few:

- Carrier fees

- Mobile management overhead

- New device purchases

- Mobile expense management software

But these BYOD policies cover much more than cell phone bills. They also address security measures that keep the information of both the employee and the company safe and confidential.

How Much Should I Reimburse Employees For Cell Phone Use?

The amount you reimburse employees for cell phone use depends on various factors:

- Industry: Industries with high levels of client interaction often have higher reimbursement rates.

- Employee role: Employees with frequent business calls or data usage might require higher reimbursements.

- Company budget: Your financial resources will influence the amount you can allocate.

- Reimbursement method: The total cost will be affected by whether you offer a flat rate, percentage-based, or actual expense reimbursement.

Can I Deduct Cell Phone Reimbursements As A Business Expense?

Generally, if you meet specific criteria, you can deduct cell phone reimbursements as a business expense. These criteria include:

- The reimbursement is for business-related expenses.

- Employees provide adequate documentation.

- The reimbursement is part of an accountable plan (employees return any excess funds).

It's advisable to consult with a tax professional to ensure compliance.

{{find-an-accountant="/cta-banners"}}

What If An Employee Loses Their Phone?

Your policy should outline who is responsible for replacing a lost phone. Generally, employees are responsible for replacing their own phones. However, you might consider providing insurance options or stipulating conditions under which the company would replace the phone.

Can I Reimburse Employees For Phone Accessories?

Whether or not to reimburse employees for phone accessories is a company decision. If you choose to do so, clearly outline which accessories are eligible for reimbursement and any limits or restrictions.

Do I Need A Written Cell Phone Reimbursement Policy?

Having a written cell phone reimbursement policy is highly recommended. A written policy provides clarity to both employees and the company, prevents misunderstandings, and helps ensure compliance with tax laws and regulations.