.webp)

Key Takeaways

- An LLC is a state-law entity, but the IRS taxes it as a sole proprietorship, partnership, or corporation depending on member count and elections made.

- Any expense that is "ordinary and necessary" for your trade or business is generally deductible under IRC Section 162.

- The 2025 standard mileage rate is 70 cents per mile; the Section 179 deduction limit is $2.5 million; and 100% bonus depreciation is back for qualified property acquired after January 19, 2025.

- The de minimis safe harbor lets you immediately deduct asset purchases up to $2,500 per item ($5,000 with an applicable financial statement).

- Records must be kept for at least 3 years, and 7 years for bad debt or worthless securities deductions.

- Personal expenses, fines, lobbying costs, political contributions, and entertainment expenses are never deductible.

Navigating tax-deductible expenses can be daunting, especially for LLC owners seeking to maximize tax benefits while maintaining financial stability.

This cheat sheet covers all the essentials on what LLC expenses qualify for deductions, what's off-limits, and the best way to manage these expenses efficiently.

By the end, you'll have a comprehensive understanding of what you can deduct, common expense categories, and how to make expense tracking a breeze. All figures referenced are for the 2025 tax year unless otherwise noted; verify current-year amounts with the IRS or your tax advisor before filing.

How Does the IRS Define an LLC?

How Does the IRS Define an LLC?

A Limited Liability Company (LLC) is a flexible business structure created under state law that protects owners (called "members") from personal liability for business debts. The IRS does not recognize "LLC" as a federal tax classification — instead, an LLC is taxed as a disregarded entity, partnership, or corporation based on member count and elections filed.

This distinction matters because how your LLC is taxed determines which forms you file, what deductions are available, and how income flows to you. The IRS provides full guidance on entity classification here.

Single-Member LLCs (Disregarded Entities)

By default, a single-member LLC is treated as a "disregarded entity" — meaning the IRS ignores the LLC for tax purposes and taxes the owner directly.

The owner reports business income and expenses on Schedule C (Form 1040), the same form sole proprietors use. Self-employment tax applies on net earnings of $400 or more, per IRS Publication 334.

Multi-Member LLCs (Partnerships by Default)

LLCs with two or more members are taxed as partnerships by default. The LLC files Form 1065, and each member receives a Schedule K-1 reporting their share of income, deductions, and credits.

Members then report their K-1 amounts on their personal returns. The LLC itself pays no federal income tax — all profit and loss passes through to the members.

LLCs Electing Corporate Taxation

An LLC can elect to be taxed as a C corporation by filing Form 8832, or as an S corporation by filing Form 2553.

Owners often make the S-corp election to reduce self-employment tax on a portion of business profits. This election comes with payroll, "reasonable salary," and recordkeeping requirements that don't apply to default LLC taxation.

Restrictions on LLC Tax Classification

Not every business can operate as an LLC — banks and insurance companies are common exclusions, and foreign-owned LLCs face additional IRS reporting under Form 5472.

There's also a "60-month limitation" rule: once an LLC changes its tax classification, it generally cannot change again for five years (per Form 8832 instructions).

What Are Tax-Deductible Business Expenses?

Tax-deductible business expenses are the ordinary and necessary costs of carrying on a trade or business. Under IRC Section 162, an "ordinary" expense is one that is common and accepted in your industry, while a "necessary" expense is one that is helpful and appropriate for your business — it does not need to be indispensable.

The IRS allows these expenses to be subtracted from gross income, reducing taxable income and ultimately your tax liability.

These expenses should align directly with business needs, though some are only partially deductible depending on use. The full framework is explained in IRS Publication 334, which is the current guide for small businesses filing Schedule C.

Examples of Common Tax-Deductible Expenses

Here are several examples of typical LLC business expenses eligible for deductions:

- Employee wages and salaries: compensation paid to employees for their services.

- Rent or lease payments: costs associated with renting or leasing property for business purposes.

- Utilities: charges for electricity, water, and gas related to business premises.

- Insurance premiums: business insurance, including liability, property, and workers' compensation.

- Loan interest: interest on business loans, such as those for purchasing equipment or financing operations.

- Depreciation on business assets: spreading out the cost of significant purchases, like equipment or property, over their useful life.

- Taxes and licenses: costs associated with regulatory compliance, including license fees.

The IRS distinguishes between regular business expenses, Cost of Goods Sold (COGS), and capital expenditures. Unlike regular business expenses, capital expenses involve long-term assets (vehicles, property, major equipment) that must be depreciated over time rather than deducted in the year purchased.

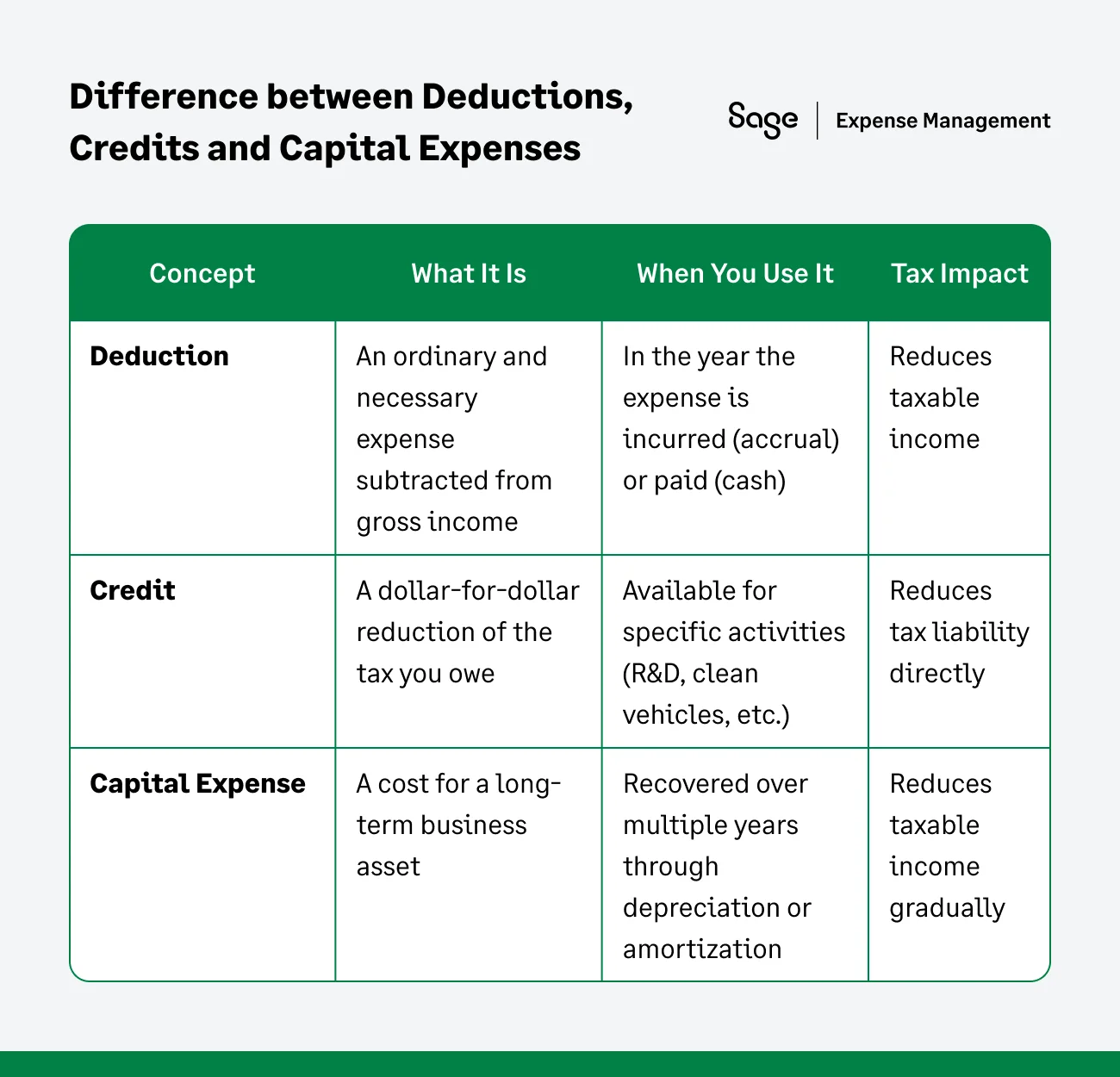

The Difference Between a Deduction, a Credit, and a Capital Expense

Understanding the distinction between these three is one of the most common sources of confusion for LLC owners. The table below summarizes the difference:

A $1,000 deduction at a 24% tax rate saves you $240. A $1,000 credit saves you the full $1,000. A $1,000 capital expense saves you tax over several years rather than all at once.

When Can I Deduct an Expense?

The timing of when you can deduct an expense depends on your accounting method. Under the cash method, you deduct expenses when paid; under the accrual method, you deduct them when incurred. Your method must be applied consistently and clearly reflect your income.

The IRS covers accounting periods and methods in detail in Publication 538 and Chapter 2 of Publication 334.

Accounting Methods Explained

Most small LLCs use either the cash or accrual method. A "small business taxpayer", one with average annual gross receipts of $31 million or less for 2025, generally has flexibility to use either, per IRS Publication 334.

Cash Accounting

The cash method allows you to deduct business expenses in the year they're paid. For example, if you pay for supplies in December, you can deduct the expense in that same tax year.

This method is straightforward and matches when money actually leaves your account. Most single-member LLCs and small service businesses use it.

Accrual Method

Under the accrual method, expenses are deducted when they're incurred, regardless of when they're paid. This method follows two IRS rules:

- All-events test: all events establishing the liability have occurred and the amount can be reasonably determined.

- Economic performance: the service has been rendered or the product received.

Example: A repair company services your office building in December 2024 and bills you $600, but you pay in January 2025.

- Cash method: you'd deduct the expense in 2025 when payment was made.

- Accrual method: you'd deduct the expense in 2024, since the service was performed then.

Hybrid Method

The hybrid method combines elements of cash and accrual accounting. A common example is using the accrual method for purchases and sales (where inventory is involved) while using the cash method for everything else.

The IRS permits this only if the combination clearly reflects income and is applied consistently. Specifics are detailed in Publication 538.

A Complete List of Tax-Deductible LLC Business Expenses

Below are 30 of the most common deductions available to LLCs in 2025, grouped by category. Each entry notes what's deductible, the relevant IRS source, and any limits or caveats LLC owners frequently miss.

1. Rent or Mortgage

Rent paid for business property is deductible if it meets the IRS's "reasonable rent" standard, particularly if paid to related parties.

Home-based LLCs can deduct a portion of rent or mortgage interest if there's a dedicated workspace used solely and regularly for business. Deduction eligibility extends to associated costs, such as property taxes and insurance, based on the percentage of your home used for business. See IRS Publication 587 for home office rules.

2. Utilities

Electricity, water, gas, and trash service costs related to business operations are deductible.

If you work from home, only the business-use portion is deductible, typically calculated as the percentage of your home used exclusively for business.

3. Office Supplies and Assets

Office supplies, stationery, cleaning supplies, paper towels, and printer ink that are consumed during the tax year can be deducted. If you keep incidental supplies on hand and don't track inventory precisely, you can typically deduct supplies purchased during the year.

The distinction between a deductible supply and a capitalized asset is crucial. Supplies are typically low-cost, short-lived items used up quickly. Office assets like land, buildings, machinery, furniture, patents, and franchise rights must generally be capitalized and recovered through depreciation or amortization.

What is The De Minimis Safe Harbor Election?

The de minimis safe harbor election lets businesses deduct the cost of small asset purchases immediately rather than depreciating them. With written accounting procedures in place, you can expense items costing up to $2,500 per invoice or item or $5,000 if you have an applicable financial statement (AFS).

This election is established under Treas. Reg. 1.263(a)-1(f) and is a powerful tool to simplify bookkeeping by avoiding depreciation calculations on small-dollar assets.

4. Maintenance and Repairs

The cost of incidental repairs that keep your business property in normal operating condition is fully deductible in the year incurred.

The key distinction is repair vs. improvement: repairs (fixing a broken window, patching a roof) are deductible currently, while improvements that add value, prolong useful life, or adapt the property to a new use must be capitalized and depreciated. The IRS tangible property regulations covers this in detail.

5. Printing

Business-related paper, ink, and other office supply costs, as well as printer repairs, qualify for deductions.

This includes the cost of printing marketing materials, business cards, invoices, and shipping labels.

6. Software

The cost of off-the-shelf software and subscription fees for cloud-based software (SaaS) are deductible.

For perpetual-license software purchased outright, depreciation rules may apply. SaaS subscriptions billed monthly or annually are typically deducted as ordinary business expenses in the year paid.

7. Internet

Domain registration, website hosting, and internet service fees are deductible if used for business purposes.

If you use the same internet connection for personal and business use, only the business-use portion is deductible.

8. Telephone

The cost of a dedicated business line is fully deductible.

For a personal phone used partly for business, you can deduct the business-use portion based on a reasonable allocation method, such as the percentage of business calls or business-use minutes per month.

9. Bank Fees and Service Charges

Ordinary and necessary bank fees on your business accounts are deductible.

This includes monthly maintenance fees, wire transfer fees, ATM fees on business cards, and stop-payment orders on business checks.

10. Payroll & Employee Wages

Wages, bonuses, and other compensation paid to employees are deductible, provided they are reasonable and for services actually performed. As the employer, you can also deduct employee benefits like retirement plan contributions, health insurance, and adoption assistance.

The "Reasonable" Test

Employee pay is considered reasonable if it reflects the true value of the work and is comparable to what others in the industry would be paid for the same job.

The IRS considers the employee's job duties, the complexity of the business, the individual's experience, and what similar businesses pay for similar roles when evaluating reasonableness.

The "For Services Performed" Test

You must be able to prove that payments were for services actually rendered to the business.

Maintain detailed records of timesheets, job descriptions, and performance reviews to substantiate that the work was performed and that compensation matched those services.

11. Employee Benefit Programs

Costs for qualified employee benefit programs are deductible as business expenses. These programs are designed to provide employees with benefits in addition to their wages.

Examples of these programs include:

- Group-term life insurance: premiums are deductible, provided you are not the direct or indirect beneficiary.

- Adoption assistance programs: financial assistance to employees for qualified adoption expenses.

- Dependent care assistance programs: help employees cover the costs of caring for dependents while at work.

12. Medical & Health Insurance Expenses

Self-employed LLC owners can deduct premiums paid for medical, dental, and qualified long-term care insurance for themselves, their spouse, and their dependents.

This deduction is taken as an adjustment to income on Schedule 1 (Form 1040) and is limited to the net profit from the business. Note: if your LLC has elected S-corp status, the more-than-2% shareholder rule applies, requiring health insurance premiums to be reported as wages on the shareholder's W-2 to remain deductible as per IRS guidance on S-corp shareholder health insurance.

13. Retirement Plan Contributions

Contributions you make to a qualified retirement plan for yourself or your employees are generally deductible as a business expense.

Common options for LLCs include the SEP-IRA, SIMPLE IRA, and Solo 401(k).

For 2025, the SEP-IRA contribution limit is the lesser of 25% of compensation or $70,000, and the Solo 401(k) employee deferral limit is $23,500 (or $31,000 if age 50+), per IRS retirement plan limits. Plan setup deadlines and contribution mechanics vary, so consult IRS Publication 560 before electing a plan.

14. Employee Education and Training

You can deduct the cost of education and training that maintains or improves skills required in your employees' current jobs, or that is required by law to keep their position.

This includes tuition, books, supplies, lab fees, and certain travel related to qualifying education. Employer-provided educational assistance under a written Section 127 plan is also excludable from employee wages up to $5,250 per year, per IRS Publication 970.

15. Licenses and Permits

Fees paid to state or local governments for licenses and permits required to operate your trade or business are deductible. This includes annual renewals.

However, significant costs for licenses that grant rights over a longer period may need to be capitalized and amortized rather than deducted immediately.

16. Legal and Professional Expenses

Fees paid to professionals like lawyers, accountants, consultants, tax preparers, bookkeepers are deductible if they are ordinary and necessary for operating your business.

Legal fees for forming the LLC are typically treated as organizational costs (see #25 below) rather than current-year deductions.

17. Business Insurance

Premiums for insurance that covers fire, theft, accident, liability, and workers' compensation are generally deductible. The premiums you pay for various types of business insurance are considered deductible because they are deemed ordinary and necessary for business operations.

Here's a more detailed look at the types of insurance premiums you can deduct:

- Property and casualty insurance: covers losses due to fire, theft, or other unforeseen events affecting your business property.

- Credit insurance: protects you from losses if a customer's business debt becomes uncollectible.

- Health and medical insurance: premiums for health coverage for your employees, including long-term care, are deductible.

- Liability insurance: safeguards your business against legal claims from damages or injuries caused by your business activities.

- Malpractice insurance: crucial for professionals; covers claims of professional negligence.

- Workers' compensation insurance: premiums for this mandatory insurance covering employee injuries are deductible.

- Unemployment insurance contributions: amounts contributed to a state unemployment fund are deductible if considered a tax under state law.

- Overhead insurance: covers business expenses incurred during a prolonged disability.

- Vehicle insurance: deductible for business vehicles. If used for both personal and business, only the business-use portion is deductible. If you use the standard mileage rate, you cannot deduct insurance premiums separately.

- Life insurance: you cannot deduct premiums if you are a direct or indirect beneficiary.

- Business interruption insurance: premiums are deductible, as it compensates for lost profits due to business disruptions.

You cannot deduct amounts you credit to a self-insurance reserve fund. You can only deduct premiums paid to a third-party insurance provider.

18. Marketing & Advertising

Marketing costs are deductible if they promote your business and are reasonable in nature.

This includes digital and print advertising, branding work, social media spend, content production, local sponsorships directly related to your business, and goodwill advertising that keeps your name before the public.

19. Dues and Subscriptions

You can deduct dues paid to professional organizations and trade associations related to your business.

This can include memberships in groups like bar associations, medical associations, or local chambers of commerce. Subscriptions to professional, technical, and trade journals in your business field are also deductible.

However, dues paid to clubs organized for business, pleasure, recreation, or other social purposes (country clubs, golf clubs, athletic clubs) are generally not deductible.

20. Bad Debts

A business bad debt is a loss resulting from a debt that becomes worthless and arises from your trade or business. This can include an uncollectible loan to a client or supplier for a business reason.

To claim a deduction, you must demonstrate that the debt is worthless and that you've taken reasonable steps to collect it. Cash-basis LLCs generally cannot deduct bad debts arising from unpaid invoices because the income was never reported in the first place the deduction effectively requires that the income was previously included.

This is distinct from bad debts from credit sales: business bad debts can also arise from loans made to suppliers, clients, or employees for business purposes that become uncollectible.

21. Business Trip Expenses

Ordinary travel expenses for employees and owners traveling away from their primary work location qualify as deductions. You are considered "away from home" if you are away from the general area of your tax home for a period substantially longer than an ordinary workday and need to sleep or rest to perform your duties.

The trip's primary purpose must be for business. Deductible travel costs include:

- Transportation: flights, trains, or buses between your home and business destination.

- Car expenses: the cost of operating and maintaining your car during the trip, including tolls and parking.

- Accommodation: lodging costs for business travel.

- Meals: generally deductible at 50%.

- Other essentials: taxis, rideshares, baggage fees, laundry, dry cleaning, and business phone calls.

The full rules are in IRS Publication 463. For 2025, the standard meal allowance (M&IE) for most U.S. localities is $68 per day, with high-cost localities at $86 per day under the high-low method.

22. Car & Vehicle Expenses

If you use your car for business, you can deduct expenses using one of two methods:

- Standard mileage rate: for 2025, the rate is 70 cents per mile for business use, per IRS Publication 463.

- Actual car expenses: the business-use portion of expenses such as gas, oil, repairs, insurance, depreciation, and license fees.

To support your deduction, you must maintain adequate records — a log showing the date of each business use, the mileage for each trip, the business purpose, and the total miles for the year.

Also Read

23. Business Meals

Business meals are 50% deductible if they are ordinary and necessary, not lavish or extravagant, and the taxpayer or an employee is present when the food or beverage is provided.

Entertainment expenses are no longer deductible following the Tax Cuts and Jobs Act of 2017. However, meals provided at an entertainment event can still be 50% deductible if they are purchased separately or stated separately on the receipt. This rule is established in Treas. Reg. 1.274-11.

Buying a client lunch at a restaurant: 50% deductible. Taking a client to a basketball game: not deductible. Buying hot dogs and drinks separately at the basketball game: the meals portion is 50% deductible.

24. Business Gifts

You can deduct the cost of gifts given to clients, customers, or employees, but the deduction is limited to $25 per recipient per year.

Incidental costs like packaging, engraving, or mailing do not count toward this limit unless they add substantial value. Exceptions to the $25 cap include:

- Promotional items costing $4 or less with your name permanently imprinted.

- Items like signs or display racks for the recipient's business premises.

These are not considered gifts and are not subject to the $25 limit, per IRS Publication 463.

25. Startup and Organizational Costs

The IRS allows you to deduct a portion of the costs incurred before you officially open your doors. These costs fall into two categories:

- Startup costs: expenses for creating an active business or investigating its creation or acquisition.

- Organizational costs: expenses related to forming a corporation, partnership, or LLC.

You can elect to deduct up to $5,000 for each category in the tax year your business begins. Any costs above this initial deduction must be amortized over 180 months (15 years). The deduction is reduced dollar-for-dollar if your total startup or organizational costs exceed $50,000.

Full guidance is in IRS Publication 535 with current-year treatment confirmed in Publication 334.

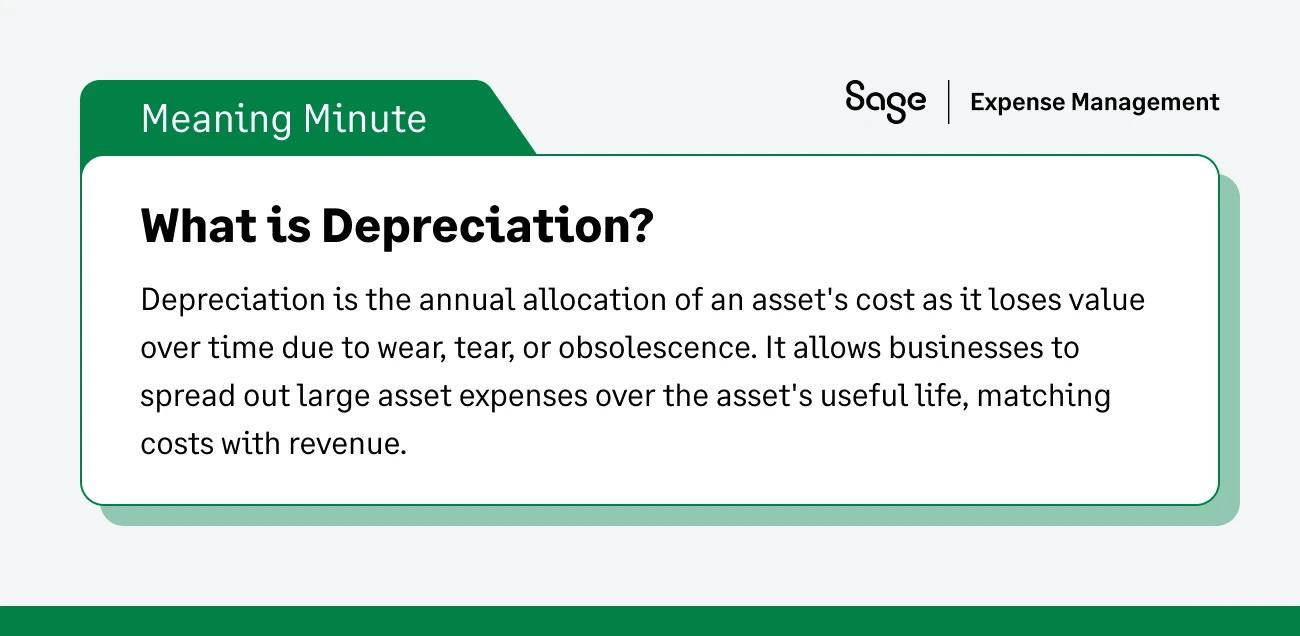

26. Depreciation

Depreciation is the process of gradually deducting the cost of tangible business assets that are expected to last more than a year. This method accounts for the asset's wear and tear or obsolescence over its useful life, rather than deducting the entire purchase price at once.

What Qualifies for Depreciation?

Depreciation applies to assets like buildings, machinery, equipment, furniture, and vehicles that are owned and used for business or to produce income.

Assets must have a determinable useful life. Land and inventory held for sale cannot be depreciated.

Depreciation Systems

The primary method used for most property is the Modified Accelerated Cost Recovery System (MACRS), which assigns assets to specific property classes with defined recovery periods.

Detailed MACRS tables and class lives are available in IRS Publication 946.

Special Deductions for Depreciation

- Section 179 deduction: allows businesses to deduct the cost of certain qualifying property in the year placed in service. For 2025, the deduction limit is $2.5 million, with a phase-out beginning at $4 million in total qualifying purchases (per Publication 946).

- Bonus depreciation: an additional first-year deduction. Following the One Big Beautiful Bill Act, 100% bonus depreciation is available for qualified property acquired and placed in service after January 19, 2025. Property acquired before that date but placed in service in 2025 is subject to the prior 40% rate.

Recordkeeping for Depreciation?

Stricter record-keeping rules apply to "listed property," such as passenger automobiles, due to their potential for personal use.

For 2025, the first-year depreciation cap for passenger autos with bonus depreciation is $20,200, dropping to $19,600 in year two. Consulting IRS Publication 946 is highly recommended for detailed guidance.

27. Amortization

Amortization is the method for deducting the capitalized cost of certain intangible assets over a set period, usually using the straight-line method. This is similar to depreciation, but applies to assets that lack a physical form.

This deduction applies to acquired Section 197 intangibles like goodwill, going-concern value, patents, copyrights, customer lists, franchises, and trademarks as well as costs of getting a lease and pollution control facilities. The amortization period is typically 15 years for Section 197 intangibles.

28. Depletion

If your business involves extracting natural resources like minerals, oil, gas, or timber, you can deduct depletion. Depletion is similar to depreciation but applies to natural resources, accounting for the using up of the resource as it is extracted and sold.

There are two primary methods, and you generally use whichever gives the larger deduction:

- Cost depletion: based on the unrecovered cost of the property and the number of units (tons of ore, barrels of oil) produced during the tax year.

- Percentage depletion: allows you to deduct a specific percentage of the gross income from the property, regardless of cost basis. Generally available for most minerals, oil, and gas, but not for timber.

29. Research and Experimental Costs

Research and experimental (R&E) costs are expenses a business incurs in developing a new product or improving an existing one. As of January 1, 2022, businesses can no longer elect to deduct these costs in the year incurred, they must be capitalized and amortized.

- Domestic research: costs for specified research conducted within the U.S. must be amortized ratably over a 5-year period.

- Foreign research: costs related to research conducted outside the U.S. must be amortized over a 15-year period.

This change, enacted by the Tax Cuts and Jobs Act, requires businesses to adjust their accounting for these expenses, moving from a direct deduction to a long-term amortization schedule. The IRS provides current guidance at 26 CFR § 1.174-2.

30. Charitable Contributions

For default LLCs (taxed as sole proprietorships or partnerships), direct charitable contributions are not deducted as business expenses — they pass through to members' personal returns and may be claimed as itemized deductions on Schedule A.

However, payments to charitable organizations may qualify as a business expense if they bear a direct relationship to your business and you can reasonably expect a financial return commensurate with the amount paid. For example, sponsoring a table at a charity event where you prominently advertise your business may qualify as marketing rather than a charitable contribution. LLCs taxed as C corporations follow corporate charitable contribution rules and deduct directly, subject to a 10% of taxable income limit.

Non-Deductible LLC Business Expenses

Some expenses are explicitly disallowed by the IRS, regardless of whether they support your business indirectly. Understanding these prevents costly errors and audit exposure.

The IRS prohibits deductions on certain expenses because they either don't support business operations directly or are illegal. These include:

- Bribes and kickbacks: payments made to gain a business advantage.

- Personal charitable contributions: for default LLCs, contributions flow to members' personal returns rather than the business deduction (unless they qualify as advertising or sponsorship with a business benefit).

- Demolition expenses: costs related to tearing down existing structures.

- Dues to social clubs: memberships for clubs unrelated to business (country clubs, golf clubs).

- Entertainment expenses: events, recreational activities, and related expenses (post-TCJA).

- Improvements: structural improvements or betterments to business property must be capitalized, not deducted.

- Lobbying expenses: payments for influencing legislation or government actions.

- Penalties and fines: payments to a government for violating any law.

- Personal, family, and living expenses: any non-business expenses.

- Political contributions: donations to political parties or campaigns.

- Settlements for sexual harassment or abuse: deducting settlements subject to nondisclosure agreements is prohibited under Section 162(q).

- Federal income taxes: the federal income tax itself is not a deductible business expense.

- Commuting: the cost of commuting between home and your regular workplace.

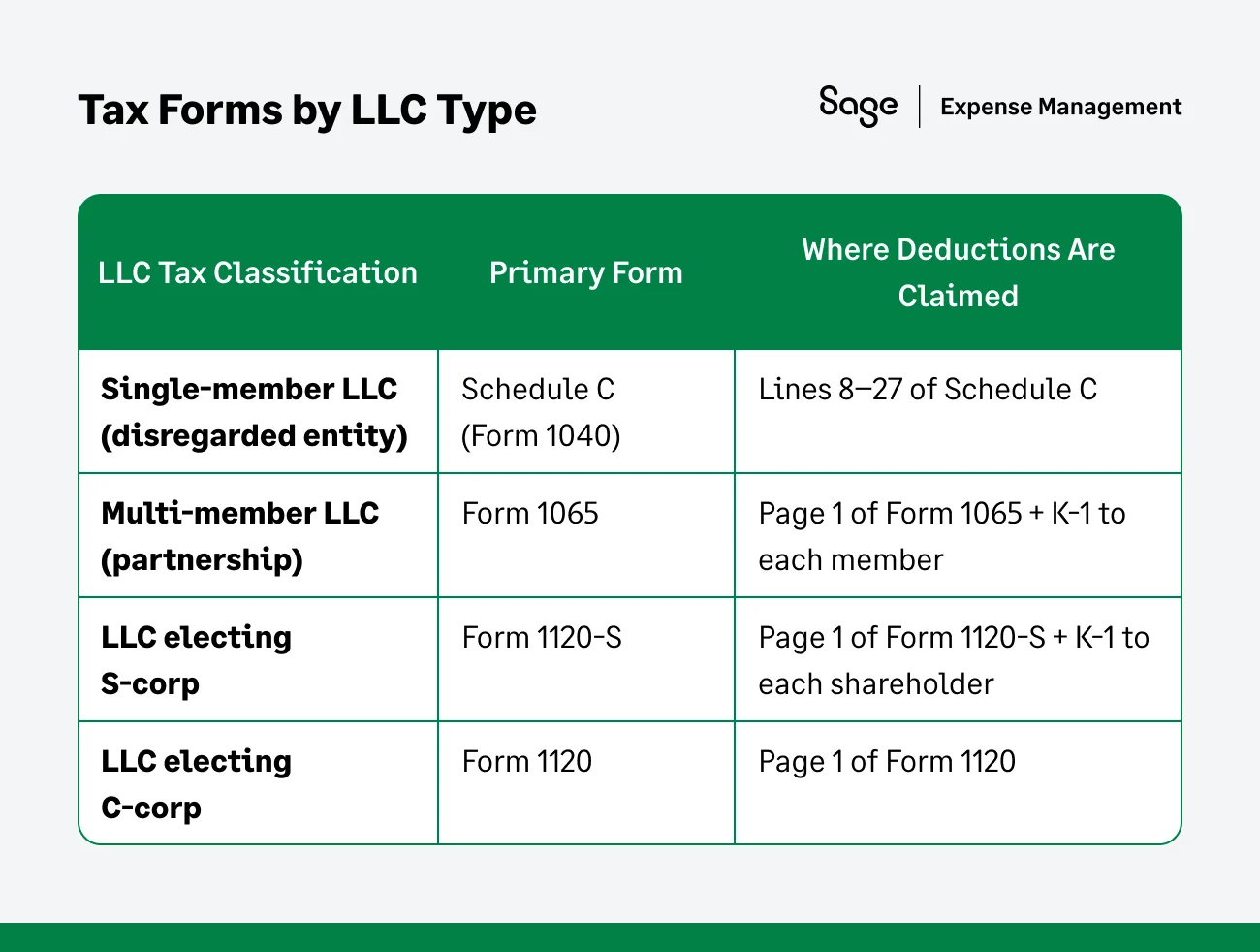

How Do You Actually Claim These Deductions?

How you claim LLC deductions depends on how your LLC is taxed. Single-member LLCs file Schedule C; multi-member LLCs file Form 1065 with K-1s; LLCs electing S-corp or C-corp status file Form 1120-S or Form 1120 respectively.

Knowing the right form is half the battle — the other half is having records that hold up if questioned.

Tax Forms by LLC Type

The table below maps each LLC tax classification to the form you'll file:

Forms and instructions are available at Forms & Instructions on the IRS Website.

What Records You Need to Substantiate Each Deduction

The IRS requires that records show five elements for most deductions: the amount, the time, the place, the business purpose, and (for travel and meals) the business relationship.

For non-lodging expenses under $75 and transportation expenses where a receipt isn't readily available, documentary evidence is not required, though a contemporaneous log is. Records must be kept for at least 3 years (7 years for bad debt deductions). The IRS explicitly accepts records prepared on a computer as adequate, per Publication 463 and Publication 583.

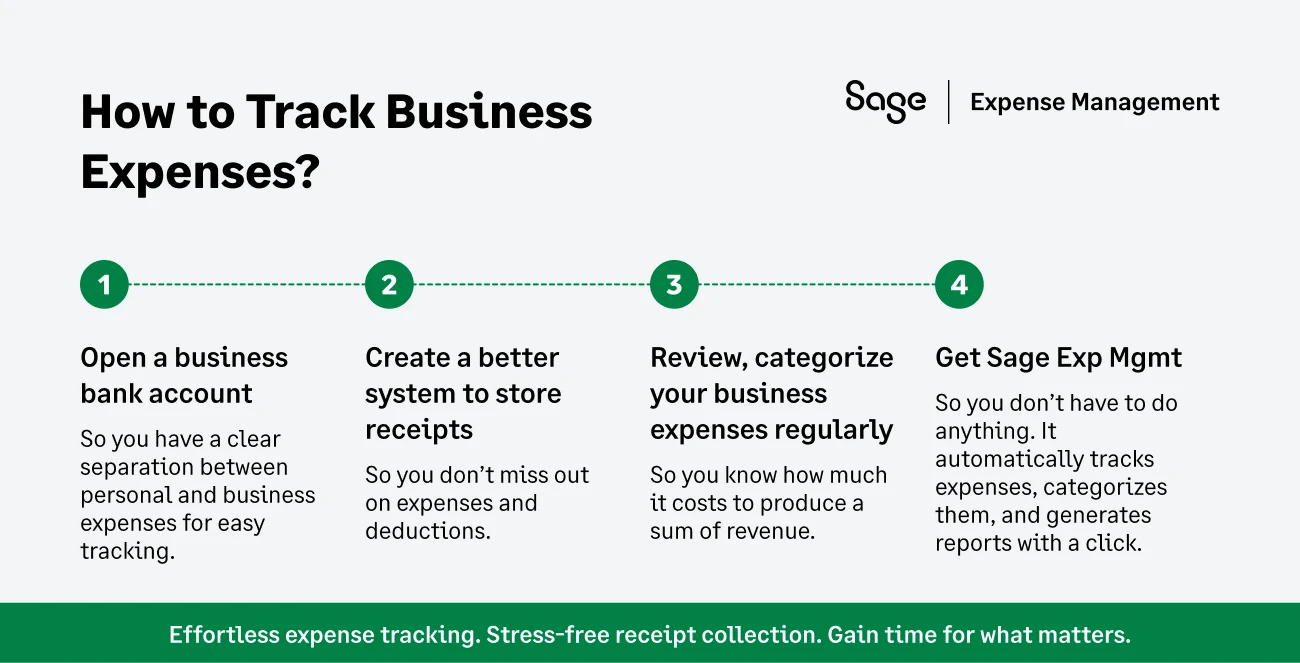

How to Track and Manage LLC Expenses?

Effective expense tracking comes down to six habits: separating business and personal finances, capturing receipts as they happen, setting clear policies, categorizing consistently, documenting travel thoroughly, and reviewing regularly.

Managing expenses accurately is crucial for tax compliance and maximizing deductions. Here are some strategies:

Open A Business Bank Account

Open a dedicated business bank account to keep business and personal finances separate. This separation simplifies record-keeping and provides a clear audit trail.

A business account also helps build your LLC's credit profile, making it easier to secure loans or other financial products in the future.

Track Your Expense Receipts

Use digital or physical copies showing expense details: date, amount, vendor, and business purpose.

Physical vs Digital Receipts

Physical receipts should be stored carefully, though digital copies simplify tax preparation and reduce paper clutter.

The IRS considers a receipt "adequate" if it includes the vendor's name, the date of purchase, an item description, and the amount paid, as per Publication 583.

Establish A Clear Expense Policy

For LLCs with multiple members or employees, having a defined expense policy prevents misclassifications.

Outline what qualifies as a deductible business expense, set spending limits, and include guidelines on required documentation for reimbursements. If you reimburse employees, make sure your plan qualifies as an "accountable plan" under IRS rules. It must establish a business connection, require adequate accounting within a reasonable time, and require return of any excess advances.

Otherwise, reimbursements become taxable wages on the W-2.

Leverage Multiple Expense Categories

Specific categories for expenses (utilities, marketing, travel, meals) are essential for accurate record-keeping. Use categories that align with IRS guidelines.

This streamlines tax filing and provides insight into where your LLC spends most of its resources, helping you make more informed decisions.

Maintain Records Of Business Travel Spending

Business travel expenses can add up quickly, so it's important to maintain thorough records.

Document transportation, accommodation, meals, and any other travel-related expenses. Note the purpose of each trip and keep receipts for all qualifying expenses. If you use a personal vehicle for business, maintain a mileage log that records dates, destinations, business purpose, and miles driven.

Regular Expense Reviews

Conduct regular reviews of your expenses, ideally on a quarterly basis.

Reviewing your LLC's expenses helps catch any missed deductions, addresses wasteful spending, and enables more accurate year-end planning. These periodic checks also help identify spending patterns so you can make adjustments before the year closes.

How Sage Expense Management (formerly Fyle) Can Help LLC Expense Management

Sage Expense Management automates the receipt-to-reconciliation workflow for LLCs, capturing card transactions in real time, matching receipts via text message, and syncing categorized expenses directly into Sage Intacct, Sage 50, QuickBooks, or Xero. The result is audit-ready records without manual entry at month-end.

- Real-time purchase alerts on credit cards: Sage Expense Management connects directly with your business credit cards, not through third-party data aggregators so card transactions appear instantly with merchant detail intact.

- Text-based receipt submission: employees text a photo of the receipt, and the system matches it to the corresponding card transaction. There's no app to install, which removes the biggest adoption hurdle for small teams.

- Submission via everyday tools: receipts can also be forwarded from Gmail, Outlook, Slack, or Teams. Expenses are auto-categorized based on merchant and historical coding.

- Real-time spend visibility: the dashboard shows expenses by category, employee, project, or department making it useful for LLCs tracking spend against jobs, classes, or entities.

- Native Sage Intacct integration: as the Sage-native expense management product, Sage Expense Management syncs cleanly with Sage Intacct for multi-entity setups, and integrates with Sage 50, QuickBooks Online, Xero, and other major accounting tools.

- Responsive support: dedicated customer success, with average support first response times in less than 30 minutes.Meaningful for finance leaders evaluating against ticket-queue alternatives.

In Conclusion

Managing LLC expenses effectively can be a game-changer for your business. It keeps you compliant and helps maximize tax savings.

By carefully tracking deductible expenses, categorizing them accurately, and staying organized, you can confidently approach tax season and make the most of your eligible deductions. Streamlining these tasks becomes even more accessible with tools like Sage Expense Management, which offers real-time tracking, seamless receipt management, and automated integrations with your accounting software.

Ready to take the hassle out of LLC expense management? Sign up for a Sage Expense Management demo today and see how effortless expense tracking can be for your business.

{{receipt-chasing="/cta-banners"}}

FAQs Around LLC Business Expenses

What Expenses are Tax-Deductible For an LLC?

Any expense that is ordinary and necessary to conduct business can be deducted. "Ordinary" means common and accepted in your industry; "necessary" means helpful and appropriate, it does not have to be indispensable.

What Expenses are Not Tax-Deductible?

Personal expenses, entertainment expenses, fines or penalties paid to a government for violating a law, illegal payments, lobbying costs, political contributions, and dues to country clubs cannot be written off.

What about Home Office Expenses?

Home-based LLCs can deduct a portion of their rent or mortgage interest if there is a dedicated workspace used exclusively and regularly for business.

You can use the simplified method ($5 per square foot, up to 300 square feet, capped at a $1,500 deduction) or the regular method (calculating the actual percentage of your home used for business and applying it to total home expenses). Full guidance is in IRS Publication 587.

How Long Do I Need to Keep Records for my LLC?

The general rule is to keep records for 3 years from the date you filed the original return. However, you must keep records for 7 years if you claim a bad debt deduction or a loss from worthless securities.

Records related to property should be kept indefinitely or at least until the period of limitations expires for the year in which you sell or dispose of the property.

Can an LLC Take the Standard Deduction and Still Deduct Business Expenses?

Yes. Business expenses are deducted from your gross income to determine your adjusted gross income, while the standard deduction (or itemized deductions) is taken from your adjusted gross income. You can take the standard deduction and still deduct your business expenses.

How Do I Deduct Car Expenses For My LLC?

You can deduct car expenses using either the standard mileage rate (70 cents per mile for 2025) or actual car expenses such as gas, oil, repairs, and insurance.

You must maintain a log of business mileage, dates, and business purpose to support your deduction.

How are Startup Costs for an LLC handled?

The IRS allows you to deduct up to $5,000 in startup costs and an additional $5,000 in organizational costs in the year your business begins.

Any remaining costs must be amortized over 180 months (15 years). The $5,000 deduction phases out dollar-for-dollar once total costs exceed $50,000.

What is the Difference Between a Deductible Expense and a Capital Expense?

A deductible expense is a cost that is both ordinary and necessary for business operations and can be deducted in the current year.

A capital expense, on the other hand, is an investment in a business asset that must be capitalized and recovered over time through methods like depreciation or amortization.

Do LLC members pay self-employment tax on all income?

It depends on the LLC's tax classification and the member's role.

For default LLCs (sole proprietorship or partnership), single members and active partners generally pay self-employment tax (15.3% in 2025, with the 12.4% Social Security portion applying only to the first $176,100) on their share of net earnings.

Passive members in a partnership-taxed LLC may not owe SE tax on their distributive share. If the LLC has elected S-corp status, members who work in the business pay payroll taxes only on their reasonable salary, not on additional profit distributions, which is the main reason owners make the S-corp election.

What is the QBI deduction and does my LLC qualify?

The Qualified Business Income (QBI) deduction, established under Section 199A of the Tax Cuts and Jobs Act, lets eligible owners of pass-through businesses deduct up to 20% of qualified business income on their personal return.

Most default-classification LLCs (sole proprietorships, partnerships) and S-corp-elected LLCs qualify, subject to income thresholds and limitations for "specified service trades or businesses" (law, health, accounting, consulting, etc.). For 2025, the income threshold above which limitations begin is $241,950 for single filers and $483,900 for joint filers. Full details on IRS Qualified Business Income Deduction.

Can I deduct expenses incurred before my LLC was officially formed?

Yes, these are generally treated as startup or organizational costs.

You can elect to deduct up to $5,000 of startup costs and $5,000 of organizational costs in the tax year your business begins operating. Anything above those amounts is amortized over 180 months. Pre-formation expenses (market research, business plan development, formation legal fees) typically fall into one of these two buckets.