Every business, from handmade cloth makers to game developers to restaurant chains, earns and spends money. Bookkeepers help you track all of it. But what do they really do?

It’s hard knowing all the answers to this question if you’ve been solely focused on growing your organization. You might not fully understand or even begin to fully appreciate what a bookkeeper does. This guide breaks down a bookkeeper's daily duties and will also show you why the good ones are priceless.

Let’s start from the beginning.

What Is Bookkeeping?

Bookkeeping is the process of recording and organizing financial transactions in a systematic way to help businesses track their income and expenses, understand their financial performance, and make informed business decisions.

What Is a Bookkeeper?

A bookkeeper is a financial professional who records and organizes financial transactions for businesses. Bookkeepers help businesses track their income and expenses, understand their financial performance, and make informed business decisions.

History Of Bookkeepers

The history of bookkeeping dates back to the beginning of commerce, around 2600 B.C. Early Babylonian and Mesopotamian bookkeepers kept records on clay tablets to keep accounts of transactions in remote cities.

In colonial America, a Waste Book was traditionally used in bookkeeping. It consisted of a daily diary of every transaction in the chronological order.

Today, a bookkeeper worth their salt uses software to track finances.

The Difference Between Bookkeepers and Accountants

Bookkeepers record day-to-day financial transactions, such as sales, purchases, and expenses. This helps businesses track their income and spending and understand their current financial position. Bookkeepers do not need any special training or education, but many have an associate's degree in accounting or a related field.

Accountants use the financial data recorded by bookkeepers to prepare financial statements, analyze financial performance, and provide financial advice. Accountants need a bachelor's degree in accounting and may also have a master's degree or professional certification, such as a Certified Public Accountant (CPA).

When Does a Business Need a Bookkeeper vs an Accountant?

Businesses usually need both a bookkeeper and an accountant, but the timing and level of involvement depend on the complexity of the financial situation.

- Bookkeepers are essential for keeping daily transactions organized and up-to-date. They handle routine tasks like processing invoices, reconciling bank statements, and preparing financial reports.

- Accountants come into play when more in-depth financial analysis is required. For instance, when businesses need financial statements prepared, tax returns filed, or financial advice on scaling operations, accountants step in.

Small businesses may rely solely on a bookkeeper at first, but as they grow, having both professionals on board becomes increasingly valuable.

Types Of Bookkeeping

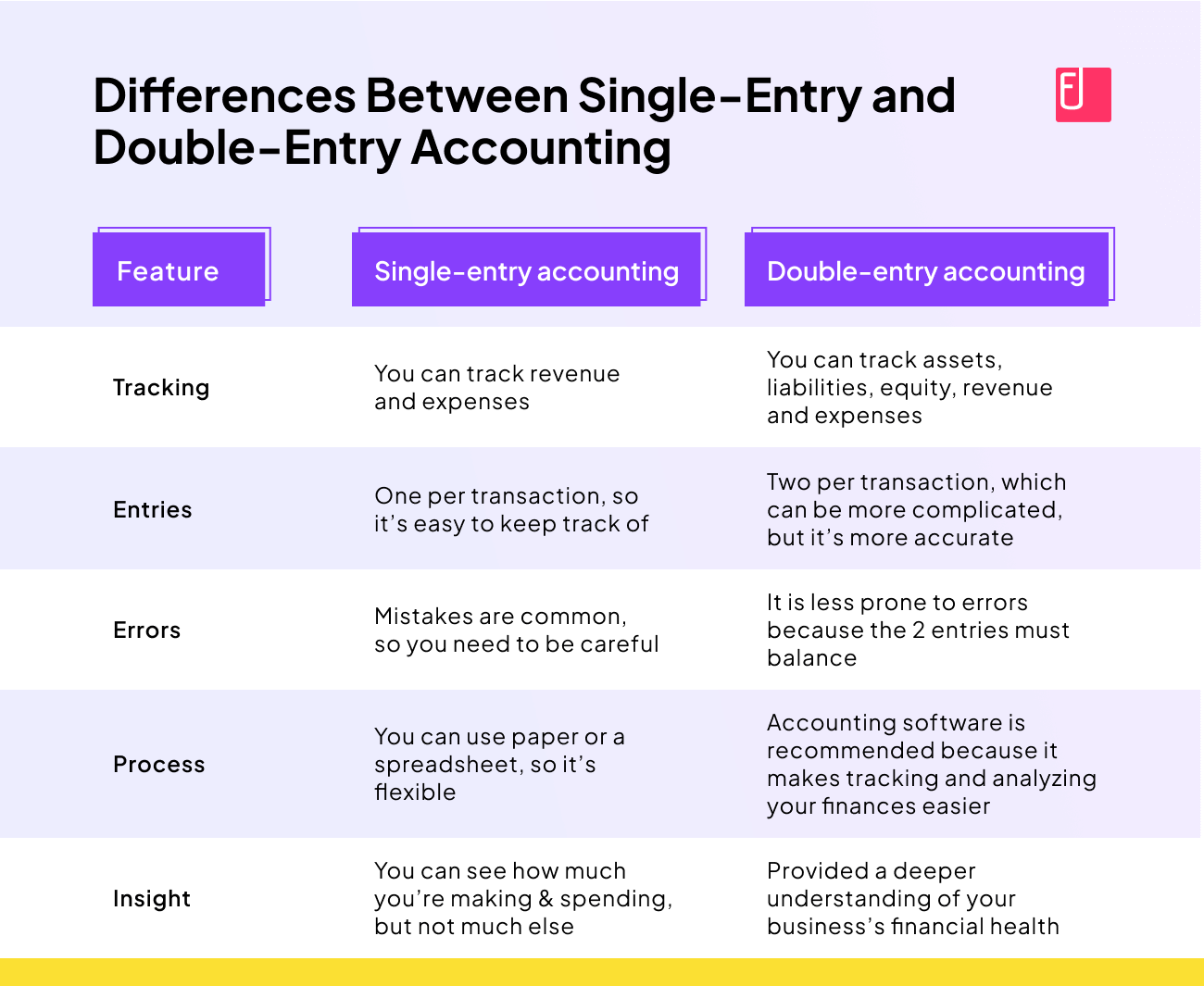

There are two main types of bookkeeping: single-entry and double-entry bookkeeping.

Single-entry bookkeeping records one side of a financial transaction, such as adding $100 to your expense account when you make a $100 purchase with your credit card.

Double-entry bookkeeping records both sides of a financial transaction, such as adding $100 to your expense account and reducing your cash account by $100 when you make a $100 purchase with your credit card.

Manual vs Automated Bookkeeping Systems

- Manual bookkeeping involves recording financial transactions by hand or using spreadsheets. While low-cost, it’s time consuming and prone to errors.

- Automated bookkeeping uses tools like Sage Expense Management. These systems automatically sync with your credit card networks to give you credit card transaction data in real-time, and automatically code all data around expenses including projects, GL codes, locations, and categories.

What does a Bookkeeper Do?

Bookkeepers are responsible for recording transactions, updating ledgers, and preparing books for accountants. They ensure that all documentation adheres to tax rules and regulations. They monitor cash flow and regularly produce financial reports that assist key decision-makers in an organization to push the business forward. Additionally, some bookkeepers also assist in optimizing payroll and invoice generation for an organization.

What Skills Are Required To Be a Successful Bookkeeper?

A successful bookkeeper needs the following skills:

- Attention to detail: Accuracy is key in financial recordkeeping.

- Basic accounting knowledge: Understanding financial principles is important.

- Familiarity with bookkeeping software: Tools like Quickbooks, Netsuite, Sage or Xero are essential.

- Time management: Bookkeepers oten juggle multiple tasks at once.

- Organizational skills: They must ensure that all financial documents are stored properly.

Bookkeeping Job Description

A bookkeeper’s job is not just about crunching numbers; it requires patience and meticulous analysis to ensure an organization has accurate financial records. Anyone who has managed a business's finances by themselves knows the value of a great bookkeeper.

Here’s a breakdown of everything a small business bookkeeper does:

1. Managing Day-to-Day Activities In Business Accounts

A bookkeeper’s job is to monitor and oversee your company's financial transactions daily by identifying and addressing financial issues promptly. They usually start with a macro perspective, such as a balance sheet or a profit and loss statement, and then drill into the details.

2. Ensuring Records Are Up To Date

Bookkeepers ensure that vendor and customer records are always up to date, even as people and businesses change. They may also need to coordinate with other departments to ensure that everyone is using the same data.

3. Keeping You Tax Ready

Tax preparation is a continuous process that requires accurate records, proper accounting systems, and timely reports. Small business bookkeepers can help make tax season smoother by maintaining accurate records, implementing proper accounting systems, and generating reports, especially for payroll. It is important to run your reports consistently and keep them in an organized folder.

4. Monitoring And Managing Bank Feeds

Bookkeepers regularly monitor your bank feeds and balances. Daily check-ins help identify discrepancies or potential issues early on. It also ensures your monthly bank reconciliations happen faster.

5. Streamlining Accounts Payable (AP)

Bookkeepers quickly process incoming AP transactions on time and make sure they are well-documented and easy to audit. Entering bills into the accounting system allows for accurate planning and decision-making.

6. Managing Invoices and Accounts Receivable (AR)

Bookkeepers quickly create and send invoices that are easy to track and replicate. This helps businesses receive payments faster and improve cash flow. To do this, small business bookkeepers perform weekly check-ins on AR aging and make adjustments as needed, such as writing off debt.

7. Preparing Financial Statements Regularly

It’s a bookkeeper’s job to prepare important financial statements for small businesses, such as profit and loss statements, cash flow statements, and balance sheets. These reports provide insights into a business's profitability, operating expenses, financial position, and cash flow.

8. Payroll

Bookkeepers can help businesses set up a systematic payroll process by creating a journal entries spreadsheet that can be reused for each payroll cycle.

9. Dealing With Foreign Currency Transactions

For businesses that deal with foreign currency transactions, small business bookkeepers can help ensure consistency by using the same spot rate from a reliable source for all transactions. This helps avoid discrepancies.

10. Regularly Conducting Stocktake

Bookkeepers regularly conduct physical inventory counts to avoid overstating the value of assets. This is an important aspect that auditors carefully examine.

Pro-tip: Involve internal auditors and compare their counts with the recorded values.

Also Read:

How Much Do Bookkeepers Make?

Bookkeepers can work as freelancers or in-house employees, and their compensation varies depending on the nature of their employment.

Freelancer Bookkeeper Salary

As of August 2024, freelancers bookkeepers in the United States earn an average of $24.31 per hour. However pay rartes can range from as low as $12.98 to as high as $35.38 per hour.

That being said, most freelance bookkeepers earn betteern $19.71 and $26.64 per hour. This variation is influenced by factors like location, experience, and skill level. Freelancers often charge by the hour but may offer flat-rate packages for specific tasks.

In-House Bookkeeper Salary

According to the US Bureau of Labor Statistics, the average bookkeeper salary in the United States is $45,860 per year or $22.05 per hour.

Remember that salaries can vary depending on experience, education, location, and industry. Bookkeepers with more experience and education or who work in high-paying industries can earn significantly more.

How To Become a Bookkeeper?

Here are a few pathways to become a bookkeeper:

- Education: A formal degree isn’t always required, but having an associate’s degree or certification in accounting can be beneficial.

- Certification: Becoming a Certified Bookkeeper (CB) through the American Institute of Professional Bookkeepers (AIPB) or a similar certification can boost credibility.

- Experience: Many bookkeepers start as administrative assistants or in entry-level accounting roles to gain on-hands experience.

- Skills: Familiary with accounting automation software, attention to detail, and organizational skills are essential for success.

Is Certification Necessary To Be a Bookkeeper?

No. Certification isn’t necessary to become a bookkeeper. However it’s highly recommended for those who want to stand out in a competitive field or charge higher rates. Certification programs provide formal education and offer practical knowledge on managing financial systems, payroll, and tax compliance.

Why is Bookkeeping Important for Businesses?

Bookkeeping plays a very important role in how an organization operates. Every business deals with money, and keeping accurate records of all transactions is crucial to its smooth functioning.

Regardless of whether you outsource the work to a professional or do it by yourself, there are a variety of benefits to great bookkeeping.

1. Instant Access To All Transactions

By updating all your financial records regularly, you will have instant access to any financial information you’d need. To make it easier, you can group your transactions into the most common categories, like:

- Goods

- Services

- Taxes

- Wages

When it’s time for a financial audit, small business bookkeepers can produce an accurate report of how your organization managed its delegated capital.

2. Making Data-backed Financial Decisions

By regularly creating and updating financial reports, you will have accurate indicators to measure success. With this data, businesses of all sizes can develop strategic plans with realistic objectives.

Some financial statements that can help in the decision-making process are:

- Balance sheet

- Cash flow statement

- Income statement

These statements don’t just help you set realistic goals but also help you identify problems in your organization. Having accurate financial records also helps you discover discrepancies between financial statements and what’s actually been recorded.

3. Better Prepared for Tax Season

To prepare for tax season, you will need to comply with the IRS’s rules and regulations, which govern their finances. Some of the most common documentation that organizations must submit to the federal government includes

- Transaction information

- Financial statements

- Tax compliance reports

- Cash flow reports

If your bookkeeping is up to date all year, you can avoid a ton of stress during tax season.

Also Read:

5 Bookkeeping Tips for Businesses

Patience and attention to detail are key to better bookkeeping. While there is no one-size-fits-all checklist, there are some standards you can adhere to which will ensure that you constantly stay on top of your finances.

1. Have a Phased Approach

If you’re in the process of moving from manual bookkeeping to a digital system, take a step-by-step approach. Rapidly shifting all at once can be overwhelming to your employees and can also discourage them.

Taking baby steps ensures you are also in control of your organization as they adjust to a new system.

2. Ensure Your General Ledger Is Up-to-date

A general ledger has all the information needed regarding a company’s financial transactions. It includes the balance sheet (equity, assets, and liabilities), and income statement accounts. General ledger accounts normally include:

- Assets like cash, accounts receivable, land, investments, and inventory.

- Liabilities like accounts payable and customer deposits.

- Stockholder accounts like treasury stock, common stock, and retained earnings.

3. Plan Taxes For The Year

Maintaining your business’s financial records and expenses throughout the year can ensure you are well-prepared when it’s time to file taxes. Without the usual hiccups or last-minute runs, you will be able to enter tax season confidently.

4. Be Aware of Seasonal Trends

Seasonality is a part of any job in the world. For bookkeepers, seasonality means periods when payments come flying in through the roof, where having outstanding work can become a serious blocker.

It becomes critical to anticipate these moments beforehand and to complete any backlog before the pressure period hits.

5. Keep Your Business And Personal Expenses Separate

It might be tempting to blur the lines between personal and business expenses when you go deep into your bookkeeping process, but it’s never the best idea. Avoiding this will reduce the risk of triggering an IRS audit as it provides an accurate representation of your finances.

Some common to keep your personal and business finances separate are

- Using a business credit card for all your business expenses

- Having separate checking accounts

- Keeping receipts for personal and business expenses separate

How Sage Expense Management (Formerly Fyle) Can Help You Automate Your Bookkeeping

Imagine a world where your bookkeeping is done for you. No more waiting for credit card statements, scanning receipts, matching transactions, or generating reports. It can automate all of these tasks, so you can focus on growing your business. Here’s how:

Conversational AI and Real-Time Credit Card Feeds

Bookkeepers can finally say goodbye to the age of frustration of missing receipts and delayed bank statements.

- With its Conversational AI, employees can also send receipts for reimbursable and credit card expenses to Sage Expense Management via text, and we will automatically create, code, and submit the expense.

- Real-time credit card feeds connect to credit card networks like Visa and Mastercard to give you notifications via text message on all card spend as soon as a credit card is swiped.

- Employees can reply to this message with a picture of the receipt, and it will automatically match it for you!

Integrate with any Accounting Software

- Sage Expense Management offers highly customizable two-way integrations with QuickBooks Online, QuickBooks Desktop, Sage Intacct, Sage 300 (beta) Xero, and NetSuite.

- These integrations are self-serve and require no coding. On average, setting up our QuickBooks integration takes just 12.6 minutes!

- It can automatically import data such as employees, projects, categories, GL codes, departments, job codes, cost codes, taxes, and more, while exporting expenses as bills, journal entries, or credit card charges in real-time. This streamlines the process and reduces manual work for accountants.

See how Sage Expense Management can elevate your bookkeeping. Schedule a demo today.

FAQs around Bookkeeping

What Is A Full Charge Bookkeeper?

A full-charge bookkeeper handles all of a business’s accounting needs, from processing payroll to managing accounts payable and preparing financial statements. Unlike regular bookkeepers, full-charge bookkeepers have broader responsibilities and often report directly to the company’s management.

How To Find a Good Bookkeeper for Your Business?

Finding the right bookkeeper can make a huge difference for your business. Consider the following tips:

- Look for Experience – A bookkeeper who has worked with businesses in your industry will better understand your specific needs.

- Ask for Certifications – Certifications like those from AIPB or NACPB can be a sign of credibility and competence.

- Check Reviews – Ask for references or check online reviews to ensure you’re hiring someone reliable.

Sage Expense Management’s Accountant Directory is a great place to start. You can search for certified professionals who can help automate your financial management and offer expertise tailored to your business needs.