.webp)

As the fiscal year comes to an end, your company must complete a handful of accounting tasks. This step guarantees accurate financial reporting for a smooth transition into the following year.

Having a year-end checklist in place should be a part of your financial accounting process. A detailed list simplifies the closing process for informed decisions, legal compliance, and solid financial health.

This page shares with you our year-end accounting checklist for robust financial management. Read on to learn how to close the fiscal year efficiently and effectively.

What Is the Year-end Close Process?

The year-end closing process is a thorough review and reconciliation of all your financial accounts and transactions at the end of a fiscal year. It involves checking and adjusting entries for:

- Income and expenses

- Assets and liabilities

- Equity changes

- Accruals and depreciation

- Bad debt provisions

- Tax adjustments to ensure financial statements are correct.

The primary purpose is to formally close out your books for the current year. However, your goals include establishing robust financial management, setting a proper budget, and ensuring business profitability for the coming year.

If there is such a thing as a month-end close process, year-end accounting also exists. It’s best to conduct the former to make the latter easier, faster, and more convenient for you. That’s where accounting tools and technologies come into play.

Companies and organizations invest in accounting software to record and analyze their financial transactions easier, faster, and better. Its global market could grow from $11,071.6 million in 2018 to $20,408 million by 2026 at an 8.02% compound annual growth rate (CAGR).

Common Challenges In The Closing Process

It’s inevitable for most companies and organizations to face financial challenges. This idea is especially true for your year-end closing process. Your bookkeeping and accounting tasks can be particularly challenging due to the following:

- Manual approach: Manually recording, tracking, and analyzing each financial transaction can be tedious and cumbersome, causing complications, delays, and errors in the entire closing process.

- Disorganized workflow: Without a well-defined, streamlined accounting process, your accounting team can encounter potential misunderstandings, work delays, and glaring errors.

- Human mistakes: Your finance professionals can commit accounting errors due to stress, exhaustion, oversights, neglect, and even skill gaps, compromising the closing process.

- Missing paperwork: The lack of financial documents, such as receipts and invoices, can cause inadequate accounting records, making it hard for you to close the books accordingly.

- Difficult communication: Unclear protocols and poor technologies used for accounting interactions among professionals result in unproductive delays during the closing process.

Companies should invest in accounting tools and technologies to avoid the challenges above and better manage financial transactions. About half of organizations have better financial management after transitioning to cloud-based accounting.

Can we replicate this in our theme?

Potential Benefits Of A Year-End Accounting Checklist

Given the five challenges mentioned above, setting a year-end accounting checklist is better for your closing process. With the help of accounting tools and technologies, you can streamline the entire process to achieve your desired results.

Below are the key benefits of a comprehensive, detailed checklist that can empower your accounting team:

- Guaranteed data accuracy and reliability: A checklist guides your accounting professionals to ensure properly reconciled accounts with supporting documents. This approach leads to accurate, complete, and up-to-date financial records.

- Enhanced efficiency and productivity: With a standardized checklist, your bookkeepers and accountants can work efficiently and effectively throughout the closing process. Accounting tools and software applications also make them more efficient and productive.

- Decreased costs and increased profits: Catching errors early and closing efficiently can help you save money from penalties, interests, and overpayments. Meanwhile, this checklist can aid your accountants in financial analysis, forecasting, and budgeting for increased profits the following year.

- Better financial reporting and decision-making: Accurate year-end books allow your accountants to generate accurate financial statements and reliable financial records. They can help you make wise and strategic financial decisions for the following year.

- Legal and regulatory compliance: Over half of organizations recognize keeping up with legal and regulatory changes as their biggest challenge. However, a thorough checklist covers all your requirements to avoid legal implications and financial losses.

A Checklist for Year-end Accounting for Effective Closing

Companies and organizations should use a comprehensive checklist to ensure a seamless year-end closing process. Adherence to this checklist guarantees properly reconciled accounts, accurate financial entries, and correct financial statements.

Here’s what to include on your checklist, plus crucial steps to take for effective closing:

1. Year-End Closing Schedule

A year-end timetable is a comprehensive timeline outlining all the accounting procedures and corresponding dates vital for the closing process. It helps you prepare for a financial audit and keeps you guided and accountable throughout the process. Nearly 75% of organizations set aside time each year to plan for the future.

To establish your closing schedule, here are the steps to follow:

- List year-end tasks.

- Set realistic deadlines.

- Assign tasks to the team.

- Use Excel or project software.

- Regularly update the schedule.

2. Financial Document Preparation

This critical step entails compiling all the financial documents required for the year-end close. It involves gathering records of all your company's financial transactions:

- Bank statements

- Statements from credit cards

- Inventory counts

- A copy of last year's tax return

- Account statements for loans

- Merchant statements

- Payroll reports

Grant Aldrich, Founder Preppy, emphasizes the complexity involved in financial document preparation.

Aldrich explains, “Collecting, organizing, and securing all the paperwork required for bookkeeping and accounting are no easy feat, like how we handle certifications. It’s best to leverage automation and CRM platforms to keep the process streamlined and everything completely organized.”

Understand that compiled financial reports promote financial transparency. They allow you to see your company's financial situation and performance for the fiscal year. To get started, follow the steps below:

- Collect financial records (bank statements, receipts, etc.).

- Prepare income statements (revenues, expenses, profits, losses).

- Create balance sheets (assets, liabilities, equity).

- Make cash flow statements (cash movements).

- For corporations, craft equity changes statements.

3. Bank Account Reconciliation

A bank account reconciliation matches your company's financial transactions from your accounting records with your bank statements. This critical step helps promote the balances' accuracy by identifying financial irregularities and correcting inconsistencies.

Albert Kim, VP of Talent at Checkr, recommends bank account reconciliation for your closing process.

Kim argues, "You cannot completely rely on your books as bookkeepers and accountants are humans subject to committing errors. You must refer to all your bank records and financial statements to make a comparison and ensure everything matches. This is what we do at Checkr by harnessing the power of AI for background checking."

That said, Kim suggests taking the following steps.

- Gather bank statements, checks, and deposits.

- Match bank transactions with ledger entries.

- Resolve any discrepancies.

- Adjust accounting records accordingly.

- Prepare bank reconciliation statements.

- Note the reconciliation process for future use.

Also Read

4. Accounts Payable And Receivable Review

For those who may or may not know, accounts payable are the money your company owes to third-party service providers like suppliers and partner vendors. Meanwhile, accounts receivable are the amounts customers owe to your company.

Pierce Hogan, Owner VariedLands, cites striking a balance between income and expenses for robust financial health.

Hogan mentions, “ Recording and reviewing your accounts payable and receivable are crucial for maintaining a consistent cashflow. There’s a need to account for every financial transaction, even as simple as travel expenses used for your business trip. In the end, the goal is to spend less than you earn for your company.”

Automating accounts payable and receivable tasks is best. Here's what you ought to do for your closing process:

Account Receivable Review

- Check customer invoices and aging reports.

- Confirm customer balances are correct.

- Address overdue or uncollectible accounts.

- Record bad debts if necessary.

- Reconcile accounts receivable records.

- Document any changes or write-offs.

Account Payable Review

- Check vendor invoices and aging reports.

- Confirm vendor balances are accurate.

- Address accrued expenses or liabilities.

- Reconcile vendor statements and records.

- Match accounts payable records.

- Document any adjustments or accruals.

5. Assets And Liabilities Check

There's a line drawn between assets and liabilities, financial aspects to examine for your closing process. While assets are your company's resources with potential economic value, liabilities are your organization's debts or financial obligations.

Suppose your company offers a freight factoring service for trucking companies. In this case, the money you hand up to your clients in exchange for invoices is your liability. However, the amounts you'll collect from your clients' customers become your assets.

For your assets and liabilities review, follow the steps below:

- Gather info on tangible (property, equipment) and intangible assets (patents).

- Physically check fixed assets.

- Update depreciation schedules.

- Review asset values for impairments.

- Confirm liability accuracy.

6. Inventory Count And Valuation

An inventory count and valuation involves identifying the exact number and worth of sellable stocks. These steps guarantee the accurate reporting of your ending inventory for the fiscal year.

Jesse Hanson, Content Manager at Online Solitaire, cites the value of inventory count and valuation as part of the closing process.

Hanson explains, "Your inventory report reflects the current assets on your balance sheet and the cost of goods sold in the income statement. It allows you to see how you’ve regulated your stock levels throughout the year, helping you make informed decisions for the following year."

Hanson recommends following the steps below:

- Conduct physical inventory count.

- Compare with book inventory.

- Identify errors or discrepancies.

- Adjust book records accordingly.

- Review valuation methods (FIFO, LIFO).

- Document reconciliation process.

7. Payroll And Employee Benefits

Simply put, payroll is the process of paying employees for their labor. However, payroll accounting includes wage computations, salary disbursements, and even employee benefit management. Think of perks such as health insurance, retirement schemes, and paid time off (PTO).

Michael Donovan, Co-Founder of Niche Twins, highlights the value of employee payroll and benefits for job satisfaction.

Donovan believes, “These are financial areas you must stay on top of as part of your year-end accounting. They let you see if you’re paying your workers correctly and reasonably. As employees are your most valuable assets, take care of them so that they will take good care of your company.”

To stay on top of your year-end closing process, conduct the following:

Payroll Review

- Check employee payroll records for accuracy.

- Reconcile payroll data with tax filings.

- Verify personnel classifications.

- Confirm tax withholdings and deductions.

- Reconcile payroll bank statements.

- Document any payroll revisions.

Employee Benefits Review

- Examine benefit schemes for accuracy.

- Verify benefit deductions and contributions.

- Reconcile benefit plan records with payroll.

- Update records for enrollments or terminations.

- Document any benefit changes.

Also Read:

8. Tax Preparation And Compliance

Tax planning involves collecting and preparing all relevant documentation required for tax reporting. This step will help you prepare for the upcoming tax season by filing taxes correctly and promptly. However, it requires keen attention to details.

For instance, some social security benefits are not taxable. As such, you should not deduct money from either approved or denied social security disability (SSD) applications. What better way to ensure tax compliance than to hire tax specialists who are well-versed with the rulings and requirements?

The ultimate goal is promoting tax compliance to avoid legal and financial ramifications. Below are the steps to take as part of your year-end closing process:

- Collect tax documents (W-2s, 1099s).

- Review documents for accuracy.

- Prepare and file tax forms (corporate, individual).

- Ensure compliance with tax regulations.

- Reconcile tax liabilities with accounting.

- Explore tax optimization strategies.

- Make required tax payments.

Also Read

9. Performance Assessments, Improvements, And Goals

Did you know that almost half of small businesses don't employ finance professionals? About 45% don't have an accountant or bookkeeper, while a quarter still use pen and paper for bookkeeping and accounting.

Brooke Webber, Head of Marketing at Ninja Patches, recommends working with finance professionals, even as a startup or small business.

Webber says, "It's best to hire accountants leveraging accounting tools for financial performance evaluation, improvements, and goal-setting. Not only will they help track and analyze your financial records, but they can also manage your financial health and help grow your business."

As part of your year-end closing, hire accounting professionals to perform the following:

- Review KPIs and financial ratios (profitability, liquidity).

- Analyze performance against goals and budgets.

- Identify strengths, weaknesses, opportunities, and threats.

- Find areas for procedural and reporting improvement.

- Develop an action plan for efficiency enhancements.

- Set SMART goals for the following year.

- Create plans, budgets, and forecasts.

- Communicate findings and plans across the company.

How Sage Expense Management (Formerly Fyle) Can Help You Speed Up the Year-End Close

Sage Expense Management offers a suite of features designed to transform your year-end accounting process.

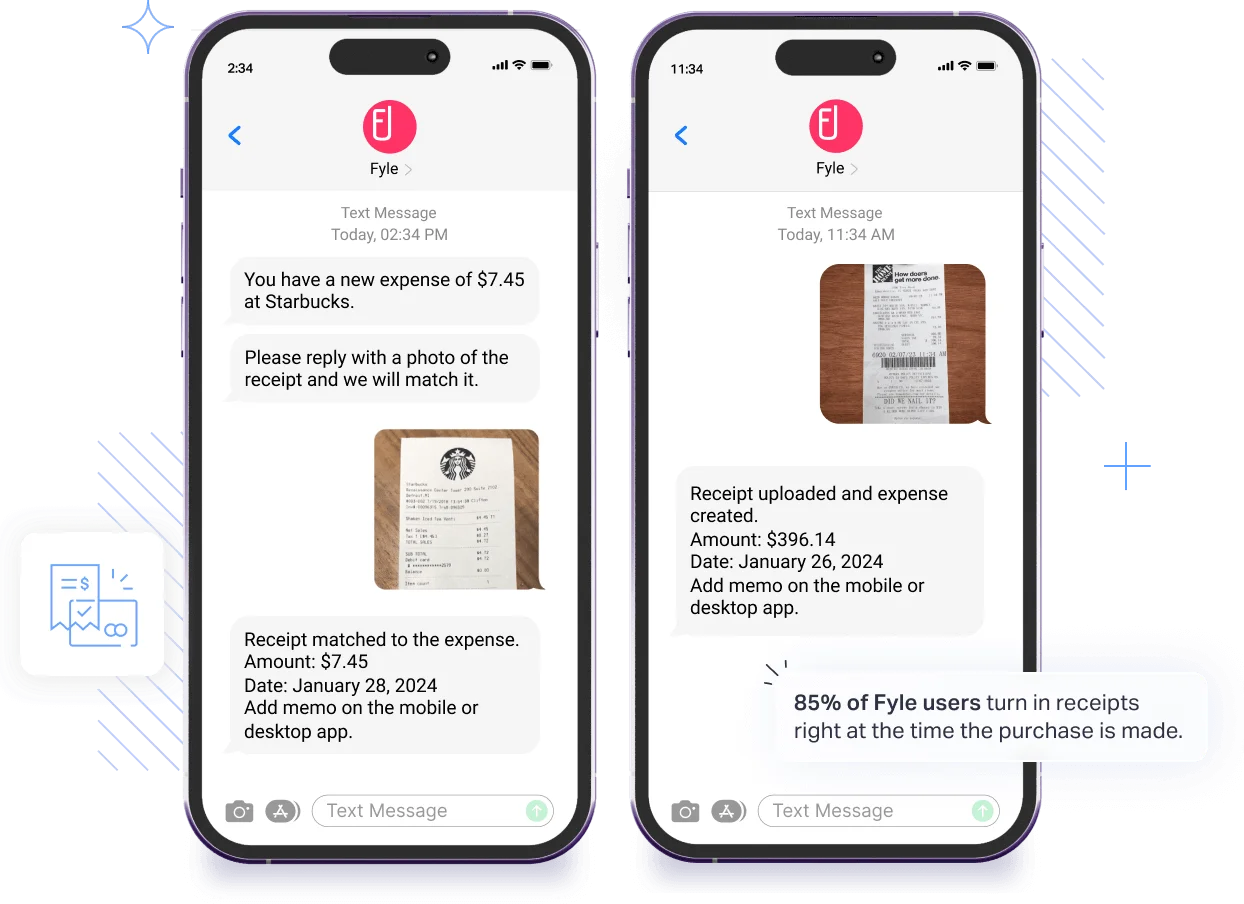

Conversational AI for Receipt Management

Employees can instantly send receipts for both reimbursable and credit card expenses to via text. The system will automatically match the receipts to the corresponding card transactions.

Real-Time Credit Card Feeds

Our platform directly integrates with credit card networks like Visa and Mastercard to give you real-time text notifications for all credit card transactions.

Users can reply to this text with a picture of the receipt for instant reconciliation!

Policy Compliance

Built-in compliance checks flag policy violations instantly, ensuring every expense adheres to company regulations.

AI-Enhanced Spend Visibility

Sage Expense Management's CoPilot provides instant, AI-driven insights into spending, helping you monitor budgets and spot discrepancies quickly.

Accounting Integrations

Our platform integrates seamlessly with QuickBooks, Sage, Xero, and other accounting software, ensuring a smooth transfer of data for tax filing and financial reporting.

Multi-Level Approvals

Approvers can review and approve expenses from anywhere, streamlining workflows and speeding up the approval process.

Exceptional Customer Support

With 24/7 customer support and a record implementation time of under two weeks, Sage Expense Management ensures businesses are up and running quickly, no matter the time of year.