.webp)

Running a small business is a journey full of challenges, and managing your finances is one of the biggest. The manual,paper-based workflows of yesterday are no longer sustainable in a world that moves at a lightning-fast pace. Inefficient processes lead to delayed month-end closes, poor financial decisions, and even missed growth opportunities.

With the right accounting practices, however, you can reduce stress, maintain compliance, and create a clear path to growth. In this guide, we’ve compiled 25 practical tips to help you streamline your small business accounting. These tips are designed for small and medium businesses looking to grow and scale their operations.

What is Small Business Accounting?

Small business accounting involves the systematic tracking of a business’s income, expenses, assets, and liabilities. It includes recording transactions, preparing financial statements, managing taxes, and maintaining accurate financial records.

A well-managed accounting system helps you understand the true financial health of your small and medium business and gives you the data you need to make informed, strategic decisions.

Why Should You Care About Small Business Accounting?

Accurate accounting is the bedrock of a sustainable business. It ensures your business is compliant with complex tax laws, provides you with valuable insights into your cash flow and profitability, and helps you proactively identify areas for improvement.

Neglecting your accounting can result in missed tax deadlines, poor financial decisions, and severe legal trouble during an audit. This is because the IRS places the burden of proof on you, the taxpayer, to substantiate every deduction and statement made on your tax returns.

Good accounting practices aren't just about avoiding penalties; they're the foundation of a thriving, growing business.

A Checklist to See If Your Small Business’s Accounting Needs Attention

Use this checklist to evaluate the state of your small business's accounting processes. If you answer “No” to any of these, it may be time to update or improve your systems.

Defined Accounting Processes

- Do you have a clear, documented process for managing your business's financial transactions?

- Have you set specific timelines for regular accounting tasks (e.g., reconciling accounts and generating financial reports)?

- Do you have a professional accountant, bookkeeper, or outsourced service to assist with complex accounting tasks?

Bill Pay System

- Do you have an efficient system for paying bills on time and keeping track of upcoming payments?

- Is your bill payment process automated (e.g., using tools like bill pay services or software for recurring bills)?

Expense Management System

- Do you have a standardized system for managing credit card expenses across the company?

- Is your team still manually collecting paper receipts and matching them to transactions?

Automated Systems & Integration

- Are your accounting systems automated to reduce manual entry and human error (e.g., invoicing, bill pay, expense tracking)?

- Do your accounting tools integrate seamlessly with other business software (e.g., your CRM, payroll system, expense management tools)?

Payroll System

- Is payroll automated and integrated with your accounting system to ensure accurate tax reporting and financial tracking?

Accounting Software & Tools

- Are you using modern accounting software that fits your business needs?

- Does your accounting software and other systems allow for easy reporting and data exporting?

Tax

- Are you working with a tax professional or accountant to ensure compliance and optimize your tax strategy?

Security

- Are your accounting systems protected with strong security measures to prevent fraud or unauthorized access?

Scalability

- Are your accounting systems and processes scalable as your business grows?

Financial Reporting

- Do you generate regular financial reports (e.g., profit and loss statement, balance sheet, cash flow statement)?

- Are your financial reports accurate, consistent, and up-to-date?

- Do you use these reports to make informed business decisions, assess profitability, and manage cash flow?

Next Steps: If you answered "No" to any of these items, it might be time to reevaluate your accounting systems and processes.

25 Small Business Accounting Tips for Business Owners

Here are 25 tips that can be used by small and medium businesses to set up, maintain, and improve their accounting process:

1. Set Up Accounting for Small Businesses

Getting your accounting system in place is the first and most critical step to achieving financial control. You’ll need to choose the right accounting method (cash or accrual), set up consistent bookkeeping practices, and decide whether to manage it yourself or hire a professional.

It’s wise to review your system as your business grows from year to year. A new controller joining your team, for instance, is a strong trigger to re-evaluate and implement a more robust system.

- Establish Foundational Practices: Define clear processes for recording transactions, handling expenses, and preparing financial statements. The IRS allows for any recordkeeping system as long as it "clearly shows your income and expenses" and includes a summary of business transactions in your books.

- Decide on Professional Help: Determine if you will handle accounting in-house or outsource it. Hiring a professional can provide expertise in tax compliance and financial strategy, saving you from costly mistakes.

How often: One-time setup, with periodic reviews as needed

2. Open A Small Business Bank Account

One of the first things every business should do is open a separate business bank account. Mixing personal and business finances can lead to confusion, errors, and potential legal issues during an audit. Having a dedicated account makes it easier to track income and expenses, ensuring your records are clean and accurate.

- Follow GAAP: This practice is a core requirement of the Economic Entity Assumption in GAAP, which treats a business as a separate entity from its owners.

- Simplify Recordkeeping: Your business checking account can serve as the main source for entries in your business books, making it easier to track and report income and expenses for tax purposes.

How often: One-time setup, ongoing use

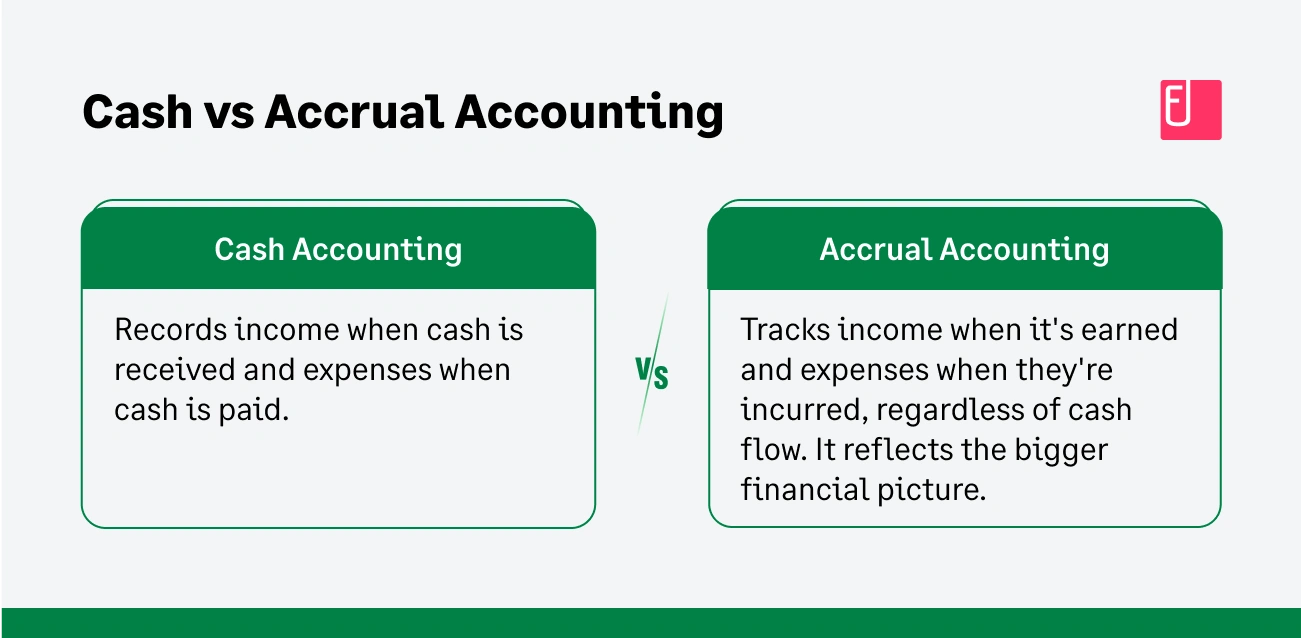

3. Choose An Accounting Method

There are two main accounting methods: cash and accrual. Your choice will determine when you can deduct expenses.

- Cash Accounting: This method records income when cash is actually received and expenses when they are paid. It’s simpler and a popular choice for very small businesses and sole proprietors who don't have inventory.

- Accrual Accounting: This method records revenue when it is earned and expenses when they are incurred, regardless of when cash is exchanged. It provides a more accurate long-term picture of your financial health and is typically required for larger businesses or those that hold inventory.

How often: One-time decision, reviewed annually

4. Set Up A Chart Of Accounts

A chart of accounts (COA) is a foundational tool for your business. It is a comprehensive, organized list of every account in your general ledger, serving as a roadmap for categorizing every financial transaction—whether it's income, an expense, an asset, or a liability. A well-organized COA is essential for quickly analyzing the financial health of your business.

Why a Detailed Chart of Accounts Matters?

A detailed COA is critical for generating the granular financial reports needed for effective decision-making. Without it, you risk having too few accounts, which blurs your financial data, or too many, which makes reporting unwieldy. A well-structured COA also helps you maintain the records required by the IRS to support your tax filings.

The Structure of a Chart of Accounts

A typical COA is organized into five main categories, with specific sub-accounts for each:

- Assets: What your business owns (e.g., cash, accounts receivable, inventory, equipment).

- Liabilities: What your business owes (e.g., accounts payable, loans, credit card debt).

- Equity: The owner’s stake in the business.

- Revenue: Money earned from sales and other income streams.

- Expenses: All costs incurred to run your business. The IRS requires expenses to be ordinary and necessary to be deductible, and your COA should be structured to easily track these.

Review and Refine Annually

As your business grows and new types of transactions emerge, you should regularly review and update your COA. Work with your accountant to ensure your COA perfectly fits your business, providing the right balance of detail for accurate reporting and tax compliance.

How often: One-time setup, with annual reviews.

Also Read:

5. Determine The Fiscal Year

Your fiscal year is the 12 months for financial reporting. It could follow the calendar or align with your business cycle. Choosing the right fiscal year can simplify your accounting and tax preparation.

How often: One-time decision

6. Know When Your Business Needs A Software Upgrade

As your business scales, manual processes can become a major bottleneck. A study by SVB found that manually processing 1,000 expense reports a year can take around 400 hours and cost about $60 per report.

If you're spending too much time on paperwork or struggling with a legacy system, it's a clear sign you need to upgrade to an automated accounting system that scales with your business.

How often: Periodically, as your business grows

7. Process and Workflow Automation

Automation is a game-changer for small business owners. It reduces manual errors, saves time, and allows you to focus on other aspects of running your business. Use software to automate invoicing, expense reporting, and bank reconciliations.

The right software can simplify each aspect of your accounting process. Some tools businesses can use include:

- Payroll: Gusto, Rippling

- Bill Pay: BILL, Routable, Settle

- Expense Management: Sage Expense Management (formerly Fyle)

- Bookkeeping: QBO

By automating repetitive tasks like data entry and reconciliation, you free up valuable time. Automated tools also ensure consistency and accuracy in your workflows. Look for tools that can seamlessly handle tasks like payroll processing, cash flow management, and credit card reconciliation.

How often: Continuous

8. Record Transactions

Recording transactions regularly is essential for accurate bookkeeping and helps you avoid costly mistakes. Ensure that every sale, expense, or refund is logged in your system promptly. Keeping records up-to-date not only makes it easier to file taxes but is also a core requirement of the GAAP Time Period Assumption, which assumes a business's life can be divided into distinct reporting periods.

How often: Daily/Weekly

9. Prepare And Send Invoices

Getting paid on time is critical for maintaining healthy cash flow. To avoid payment delays, create and send invoices promptly. Use invoicing software to automate the process and track outstanding payments. This helps you get paid faster, which is a major benefit for small businesses.

10. Track Your Small Business Expenses

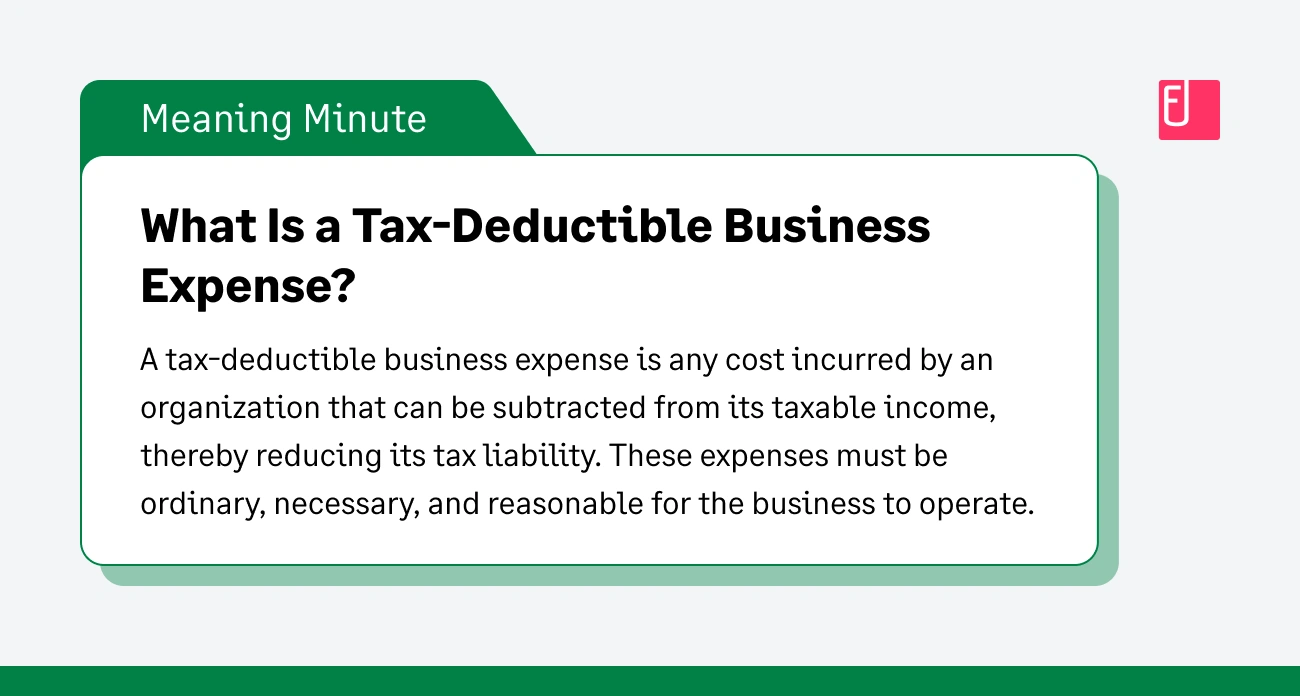

Tracking business expenses is crucial for maintaining financial health and maximizing your tax deductions. To be deductible, an expense must be both ordinary and necessary.

Small expenses can quickly pile up and, if left unchecked, lead to budgeting issues, cash flow problems, and missed tax write-offs. Consistently tracking every transaction ensures you have a clear picture of where your money is going, helping you make informed decisions and avoid overspending.

Consistently tracking every transaction ensures you have a clear picture of where your money is going, helping you make informed decisions and avoid overspending.

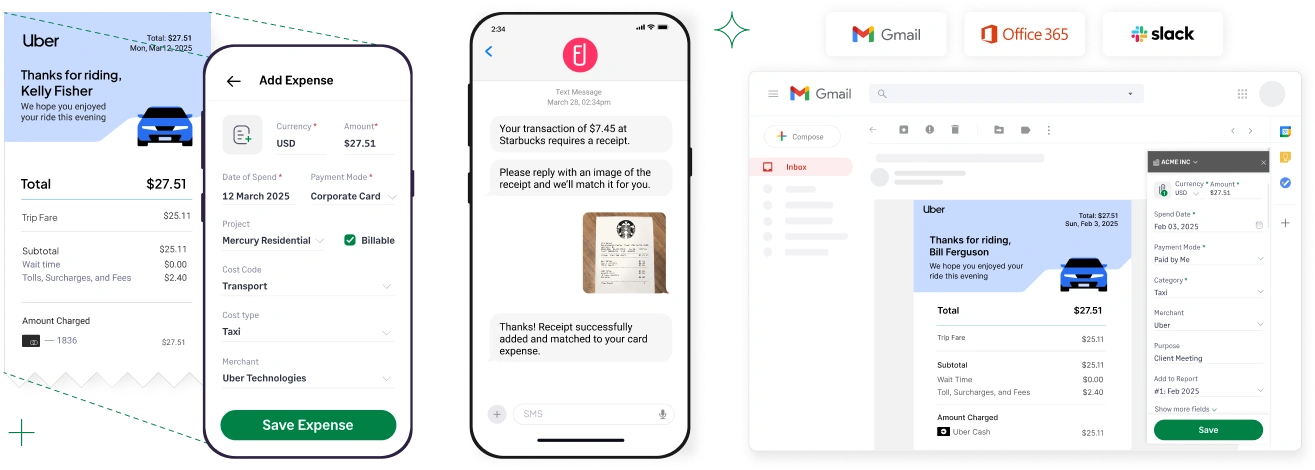

Sage Expense Management automates the entire process business expense management process. Its directly connects with business credit cards to give you real-time transaction data. When an employee swipes a card, an expense is immediately created in the system, and they are prompted to submit a receipt via text, email, or the mobile app.

This dramatically reduces the risk of lost receipts and the time spent on manual tracking, helping you stay audit-ready.

How often: Weekly

11. Document And File Receipts

Maintaining proper documentation is crucial for tax deductions and audits. The IRS requires you to keep records to support all items of income, deductions, and credits on your tax returns, typically for three years from the date you filed. A bad audit experience due to missing records can severely damage your business's reputation and financial health.

Our Conversational AI allows employees to submit and track receipts via text message, ensuring you’re always prepared for tax season. For digital receipts, you can use the Outlook or Gmail add-ons to create an expense directly from an email and forward it to a unique email address.

How often: Weekly

12. Pay Vendors

Late payments can strain vendor relationships and lead to late fees. Set up a system to track due dates and ensure that bills are paid on time. Automating this process helps you manage your cash flow effectively and maintain a positive reputation with your suppliers.

How often: Weekly/Monthly

13. Review Accounting Processes Regularly

Take the time to review your accounting processes periodically. Identify areas that could be improved or automated, and stay proactive about addressing inefficiencies. This ensures your accounting practices remain effective as your business grows.

- Continuous Improvement: An audit experience, for example, can be a "significant trigger" for adopting a more organized and compliant expense management tool to avoid future complications.

- Consistency is Key: The GAAP Consistency Principle states that once an accounting method is adopted, it should be used consistently from one period to the next to ensure comparability. Any changes should be fully disclosed and explained.

- Stay Scalable: As your business scales and the number of expenses increases, manual processes can become cumbersome. Reviewing your workflows regularly helps you identify when it's time to invest in a more automated and scalable solution.

How often: Quarterly

14. Review Cash Flow

Your cash flow statement shows how much money is coming in and going out of your business. Review it regularly to ensure you have enough cash to cover expenses. A healthy cash flow is essential to keeping your business running smoothly.

- Projecting Cash Needs: Regularly reviewing your cash flow helps you identify potential cash shortages and make strategic decisions to prevent them.

- Connect to Revenue: The GAAP Matching Principle dictates that expenses should be matched to the revenue they helped generate in the same accounting period, which provides a more accurate picture of profitability and cash flow.

- Real-Time Visibility: Tools that provide real-time visibility into spending help you manage cash flow more effectively, as you don’t have to wait for outdated reports to see where your money is going. This enables proactive budget management and faster course correction if a project or department is overspending.

How often: Monthly

15. Review Past Due Invoices

Late payments can cause serious cash flow problems. Review overdue invoices regularly and follow up promptly with customers. Consider offering early discounts or setting clear payment terms to avoid late payments. Automation tools can be particularly useful here for sending reminders to customers with overdue balances.

- Understanding the Impact: Consistent monitoring of your accounts receivable ensures you collect revenue in a timely manner, which is crucial for maintaining a healthy cash flow and making informed financial decisions.

- Handling Bad Debts: If a receivable goes unpaid for too long, it may become a "business bad debt". According to the IRS, a debt becomes a bad debt when there is no longer any chance it will be paid. If you use the accrual method of accounting, you can deduct this uncollectible amount as a bad debt if you previously included it in your income.

How often: Weekly/Monthly

16. Check + Take Stock Of Your Inventory

Inventory management is a critical part of accounting for businesses that sell products. Make sure your inventory is updated regularly to prevent over-ordering or stockouts.

- Valuation Methods: Under the GAAP Consistency Principle, once you choose an inventory valuation method (such as FIFO or weighted average), you must use it consistently from one period to the next to ensure your financial statements are comparable.

- Cost of Goods Sold (COGS): The cost of your inventory is a key factor in determining your Cost of Goods Sold. COGS is a significant deduction that impacts your gross profit and, ultimately, your taxable income, making accurate inventory records essential for tax season.

- Leverage Technology: Inventory tracking software can help automate this process, ensuring your records are always up-to-date.

How often: Monthly

17. Prepare And Review Financials

Financial reports, such as the balance sheet, profit and loss statement, and cash flow statement, provide key insights into your business’s performance. Review them regularly to track progress, identify potential issues, and plan for the future.

Follow GAAP Principles

- Full Disclosure: Your financial reports must disclose all information that could influence a user’s economic decisions, such as a large client, a major liability, or a significant change in an accounting method.

- Consistency: Consistent reporting ensures that your financial reports are comparable from one period to another.

- Objectivity: All financial records and statements must be based on objective, verifiable evidence, such as receipts and invoices.

Know Your Reports

- Balance Sheet: Provides a snapshot of your company's financial position at a specific point in time, detailing your assets, liabilities, and equity.

- Income Statement (Profit and Loss): Summarizes your revenues, costs, and expenses over a specific period, showing your profitability.

- Statement of Cash Flows: Tracks the money flowing in and out of your business, which is essential for managing day-to-day operations.

How often: Monthly/Quarterly

18. Review Long Overdue Receivables

Receivables that go unpaid for too long can create cash flow problems. Monitor overdue accounts closely and have a plan in place for collections. Automation tools can send reminders to customers with overdue balances.

- What to Track: In the context of taxes, a long overdue receivable can become a business bad debt.

- The IRS on Bad Debts: The IRS defines a business bad debt as a debt that is uncollectible and has either originated from or is closely related to your trade or business. For a business using the accrual method of accounting, this deduction is only allowed if the amount was previously included in gross income.

How often: Monthly

19. Investigate Import Tax

If your business imports goods, you should be aware of the applicable taxes and compliance requirements. Failure to adhere to import tax laws can result in fines or delays in getting products to market. Consulting with a tax professional can help you correctly account for and deduct these costs.

- Tax Compliance: Accurate recordkeeping of all import taxes and duties paid is crucial for filing your tax returns correctly.

- Deductibility: Some import taxes may be deductible as a business expense, while others must be capitalized.

How often: Annually/as needed

20. Establish Sales Tax Procedures

Sales tax can be complicated, especially if you operate in multiple locations. Set up clear procedures for collecting, reporting, and paying sales tax.

- Collection and Remittance: You are generally responsible for collecting sales tax from your customers at the time of sale and remitting it to the appropriate state or local government.

- Not a Business Expense: Sales tax that you collect is a liability for your business, not an expense. The tax itself is not a deductible business expense for your business.

- Avoid Penalties: Failure to pay the correct sales tax amount or missing deadlines can result in fines, penalties, or audits. Using tax software can automate this process and reduce the risk of errors.

How often: Monthly/Quarterly

21. Determine Your Tax Obligations

Work with a tax professional to understand all your business’s tax obligations. This includes federal, state, and local taxes, as well as any industry-specific tax liabilities you may face.

For self-employed individuals with net earnings of $400 or more, paying self-employment tax is a requirement.

- Understanding Taxable Income: A key objective of accounting is to ensure accurate reporting of income and expenses to determine your tax liability. Your gross profit (gross receipts minus cost of goods sold) is the amount you will pay tax on.

- Deductible Expenses: The IRS allows you to deduct expenses that are both ordinary (common in your industry) and necessary (helpful and appropriate for your business). Examples include rent, salaries, and insurance premiums.

- Amortizing R&D Costs: Be aware of new tax laws. For example, a new rule starting in 2022 requires research and experimental costs to be amortized over a 5-year period instead of being deducted in the current year.

How often: Annually

22. Review And Pay Quarterly Payroll Taxes

If you have employees, you must withhold and pay various employment taxes. Failure to do so can result in penalties.

- Deductibility of Payroll Taxes: When you pay employees, you can deduct their full wages as a business expense. However, the employment taxes that you pay from your own funds (the employer's portion) are deductible as a separate business expense.

- Automate to Avoid Penalties: Payroll taxes must be filed quarterly. Ensure that your payroll software is set up to calculate, deduct, and file taxes automatically to avoid penalties. The IRS considers a reimbursement plan "accountable" if employees substantiate their expenses, but reimbursements under a "nonaccountable" plan are treated as wages and are subject to employment taxes.

How often: Quarterly

23. Pay Sales Tax Obligations

Paying sales tax obligations is critical for complying with state and local tax laws. Sales tax rates and requirements vary depending on where your business operates and what products or services you sell.

- Sales Tax is a Liability, Not an Expense: Failure to pay the correct sales tax amount or missing deadlines can result in fines, penalties, or audits. To avoid this, ensure you’re collecting the correct sales tax at the time of sale and that you’re keeping accurate records of those transactions. The tax itself is not a deductible business expense for your business, but a liability you must remit to the government.

How often: Monthly/Quarterly

24. Fill Out And File IRS Forms

Filing IRS forms is a necessary part of business tax compliance. Different forms apply depending on your business structure and payroll obligations.

For example, you might need to file forms such as W-2s, 1099-NECs, or Form 941 to report employee wages, independent contractor payments, or quarterly payroll taxes. Staying organized is key, as each form has specific deadlines.

- Keep Your Records Organized: The IRS requires that all records be permanent, accurate, and complete. Your records must be sufficient to support all items of income and expense on your tax returns.

How often: Annually/Quarterly

25. File Tax Returns

Filing your business tax returns is an annual requirement. They compile your income, deductions, and other financial data for the year.

For small businesses, the type of tax return you file depends on your business structure (e.g., Form 1120 for corporations, Form 1065 for partnerships, or Schedule C for sole proprietors).

To avoid errors and missed deductions, maintain organized records throughout the year and ensure all expenses are properly categorized. Learn more about Decimal’s Tax Services and work with experts who can help you minimize your tax liability.

Using automated tools like Sage Expense Management to manage your expenses can help streamline the process and keep your financial records in perfect order for tax season.

How often: Annually

Bonus Pro-Tips

26. Apply For Small Business Funding

Having up-to-date financials is key when seeking small business loans or investments. Ensure that your bookkeeping is clean and that you have detailed reports to share with potential lenders or investors.

27. Find High-Quality Accounting Partners

Hiring the right accountant or bookkeeping service can save you time and money in the long run. They’ll help you avoid costly mistakes and ensure your books are in order. Look for someone experienced with small businesses in your industry. Check out Decimal to learn why outsourcing may be right for you.

How Sage Expense Management and Decimal Can Help

Decimal and Sage Expense Management work together to streamline accounting processes and reporting, allowing you to close your books faster each month. This boosts productivity and ensures accurate bookkeeping.

Sage Expense Management

Be Audit Ready with Accurate Record Keeping

Sage Expense Managementautomates the collection and coding of receipts, eliminating human error. When tax season arrives, your books will be in order, with every transaction accurately documented.

Stay Compliant with Robust Policies

The policy engine ensures that all expenses are verified against company policies before submission. This reduces the risk of fraud, ensures compliance, and identifies duplicates.

Decimal

Improve your accounting processes to scale with you

Decimal handles your day-to-day bookkeeping, allowing you to focus on your business. Gain reporting and insights into your business that help you make strategic decisions. As the business grows, Decimal is ready to assist with bill pay, payroll support, and so much more.

Gain expert insights in Tax Planning

Decimal’s Tax Service gives you access to former KPMG CPAs who have deep experience with businesses across the US. They’ll help you maximize your returns and walk you through the best strategies when structuring and running your business.

Small Business Accounting FAQs

What Are The Basics Of Small Business Bookkeeping?

Bookkeeping involves recording all of your business’s financial transactions, categorizing them, and tracking income and expenses. The goal is to ensure your books are accurate and up to date for tax reporting and financial analysis.

What Accounting Is Required For A Small Business?

All businesses need to maintain accurate financial records, file tax returns, and ensure compliance with local and federal regulations. Depending on the size of your business, you may also need to issue financial statements, such as balance sheets and income statements.

Can You Do Your Own Small Business Accounting?

Yes, many small business owners manage their own accounting. However, as your business grows, it may become too time-consuming, and you might want to hire an accountant or invest in accounting software to help manage the workload.

How Do I Do Accounting For My Small Business?

To do your accounting, start by setting up a system to track income and expenses. Record every transaction, reconcile your bank accounts, and prepare financial statements regularly. You can do this manually, but using accounting software makes the process much easier.

How Much Should I Pay An Accountant For My Small Business?

The amount you pay can vary widely depending on your specific needs. Consider factors like whether you need assistance with tax preparation, bookkeeping, bill payments, financial reporting, or strategic advice. The complexity of your business, its size, and the frequency of services you require will also play a role in determining the cost. As you explore options, you will find various plans or services that align with your budget and meet the needs of your business.

What Does An Accountant Do For Small Business Owners?

An accountant helps manage your financial records, ensures tax compliance, prepares financial statements, and advises on financial decisions. They can also assist with tax planning and filing, helping you save money and avoid penalties.

What Does A Bookkeeper Do For A Small Business?

A bookkeeper is responsible for recording all daily financial transactions. They manage invoices, track expenses, reconcile bank accounts, and ensure that your financial records are organized and accurate. This frees you up to focus on running your business.

.webp)