The phrase- IRS Audit is usually enough to make any business owner’s blood run cold. But the fear isn't really about getting caught doing something wrong; it’s about the paperwork.

Most audit disasters don't happen because of fraud; they happen because of disallowed deductions. You spent the money, and it was a legitimate business expense, but you couldn't prove it to the auditor's satisfaction.

The good news? The rules are actually quite clear.

Understanding the IRS requirements (specifically Revenue Procedure 97-22 and Publication 463) turns recordkeeping from a frantic month-end chore into an insurance policy for your profit margins.

What are IRS Receipt Requirements?

To the IRS, a receipt isn't just a piece of paper; it is documentary evidence.

The core concept you need to understand is the Burden of Proof. In the US tax system, you are guilty until proven innocent. The IRS does not have to prove you didn't buy that laptop; you have to prove you did. Without documentary evidence, the expense effectively didn't happen.

What Information is Required on a Receipt?

A credit card slip showing a total is often not enough. To be audit-proof, a receipt must clearly show these five specific data points:

- Name of payee: Who did you pay? (e.g., Home Depot, Delta Airlines)

- Date: When did the transaction happen?

- Amount: The total cost, including tax and tip.

- Place: The location of the expense.

- Business Purpose: The why.

The Business Purpose Trap

Most receipts (like a restaurant bill) show the first four items automatically. The fifth, business purpose, is usually missing. You must write this on the receipt yourself (e.g., "Lunch with client John Doe to discuss Q3 contract").

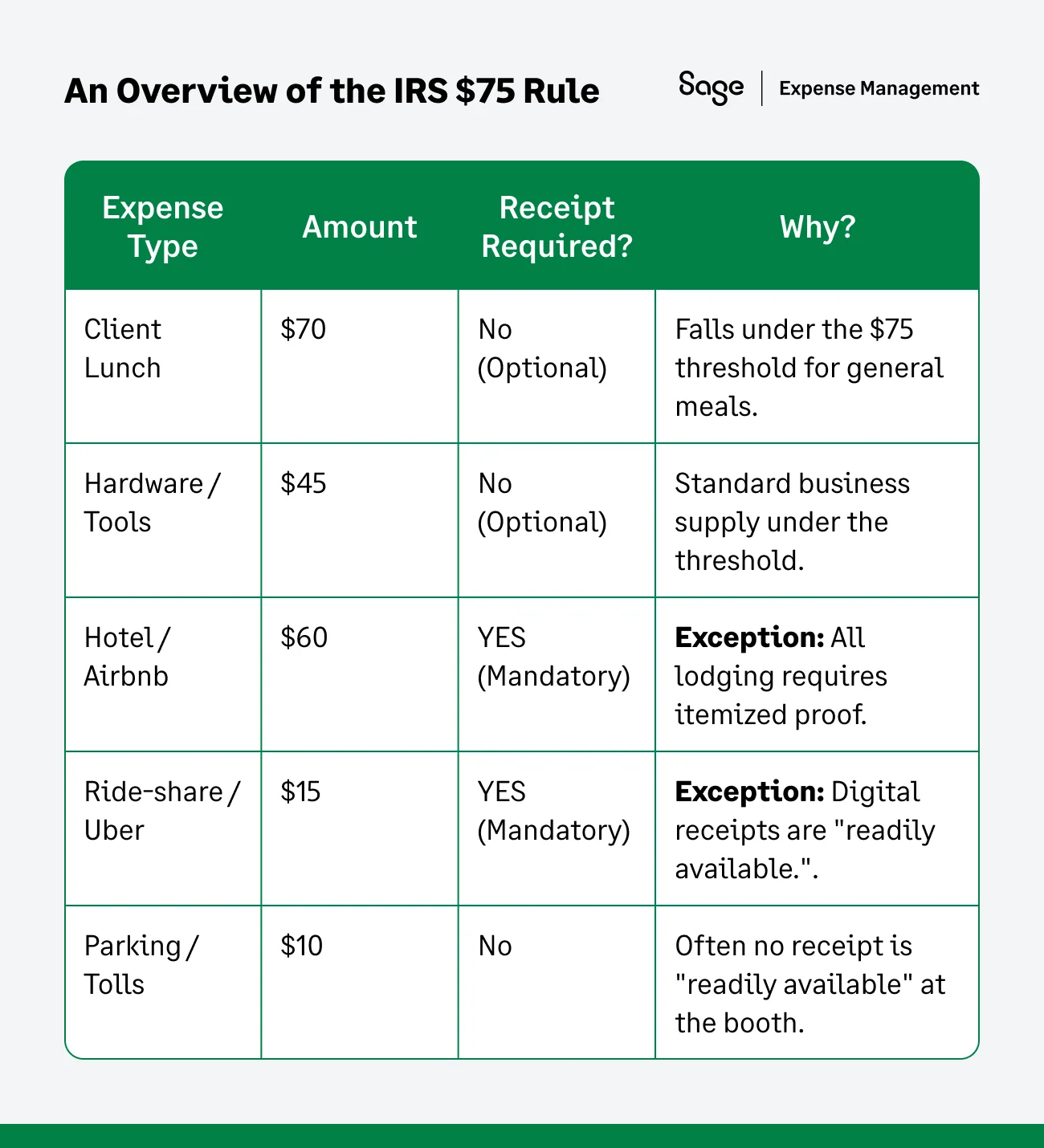

The IRS $75 Receipt Rule

This is perhaps the most famous shortcut in tax recordkeeping, but it is also the most dangerous for businesses that take it at face value.

While the IRS does offer some leniency for small, everyday expenses, the fine print contains exceptions that can lead to disallowed deductions if you aren't careful.

The General Rule: The $75 Threshold

According to IRS guidelines, you generally do not need to provide documentary evidence (like a receipt or invoice) for business expenses that are less than $75.

This rule exists to prevent both the taxpayer and the IRS from being buried in paperwork for minor costs like a quick lunch, office stationery, or a hardware store run for a few nails.

- The logic: The IRS assumes that for small amounts, the administrative burden of tracking every single slip of paper outweighs the benefit of perfect accuracy.

- The pro-tip: Even if the IRS doesn't require the physical receipt, you still need to record the Business Purpose, date, and location of the expense in your ledger to claim the deduction.

When the $75 Rule Disappears

The IRS is significantly stricter when it comes to travel and overnight stays. There are two massive exceptions where you must provide a receipt, regardless of how small the amount is:

1. Lodging (Every single cent counts)

If your business expense is for lodging—whether it’s a hotel, motel, or a short-term rental like an Airbnb—you must have a receipt.

- Why: The IRS views lodging as a high-risk area for personal vs. business mixing. They want to see the itemized breakdown to ensure you aren't billing the company for non-deductible personal services (like a spa treatment or a movie rental) disguised as a room charge.

- The scenario: You find a last-minute deal for a $65 roadside motel while traveling between job sites. Even though it is under $75, that deduction is illegal without a receipt.

2. Transportation (The readily available Standard)

For travel expenses like taxis, trains, buses, or airport shuttles, you are required to keep a receipt if one is readily available.

- What this means: In the age of Uber, Lyft, and digital train tickets, a receipt is almost always readily available via email or app history. Therefore, the $75 no receipt cushion rarely applies to modern transportation.

- The reality: If a superintendent takes a $20 taxi to a permit office and the driver can provide a printed slip, they are expected to take it.

The IRS $75 Rule at a Glance

Business Expenses That Require Receipts

While the IRS $75 rule offers some leeway, relying on it is often a rookie mistake for growing businesses. Savvy finance teams typically ignore the threshold and require receipts for every single transaction.

Here is a breakdown of why 100% receipt capture is the gold standard and the specific rules you must follow for high-scrutiny categories.

The Savvy Strategy: Fighting the Memory Gap

Finance teams mandate receipts for everything because memory is not a valid audit trail. When an auditor asks about a $60 charge from 18 months ago, a vague answer like "I think it was for printer ink" won't suffice.

- The reality of physical paper: Receipts are fragile. Thermal paper receipts (the kind commonly used at gas stations, hardware stores, and restaurants) are notorious for fading into blank strips of paper when exposed to heat or light—whether they are left in a car or even just sitting in a wallet.

- The fix: By requiring an immediate digital scan or photo of every receipt, you ensure the documentary evidence survives even if the physical paper does not.

Receipt Rules for Travel, Meals, and Entertainment

The IRS watches these categories like a hawk because they are the most common areas for personal expenses to be disguised as business deductions.

To keep a meal deduction, the "Who, What, Where, When, and Why" must be recorded. You are legally required to document:

- The names: Exactly who attended the meal.

- Business relationship: Their title or role (e.g., "Account Executive at ABC Corp").

- Business purpose: The specific topic discussed (e.g., "Discussion of Q4 partnership renewal").

Example: A $50 dinner for an employee traveling alone is a travel meal. A $150 dinner with a client is a "Business Meal," and without those three specific data points above, the IRS can (and will) disallow the entire deduction.

The $25 Gift Limit

If you send a holiday gift basket to a loyal client or a thank you gift to a vendor, you can only deduct up to $25 per person, per year.

- The documentation: You must keep the receipt to prove the item’s value was at or below that cap.

- The nuance: This limit applies to the actual gift. Incidental costs, like insurance or gift wrapping, generally don't count toward the $25 limit, but you need the itemized receipt to prove the breakdown of those costs.

Office Supplies and Recurring Essentials

Don’t let small runs to Staples, Amazon Business, or local vendors fly under the radar just because they are under $75. These are considered essentials and require mandatory receipts for two critical reasons:

- Budget accuracy: A $40 purchase for office supplies or a software subscription needs to be coded to a specific department or project to ensure company-wide spending is tracked correctly.

- Audit defense: High-frequency, low-dollar purchases are often used by auditors to establish a pattern of negligence. If you can’t produce receipts for small recurring costs, an auditor may decide to expand their search into your larger, five-figure operational expenses.

The bottom line: A "receipt for everything" policy isn't just about following the law—it's about protecting your cash flow and ensuring that every dollar spent is a dollar you can actually deduct.

The Cohan Rule: A Hail Mary, Not a Strategy

In a famous court case (Cohan v. Commissioner), George M. Cohan was allowed to estimate his travel expenses because he proved he traveled, even though he had no receipts. This established the Cohan Rule, which allows courts to accept reasonable estimates for some expenses.

Why You Should Never Rely on It

- It does not apply to Travel, Meals, Entertainment, or Gifts (Section 274(d) overrides it).

- It is a courtroom defense, not a tax return strategy. If you are citing the Cohan Rule, you are already in deep trouble.

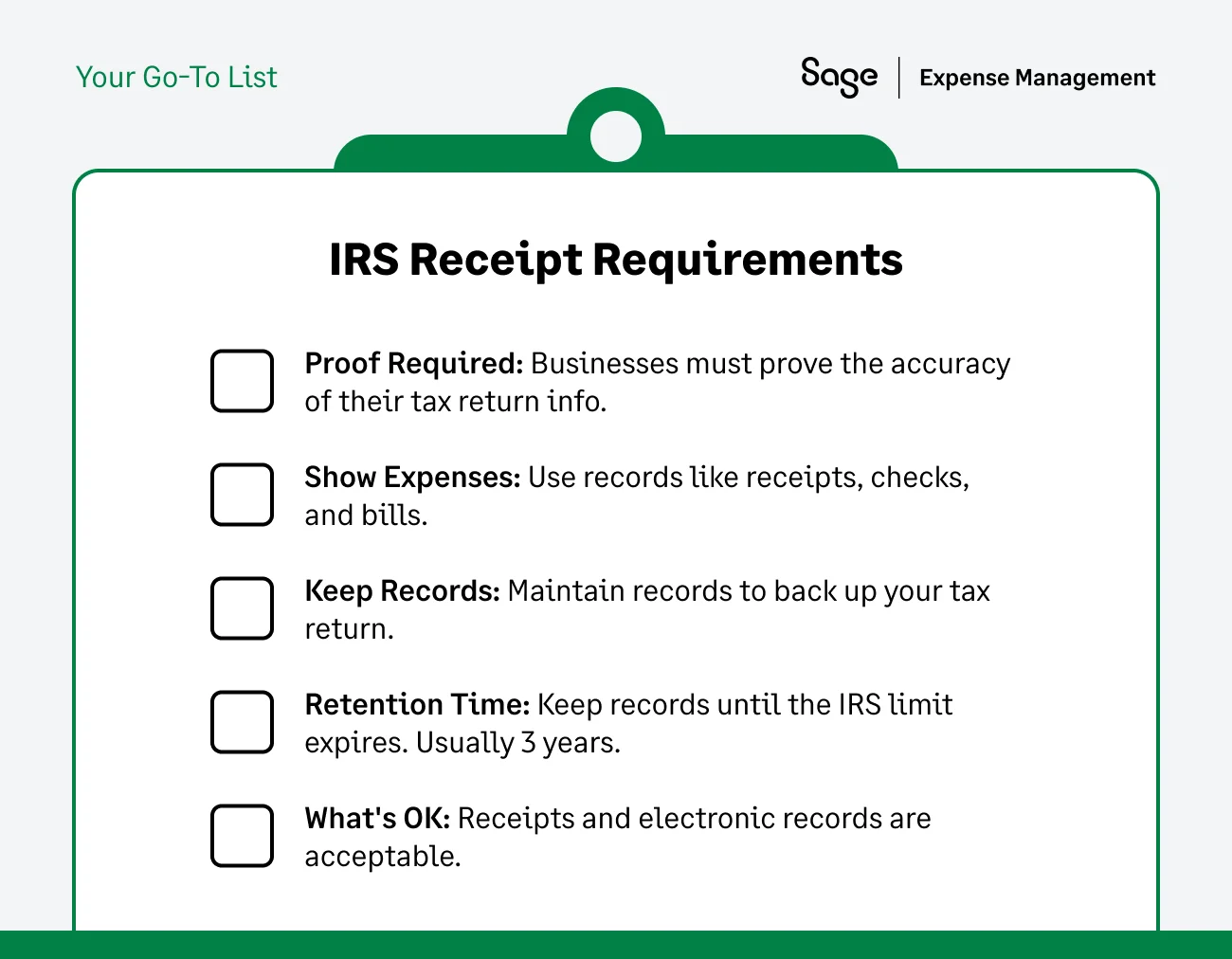

How Long Does the IRS Require to Keep Receipts?

The length of time you must keep a document depends on the "period of limitations"—the window during which the IRS can audit your return or you can amend it.

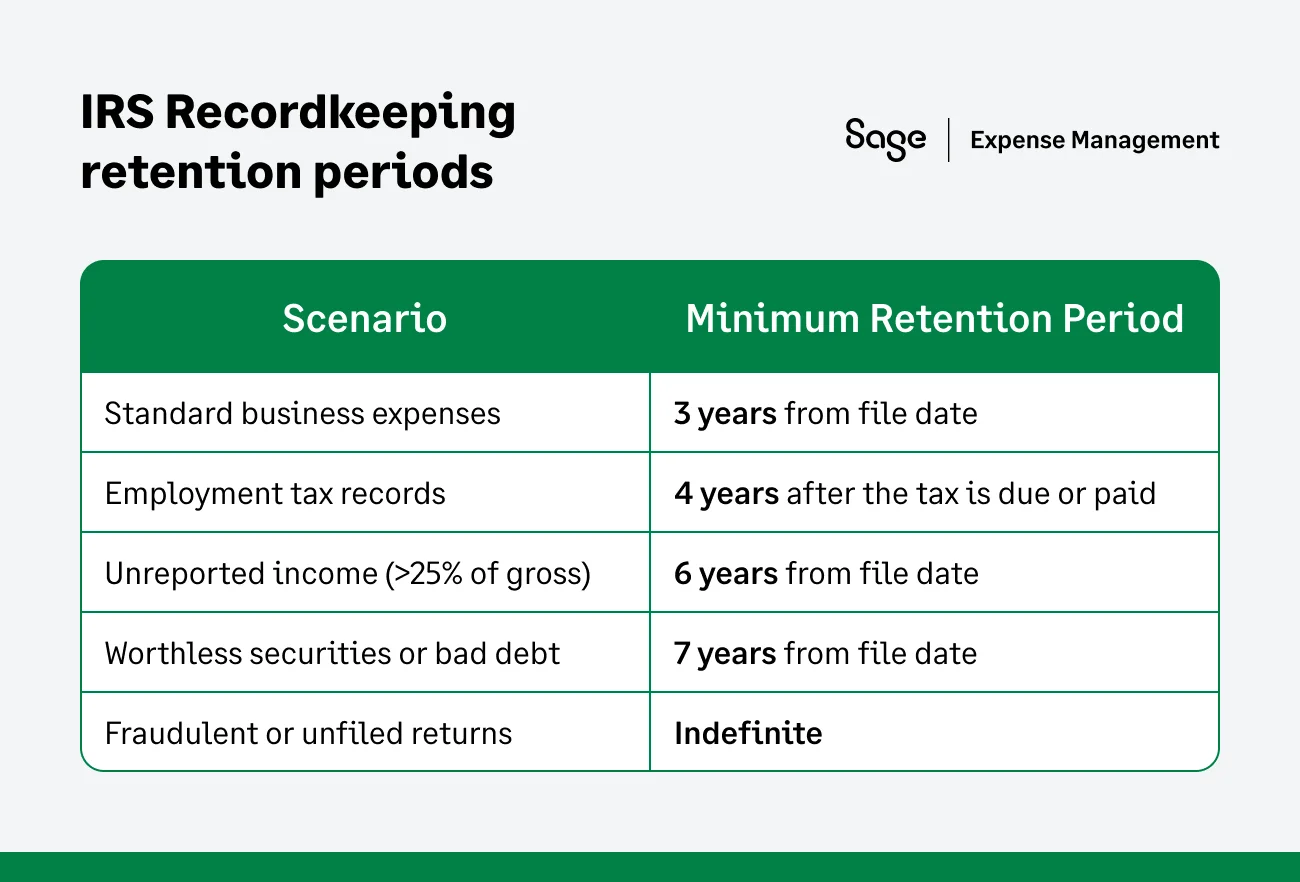

The 3-Year Golden Rule

For most businesses, the statute of limitations is three years from the date you filed the return or the date the tax was due, whichever is later. If you file your 2024 taxes on April 15, 2025, you are generally safe to purge those receipts after April 15, 2028.

The 6-Year Substantial Understatement Rule

If you fail to report more than 25% of your gross income, the IRS extends its audit window to six years. Because accidental income omissions happen, many tax pros recommend a 6-year retention policy just to be safe.

The 7-Year Bad Debt Exception

If you file a claim for a loss from worthless securities or a bad debt deduction, you must keep records for seven years.

Indefinite (The No-Limit Zone)

There is no statute of limitations if you fail to file a return or if you file a fraudulent one. In these cases, the IRS can come knocking twenty years later, and the burden of proof is still on you.

Assets (The Lifetime Rule)

For property like vehicles, machinery, or buildings, you must keep records for as long as you own the asset plus the limitation period for the year you dispose of it.

Why? You need to prove your basis (the original cost plus improvements) to calculate your gain or loss when you sell it.

Employment Taxes

If you have employees, keep all payroll tax records for at least four years after the tax becomes due or is paid.

What Happens If You Don’t Have Receipts During an Audit?

An audit without receipts isn't an automatic game over, but it puts you in a defensive position where the IRS holds all the cards.

Disallowed Deductions

If you cannot substantiate a business expense, the IRS simply removes the deduction.

The result: That $10,000 deduction is reclassified as profit. If you’re in a 25% tax bracket, you suddenly owe an extra $2,500 in back taxes for that one missing receipt alone.

Interest (The Daily Clock)

The IRS doesn't just ask for the back taxes; they charge interest from the original due date of the return. This interest is compounded daily, meaning the longer the audit takes, the more you owe.

Negligence Penalty (20%)

If the IRS determines your lack of receipts is due to "negligence or disregard of rules" (i.e., you didn't make a reasonable attempt to keep records), they can add a penalty of 20% of the underpaid tax.

Example: If you owe $5,000 in back taxes due to missing receipts, a negligence penalty adds another $1,000 to your bill.

Civil Fraud Penalty (75%)

This is the "nuclear option." If the IRS finds clear evidence that you intentionally tried to evade taxes—such as creating fake receipts or destroying records after an audit started—they can impose a penalty of 75% of the underpayment.

Challenges in Receipt Management

Even with a perfect understanding of the rules, the "real world" often gets in the way of compliance. For most businesses, receipt management fails not because of bad intent, but because of these three persistent friction points:

The Fading Problem

Most retail receipts are printed on thermal paper, which is chemically treated to react to heat. When these receipts are left in a hot vehicle, on a sunny dashboard, or even just stored in a warm office cabinet, they eventually turn into blank, white strips of paper.

The IRS is clear: if it’s unreadable, it’s not proof. A faded receipt is functionally identical to a lost one in the eyes of an auditor.

Commingling (The Mixed Receipt)

It’s a common scenario: an employee goes to a big-box store for office supplies or project materials but adds a personal item—like a soda, a magazine, or a snack—to the same transaction. This creates a "commingled" receipt.

During an audit, these personal items are "red flags" that can lead an auditor to scrutinize the entire business relationship with that vendor. Managing this manually requires tedious line-item splitting, which is a significant drain on finance's time.

The Human Factor (Administrative Friction)

Your employees were hired for their specific skills—whether they are project managers, sales reps, or site supervisors—not to be part-time accountants. Administrative compliance is often the last thing on their minds at the end of a busy day.

This leads to the "Month-End Chase," where finance teams are forced to "pull teeth" to get documentation for weeks-old charges.

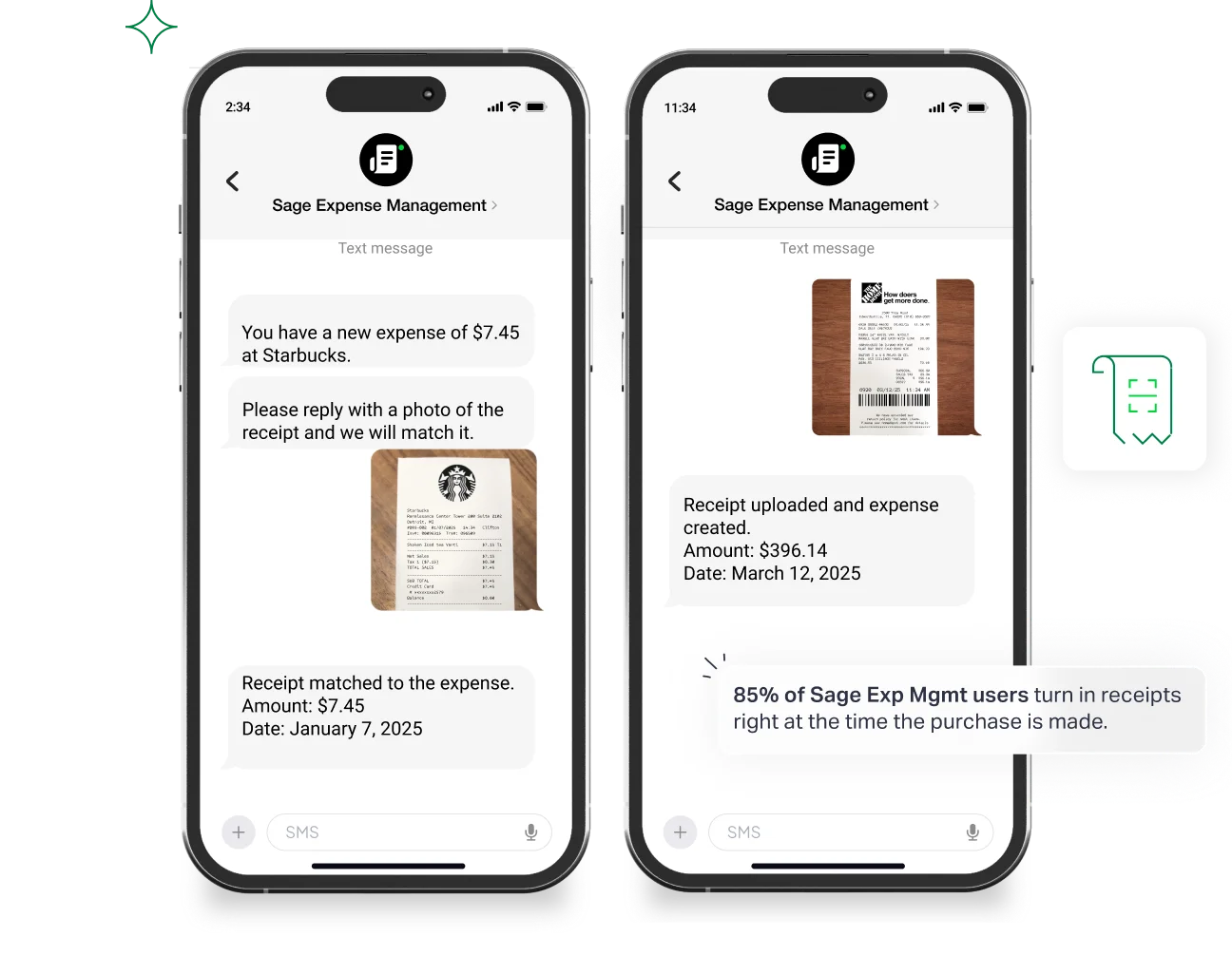

How Sage Expense Management Can Help

The era of the "shoebox full of receipts" is officially over. Modern expense management tools are designed to automate IRS compliance by removing the friction from the employee and the guesswork from the finance team.

Digital Compliance

Sage Expense Management allows employees to snap a photo of a receipt and submit it via text message the moment they receive it.

That image is instantly uploaded and stored in a secure, IRS-compliant cloud environment.

This fulfills the requirements of Revenue Procedure 97-22, ensuring your "documentary evidence" is legible, permanent, and easily accessible for years to come—long after the original thermal paper has faded.

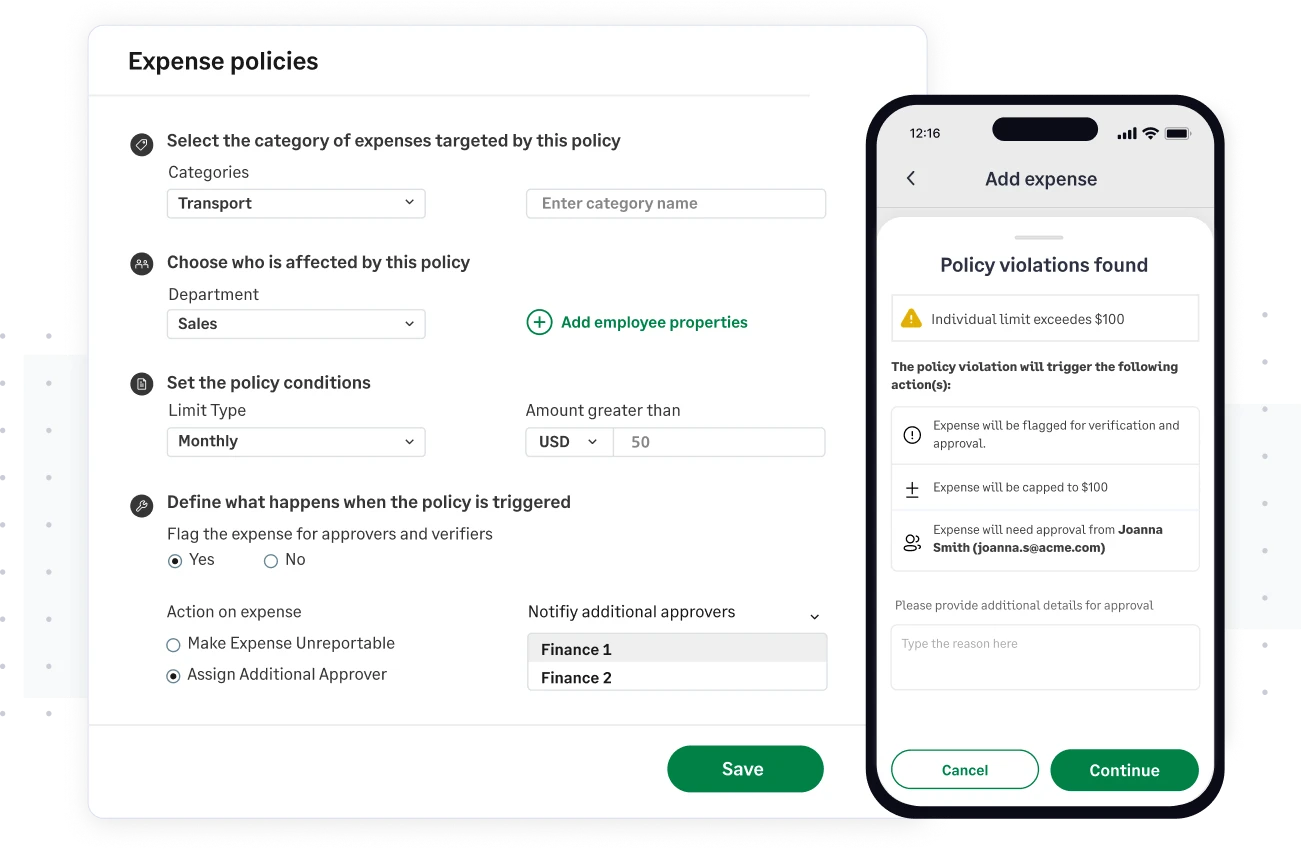

Real-Time Policy Enforcers

Instead of waiting 30 days to realize a $200 travel expense is missing a receipt, the system acts as a digital gatekeeper. It can automatically flag any transaction over the $75 threshold (or your own custom company limit) that doesn't have an attached image.

By prompting the employee to upload the receipt immediately via text or app, you stop the "reimbursement-without-proof" leak before it even hits your books.

A One-Click Audit Trail

When an auditor asks for proof, you shouldn't have to go digging through filing cabinets or messy digital folders. Sage Expense Management creates a permanent, bi-directional link between the credit card charge in your accounting system and the specific receipt image.

This "Documentary Evidence" is just one click away, allowing you to answer any IRS inquiry with confidence and speed.

{{chasing-receipts="/cta-banners"}}

Common FAQ's

1. Are Scanned and Digital Receipts IRS-Compliant?

Yes. In fact, they are preferred. According to IRS Revenue Procedure 97-22, digital receipts are fully distinct and legal as long as they are:

- Legible (readable).

- Accessible (you can retrieve them when asked).

- Secure (they can't be altered).

Why digital wins: Thermal paper (the shiny paper receipts are printed on) is chemically designed to fade. If you store a thermal receipt in a folder for 3 years, it will likely come out as a blank white strip. A blank strip is a disallowed deduction. A digital scan lasts forever.

2. What Receipt Alternatives Can You Use?

You lost the receipt. It happens. Can you still claim the deduction? Maybe. You need secondary evidence.

3. Is a Credit Card Statement Enough?

No. This is the most common audit failure. A bank statement shows Proof of Payment (money left your account), but it does not show Proof of Expense (what you bought).

Example: A line item on your Visa statement says: "Target - $100."

- Auditor's question: Did you buy office supplies, or did you buy groceries and a video game?

- The verdict: Without the itemized receipt or a detailed invoice, the statement alone is often insufficient.

4. What is the Maximum I Can Claim Without Receipts?

There is no standard deduction for business expenses. You cannot simply claim "$5,000 for supplies" without proof.

However, if you are an employee claiming per diem rates for travel (meals and incidental expenses) under an accountable plan, you may not need receipts for the meals themselves, provided you have proof of the travel (dates/location).