Key Takeaways

- A flat car allowance is taxable income by default — it's added to wages, subject to FICA, federal, and state withholding, and reported on the W-2.

- Reimbursements made under an IRS-qualifying "accountable plan" are not taxable to the employee and not deductible as wages by the employer.

- The 2025 IRS standard mileage rate is 70 cents per mile for business use.

- An accountable plan must satisfy three tests: business connection, substantiation, and return of excess — within "reasonable period of time" safe harbors of 30, 60, and 120 days.

- The TCJA eliminated unreimbursed employee business expense deductions for W-2 employees through 2025, making plan structure more important than ever.

- FAVR (Fixed and Variable Rate) allowances offer a tax-free alternative that reflects actual regional driving costs.

Some employers leave it up to employees to figure out whether their car allowance shows up as taxable income on their W-2. That's a problem — because the answer depends entirely on how the plan is structured, and getting it wrong costs both sides money.

This guide explains how the IRS treats car allowances in 2025, when they're taxable, when they're not, and how to structure a plan that keeps reimbursements tax-free for everyone involved.

What Is a Car Allowance?

A car allowance is a fixed periodic payment — usually monthly — that an employer gives an employee to cover the cost of using a personal vehicle for business purposes. Unlike a per-mile reimbursement, an allowance pays the same amount regardless of how much the employee actually drove.

Car allowances are common for sales reps, field service technicians, and any role where driving for work is routine but the employer doesn't want to maintain a fleet of company vehicles.

The catch: a flat allowance with no substantiation is taxable income. To make a vehicle reimbursement tax-free, employers need to use one of several IRS-approved plan structures.

Car Allowance vs. Mileage Reimbursement vs. FAVR vs. Company Car

These four arrangements are often used interchangeably in conversation, but the IRS treats them very differently. The table below summarizes how each works:

Why Companies Offer Car Allowances

Car allowances help employers attract and retain employees in driving-heavy roles without the overhead of managing a fleet.

They're also predictable for budgeting purposes — finance teams know exactly what vehicle costs will be each month, unlike per-mile reimbursements that fluctuate with travel volume. The trade-off is taxability, which is why many companies eventually move from flat allowances to accountable plans or FAVR programs as they grow.

The IRS Rules and Regulations on Car Allowances

The IRS treats vehicle reimbursements under the framework set out in IRC Section 62(c) and Treas. Reg. 1.62-2. Whether a payment is taxable depends entirely on whether the plan qualifies as "accountable" — meaning it satisfies three specific IRS tests.

The full framework is detailed in IRS Publication 463, which is the live, authoritative IRS publication for travel, gift, and car expenses.

How the IRS Classifies Vehicle Reimbursements

Many employers offer car allowance reimbursement because it helps them attract and keep good staff. If you receive a car reimbursement benefit, no matter the form, IRS rules apply.

The IRS allows employees to calculate vehicle expenses for reimbursement in two ways:

- Actual expense method: based on actual costs incurred while driving for work — vehicle maintenance, gas, tires, oil changes, insurance, and depreciation, allocated by business-use percentage.

- Standard mileage rate method: a per-mile rate set annually by the IRS that bundles all those costs into a single number.

The 2025 Standard Mileage Rate

For 2025, the IRS standard mileage rates are:

- Business use: 70 cents per mile

- Medical or moving (Armed Forces only): 21 cents per mile

- Charitable use: 14 cents per mile

If an employee drives 100 business miles, they're entitled to $70 in reimbursements under the standard mileage rate. The IRS announces new rates each December, so verify the current year's rate before applying it.

Is Car Allowance Taxable?

Yes, by default. A flat car allowance with no substantiation is fully taxable wages — subject to federal income tax, FICA (Social Security and Medicare), and state income tax. However, payments made under an accountable plan are not taxable to the employee and not reported as wages on the W-2.

The deciding factor is whether the plan meets the three IRS accountable plan tests. If it does, the money flows tax-free. If it doesn't, every dollar gets added to the employee's W-2 Box 1.

The Accountable Plan

Under an accountable plan, employees must report car expenses and return any excess reimbursement to the employer within a reasonable amount of time. The IRS defines what "reasonable" means in Publication 463 and Treas. Reg. 1.62-2(g).

Employees must also keep detailed records showing the date, destination, mileage, business purpose, and time of each trip. When you make your employee's W-2, you don't have to report accountable plan reimbursements as wages — they're excluded from Box 1 entirely.

The Three IRS Tests (Business Connection, Substantiation, Return of Excess)

For a plan to qualify as accountable, it must satisfy all three of the following tests under Treas. Reg. 1.62-2:

- Business connection: the expenses must have a business connection — meaning they were paid or incurred while performing services as an employee.

- Substantiation: the employee must adequately account for the expenses to the employer within a reasonable period of time. This means providing the date, place, business purpose, and amount.

- Return of excess: the employee must return any amount paid in excess of the substantiated expenses within a reasonable period of time.

If a plan fails any one of these three tests, it becomes a non-accountable plan — and every dollar paid under it is taxable wages.

The "Reasonable Period of Time" Safe Harbors (30/60/120 days)

The IRS provides three safe harbors that automatically meet the "reasonable period of time" requirement under Treas. Reg. 1.62-2(g):

- 30 days: an advance is reasonable if given within 30 days of when the expense is paid or incurred.

- 60 days: the employee must substantiate the expense within 60 days of paying or incurring it.

- 120 days: the employee must return any excess to the employer within 120 days of paying or incurring the expense.

A "periodic statement" method is also acceptable: if the employer provides a periodic statement (at least quarterly) listing amounts paid in excess of substantiated expenses, employees have 120 days from the statement date to substantiate or return the excess.

The Non Accountable Plan

If your employees do not provide proof of expenses for car allowances or mileage reimbursement, the plan is non-accountable by IRS standards. The IRS doesn't penalize the employer directly — it taxes the employee.

In such cases, the entire car allowance or mileage reimbursement becomes taxable wages on the employee's W-2. This is the default treatment for any flat monthly allowance with no substantiation requirement.

How Non-Accountable Allowances Are Taxed (FICA, federal income, state)

Non-accountable plan payments are treated identically to regular wages. They're subject to:

- Federal income tax withholding at the employee's regular rate.

- FICA taxes — 6.2% Social Security (up to the $176,100 wage base for 2025) and 1.45% Medicare, paid by both employee and employer.

- FUTA — federal unemployment tax, paid by the employer.

- State income tax withholding in states that levy income tax.

The employer effectively pays an additional 7.65% on top of the allowance amount through the employer-side FICA match — a real cost that's invisible until you do the math.

How They Appear on the W-2

Non-accountable plan payments are included in Box 1 (Wages, tips, other compensation), Box 3 (Social Security wages), and Box 5 (Medicare wages) of the employee's W-2.

There's no separate code or line item indicating the payment was a car allowance — it just looks like wages. Accountable plan reimbursements, by contrast, generally don't appear on the W-2 at all (with limited exceptions for amounts exceeding the federal rate, which appear in Box 12 with code L).

What Happens If an Accountable Plan Fails One of the Tests

This is more common than employers realize. A plan that's set up as accountable can be retroactively reclassified as non-accountable if the employee fails to substantiate within the timeline, or if the employer fails to require the return of excess advances.

The consequence is significant: every dollar paid under the plan during the failure period becomes taxable wages, retroactive to the year of payment. This may require issuing corrected W-2s (Form W-2c) and amending payroll tax filings.

As per IRS Publication 463, even partial non-compliance can taint the entire plan, which is why automated substantiation tools have become standard for companies running compliant programs.

Is Car Allowance Taxable for Miscellaneous Driving?

The lines blur when employers don't offer a structured car allowance benefit, or when the plan is non-accountable. In these cases, employees often ask whether they can recover the cost of business driving on their personal tax return.

For most W-2 employees, the answer through tax year 2025 is no. The Tax Cuts and Jobs Act of 2017 eliminated the miscellaneous itemized deduction for unreimbursed employee business expenses (subject to the 2% AGI floor) for tax years 2018 through 2025, per IRS Topic No. 514. This means W-2 employees cannot deduct unreimbursed mileage on Schedule A regardless of how much they drove for work.

There are four narrow exceptions, each filed via Form 2106:

- Armed Forces reservists traveling more than 100 miles from home.

- Qualified performing artists meeting specific income tests.

- Fee-basis state or local government officials.

- Employees with impairment-related work expenses.

Self-employed individuals (including single-member LLC owners) are not affected by this rule and continue to deduct vehicle expenses on Schedule C.

Also Read

How Much of a Car Allowance Is Taxed?

Under a non-accountable plan, the entire car allowance is taxed as wages — typically reducing the employee's net amount by 25–35% depending on tax bracket and state. Under an accountable plan, none of it is taxed.

The two scenarios below illustrate the real-dollar impact for a $600 monthly allowance.

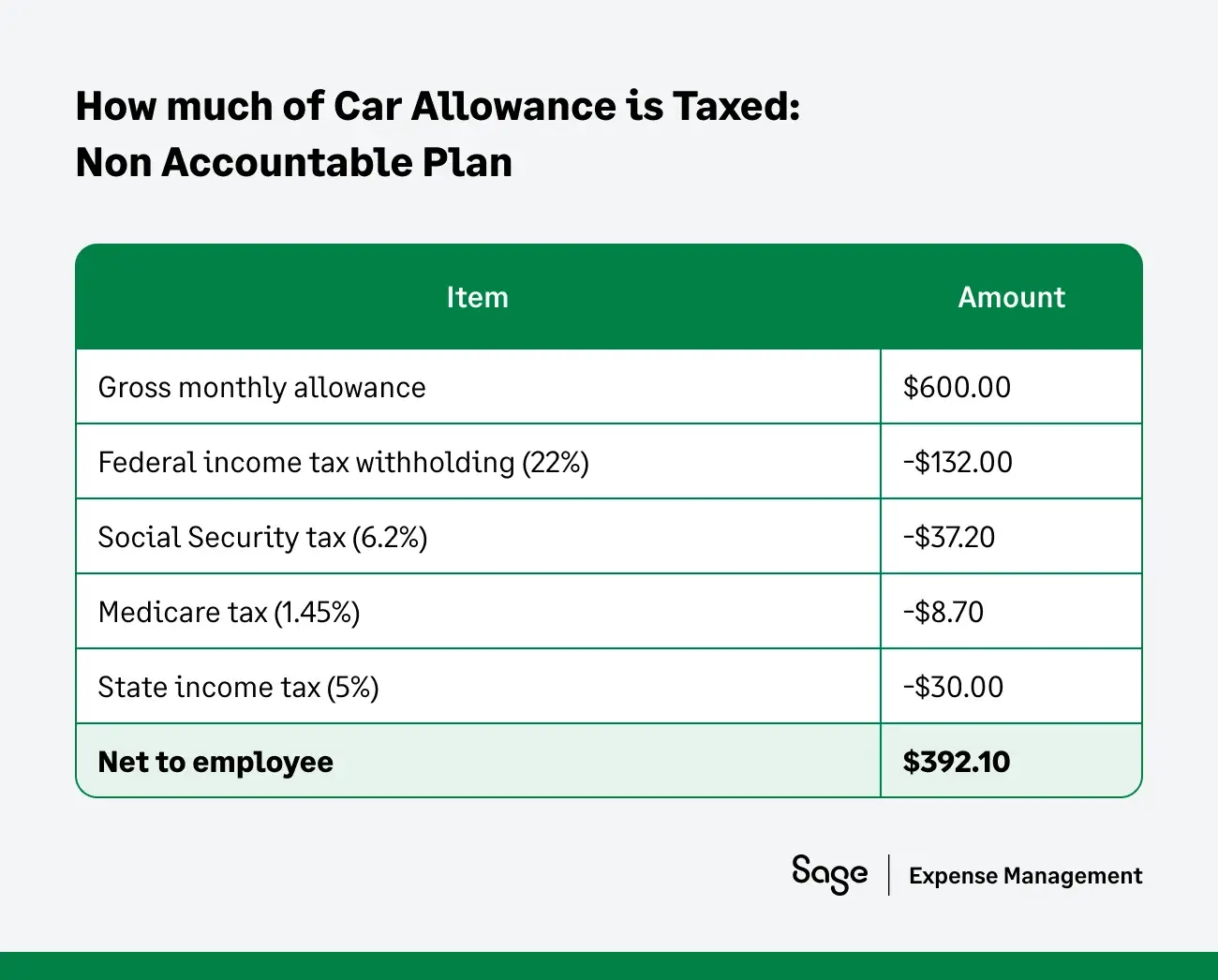

Scenario 1: $600 Monthly Allowance Under a Non-Accountable Plan

Assume an employee in the 22% federal tax bracket living in a state with 5% income tax:

The employee receives only $392 of the $600 allowance. Meanwhile, the employer also pays $45.90 in FICA match on top of the $600 — so the total cost to the employer is $645.90 to deliver $392 of value. About 39% of the allowance is lost to taxes.

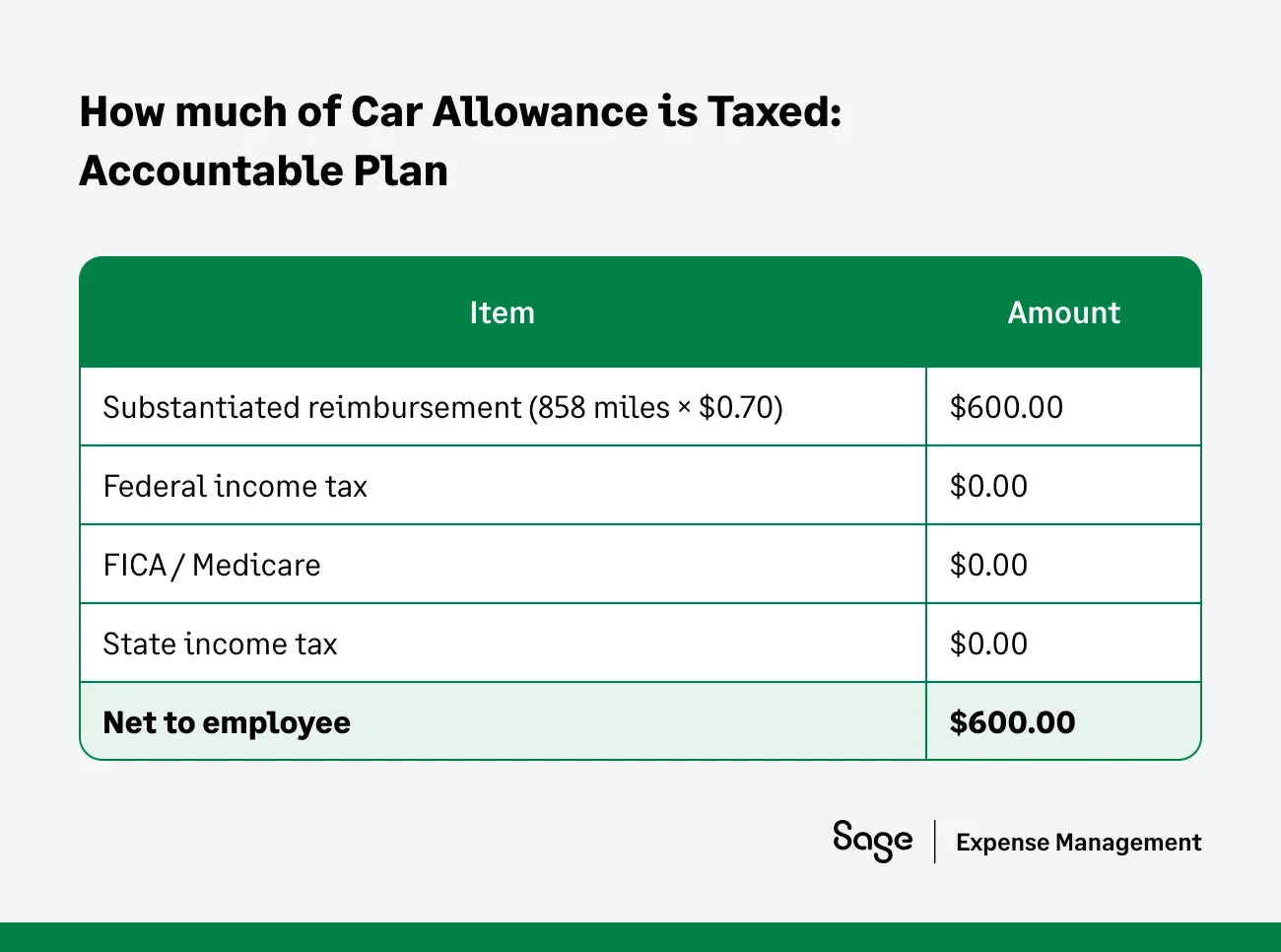

Scenario 2: $600 Monthly Allowance Under an Accountable Plan (with mileage substantiation)

Same employee, same allowance — but structured as a mileage reimbursement at the 70¢ IRS standard rate, with the employee substantiating roughly 858 business miles per month:

The employee receives the full $600. The employer pays $600 — no FICA match, no FUTA. The plan structure alone is worth roughly $250 per employee per month in this example.

Can Employees Still Deduct Unreimbursed Vehicle Expenses?

For W-2 employees, no—through tax year 2025, the TCJA eliminated the miscellaneous itemized deduction for unreimbursed employee expenses, including business mileage. The deduction is scheduled to return after 2025 unless extended by Congress.

This is the single most important shift in employee vehicle taxation in the past decade, and it's why plan structure matters more than it ever has. Before 2018, an employee with a non-accountable allowance could at least claim a partial offset on their personal return. From 2018 through 2025, that's gone.

The four narrow exceptions noted earlier (reservists, performing artists, fee-basis officials, impairment-related expenses) are the only W-2 employee categories still able to deduct vehicle expenses.

For everyone else, the only path to tax-free vehicle compensation is an accountable plan or FAVR program at the employer level.

FAVR (Fixed and Variable Rate) Allowances

A FAVR allowance is an IRS-sanctioned reimbursement structure that combines a fixed monthly payment (covering depreciation, insurance, registration, and other ownership costs) with a variable per-mile rate (covering fuel, maintenance, and tires).

When properly structured under IRS Rev. Proc. 2019-46, FAVR payments are entirely tax-free to the employee.

FAVR is increasingly the answer for companies whose employees drive significantly more than the standard mileage rate accounts for, or whose driving costs vary widely by geography.

How FAVR Works

A FAVR plan reimburses employees based on regional driving cost data — fuel prices, insurance rates, depreciation, and registration fees specific to where the employee lives and works.

The fixed portion accounts for ownership costs that don't vary with miles driven. The variable portion accounts for operating costs that scale with usage.

To qualify under Rev. Proc. 2019-46, the plan must meet specific IRS requirements: the employer must have at least 5 employees in the program (and no more than half can be management), the employee must drive at least 5,000 business miles per year, the standard automobile cost cannot exceed certain limits ($61,200 for 2025), and the plan must use a representative vehicle for cost calculations.

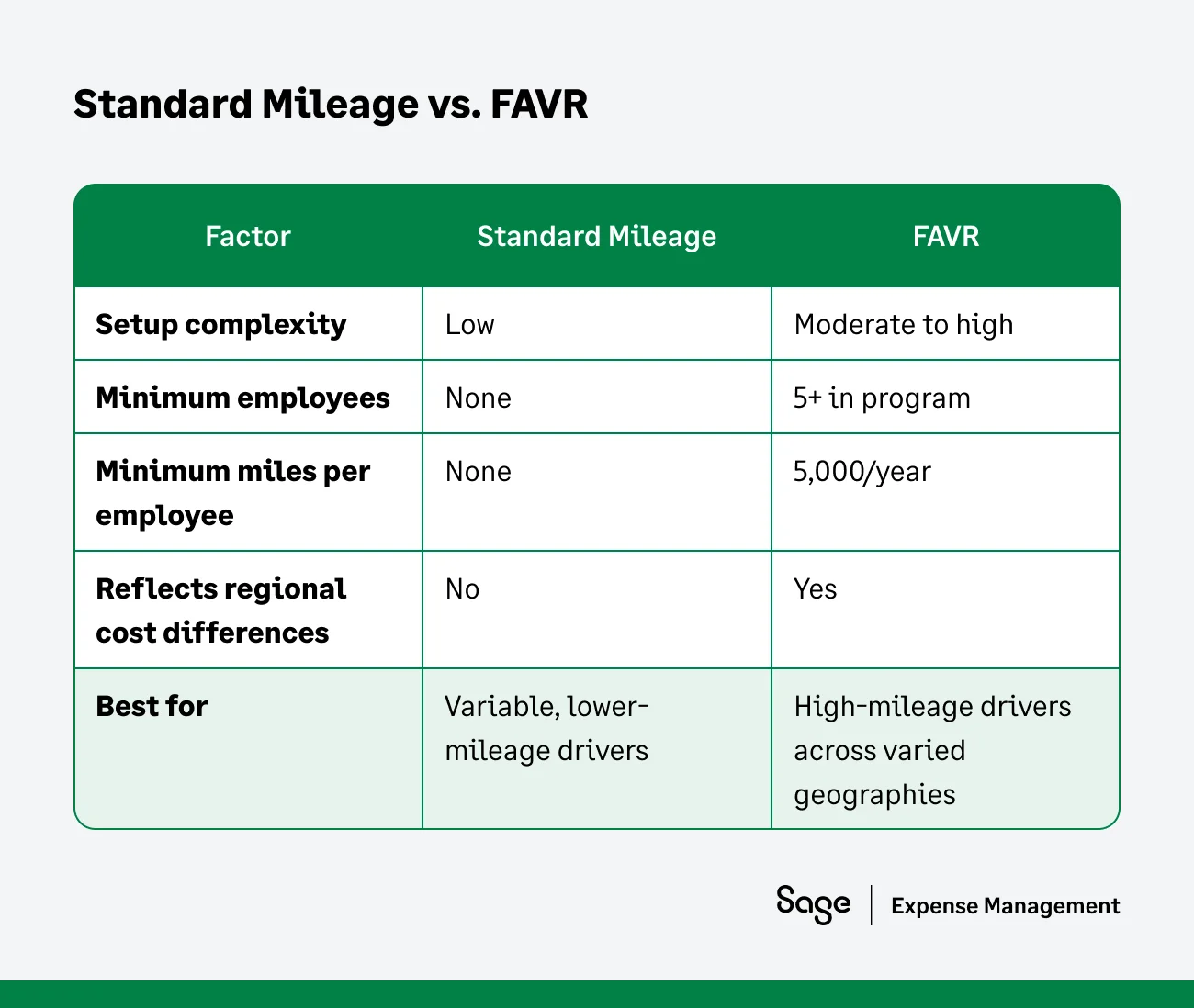

When FAVR Makes Sense vs. Standard Mileage

FAVR makes sense when employees drive a lot, in varied regions, with significantly different cost structures. For a sales rep covering rural Texas vs. one covering downtown Boston, the actual cost per mile differs substantially — and the standard 70¢ rate doesn't reflect that.

Standard mileage works better for employees with lower or more predictable mileage, smaller employers (under 5 program participants), and companies that want simpler administration. The table below summarizes the trade-offs:

How Can Businesses Structure a Compliant Car Allowance Policy?

A compliant car allowance policy requires four elements: clearly defining the plan type, setting substantiation requirements, establishing submission timelines, and documenting everything in writing. Skipping any of these turns a tax-free benefit into taxable wages.

The good news is that none of these are technically complicated — they're administrative, and they're exactly what modern expense management tools automate.

Define the Plan Type Upfront

Decide whether you're running an accountable plan, a non-accountable allowance, or a FAVR program — and communicate it clearly to employees in the offer letter or policy document.

Mixing these inadvertently is the most common compliance mistake. An employer who gives a "$600 monthly car allowance" without substantiation requirements has a non-accountable plan, even if they intended otherwise.

Set Substantiation Requirements

Specify exactly what employees must submit to substantiate vehicle expenses: a mileage log with date, destination, business purpose, and miles driven for each trip.

GPS-based mileage logs are increasingly the standard, both because they reduce employee burden and because they create a more defensible audit trail. The IRS accepts records prepared on a computer as adequate per Publication 463.

Establish Submission Timelines

Build the 30/60/120 day safe harbors directly into your policy:

- Advances must be issued within 30 days of when the expense is incurred.

- Substantiation must be submitted within 60 days of the expense.

- Excess must be returned within 120 days.

Automated reminders and submission deadlines built into your expense system are the cleanest way to enforce these without becoming the policy police.

Document the Policy in Writing

Maintain a written vehicle reimbursement policy, signed by participating employees, that spells out the plan type, substantiation requirements, timelines, and consequences of non-compliance.

If audited, the IRS will ask to see this document. Verbal policies and inconsistent practices are how plans get retroactively reclassified as non-accountable.

State Tax Considerations

Most states follow federal treatment of car allowances — taxable if non-accountable, tax-free if accountable. However, a few states have additional rules around state income tax withholding, unemployment insurance, and workers' compensation premiums on vehicle reimbursements.

California, for example, treats vehicle reimbursements above the IRS standard mileage rate as taxable wages for state purposes.

New York, Pennsylvania, and a handful of other states have specific guidance on commuting allowances vs. business mileage that diverges from federal rules.

Check your state's department of revenue or labor agency for current treatment, and consult a payroll tax advisor if you operate across multiple states.

There's also a labor-law dimension separate from tax: some states (notably California under Labor Code Section 2802) require employers to indemnify employees for all necessary expenses incurred in the course of employment, which can mandate vehicle reimbursement regardless of federal tax treatment.

How can Sage Expense Management Help with Car Allowances

Sage Expense Management automates the substantiation and reimbursement workflow that an accountable plan requires — GPS-verified mileage logs, automatic submission within the 60-day window, real-time approvals, and direct sync to payroll so reimbursements flow as non-taxable expense rather than taxable wages.

If you have employees using their personal vehicles for business, you need a structured policy. Here's what Sage Expense Management adds to make that policy actually work in practice:

- GPS-verified mileage tracking: automatic trip detection with date, route, mileage, and business purpose captured in real time. No paper logs, no manual entry, no end-of-month reconstruction.

- Text-message receipt submission: for fuel, tolls, parking, and any other vehicle-related expenses that need a receipt, employees simply text a photo to Sage Expense Management. The system extracts the merchant, amount, and date automatically and matches it to the corresponding card transaction or mileage trip — no app to download, no portal to log into.

- Accountable plan-compliant substantiation: every reimbursement is tied to a substantiated trip with the five IRS-required elements, creating an audit-ready record automatically.

- Configurable submission and approval timelines: build the 30/60/120 day safe harbors into your workflow with automatic reminders, so plans don't fail compliance because someone forgot to submit.

- Direct sync to payroll and accounting: reimbursements flow as non-taxable items into Sage Intacct, Sage 50, QuickBooks, or Xero — never accidentally coded as wages.

- Policy-level controls: set per-mile rates, monthly caps, and category rules at the plan level so policy violations are caught before reimbursement, not after.

- Real-time spend visibility: dashboards by employee, department, or region let finance teams see vehicle reimbursement spend as it happens — useful for evaluating whether a flat allowance, mileage program, or FAVR plan is the right structure.

FAQs around Car Allowances

Is a car allowance considered income?

It depends on the plan structure. Under a non-accountable plan, a car allowance is fully taxable wages and reported on the W-2. Under an accountable plan with proper substantiation, it's a tax-free reimbursement and not considered income.

Do I have to pay tax on a company car allowance?

If your employer pays a flat monthly allowance without requiring you to substantiate business miles, yes — the entire amount is taxable as wages.

If the allowance is structured as an accountable plan reimbursement (with mileage logs, business purpose documentation, and the IRS substantiation timelines), it's not taxable.

Is a car allowance better than a company car?

It depends on usage and personal preference. A car allowance gives the employee flexibility and ownership but requires them to handle maintenance, insurance, and depreciation themselves.

A company car shifts those costs to the employer but creates a taxable fringe benefit for any personal use, calculated using methods like the cents-per-mile rule or annual lease value rule per IRS Publication 15-B. For high-mileage drivers, a company car or FAVR plan often comes out ahead; for moderate drivers who prefer a personal vehicle, an accountable mileage reimbursement is usually the cleanest option.

How much should a car allowance be in 2025?

Industry surveys suggest typical car allowances range from $500–$1,000 per month for sales and field roles, with the median landing around $575 per month.

The right number depends on expected mileage, vehicle costs in your region, and whether the allowance is taxable or tax-free. A $700 taxable allowance nets the employee roughly the same as a $450 accountable plan reimbursement after taxes, which is why benchmarking should always factor in plan structure.

Can I deduct mileage if I receive a car allowance?

For W-2 employees, generally no — the TCJA eliminated the unreimbursed employee business expense deduction through tax year 2025. Even if your allowance is taxable, you cannot offset it with a personal mileage deduction.

The four narrow exceptions are Armed Forces reservists, qualified performing artists, fee-basis state/local officials, and employees with impairment-related work expenses. Self-employed individuals and single-member LLC owners are not affected and continue to deduct vehicle expenses on Schedule C.

What's the difference between a car allowance and a mileage reimbursement?

A car allowance is a fixed periodic payment (usually monthly) that doesn't depend on actual miles driven. A mileage reimbursement is a per-mile payment based on documented business miles, typically at the IRS standard rate (70¢/mile for 2025).

The tax treatment is the bigger difference: flat allowances are typically taxable, while mileage reimbursements under an accountable plan are tax-free.

Are car allowances subject to FICA and Medicare taxes?

Non-accountable car allowances are subject to both Social Security (6.2%) and Medicare (1.45%) taxes — paid by both the employee and the employer.

Accountable plan reimbursements are not subject to FICA or Medicare. This is why properly structured plans are significantly cheaper for employers, even before factoring in the value to the employee.

Can self-employed LLC owners give themselves a car allowance?

Self-employed LLC owners (single-member LLCs and partnership-taxed LLCs) don't pay themselves wages, so the "car allowance" framing doesn't apply.

Instead, they deduct actual vehicle expenses or standard mileage directly on Schedule C or the partnership return. LLC owners who've elected S-corp treatment can set up an accountable plan to reimburse themselves tax-free for business use of a personal vehicle, the same way as any other employee.

Does a car allowance affect overtime pay calculations?

It can. Under the Fair Labor Standards Act, reimbursements that approximate actual expenses (like accountable plan mileage reimbursements) are generally excluded from the regular rate of pay used to calculate overtime.

Flat car allowances that exceed reasonable expense reimbursement may be considered part of the regular rate, which would inflate overtime calculations for non-exempt employees. The Department of Labor's Field Assistance Bulletin 2020-2 provides guidance on which vehicle reimbursements qualify for exclusion.

{{mileage="/cta-banners"}}