.webp)

Nonprofit organizations play a vital role in society, driven by their mission to serve the community and make a positive impact. To effectively fulfill their purpose, nonprofits must maintain accurate and transparent financial records. This isn't just about good practice; it’s the financial backbone that ensures a mission’s sustainability, stakeholder trust, and legal compliance.

Accounting for nonprofits might seem intimidating, especially if numbers aren’t your forte. But don't worry!

This guide will break down the essentials of nonprofit accounting, providing you with the knowledge and tools you need to take control of your finances.

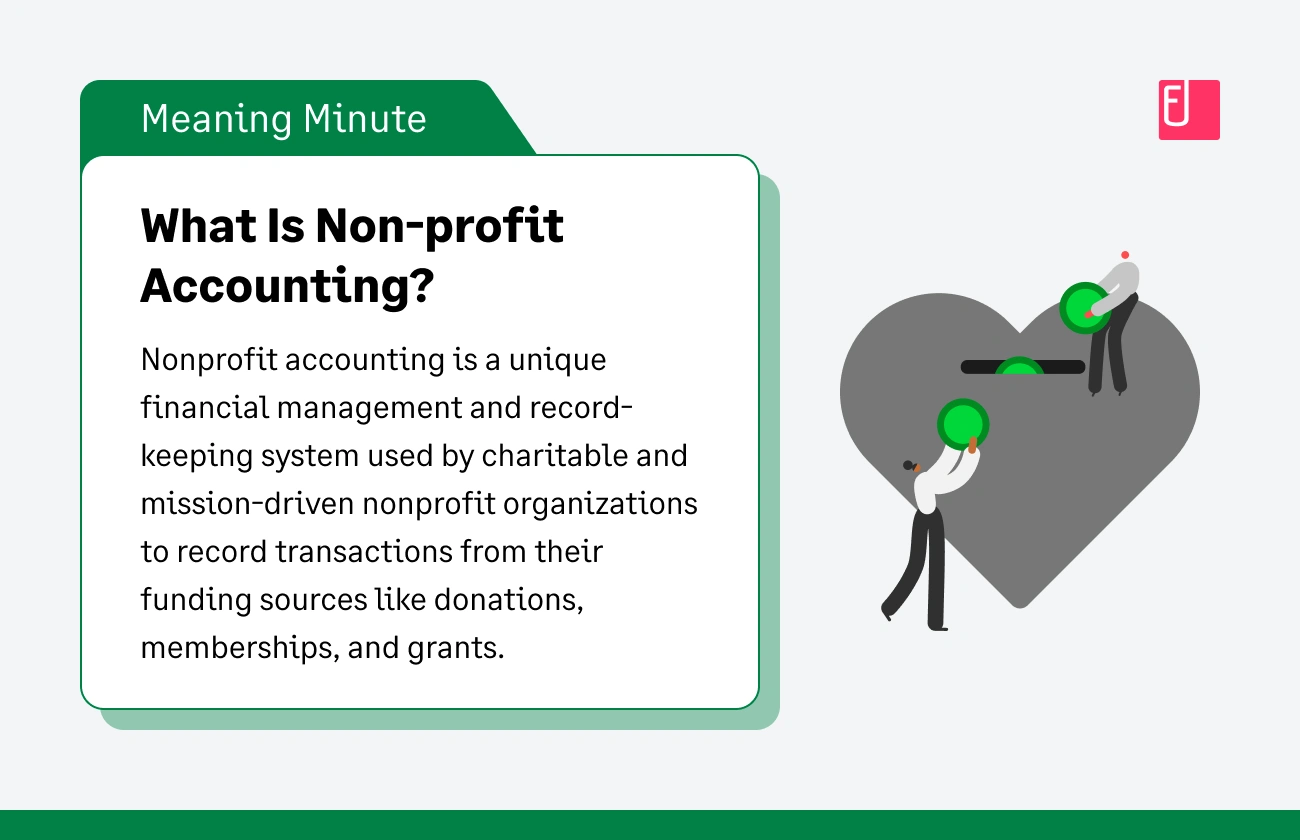

What Is Nonprofit Accounting?

Nonprofit accounting is a unique financial management and record-keeping system used by charitable and mission-driven organizations. Unlike for-profit accounting, its primary purpose is not to track profits, but to meticulously record transactions from various funding sources—like donations, memberships, and grants—to ensure accountability.

Transparency is essential in nonprofit organizations as it lets board members and donors know exactly how their money is being spent to fulfill the mission they intended to support.

Nonprofit Accounting Vs. Bookkeeping

Nonprofit bookkeeping focuses on the day-to-day financial record-keeping and management, including recording transactions and organizing receipts.

Nonprofit accounting, however, encompasses a broader scope, including financial analysis, reporting, and tax compliance. In essence, bookkeeping is the detailed work of creating a financial story, while accounting is the higher-level work of interpreting and analyzing that story.

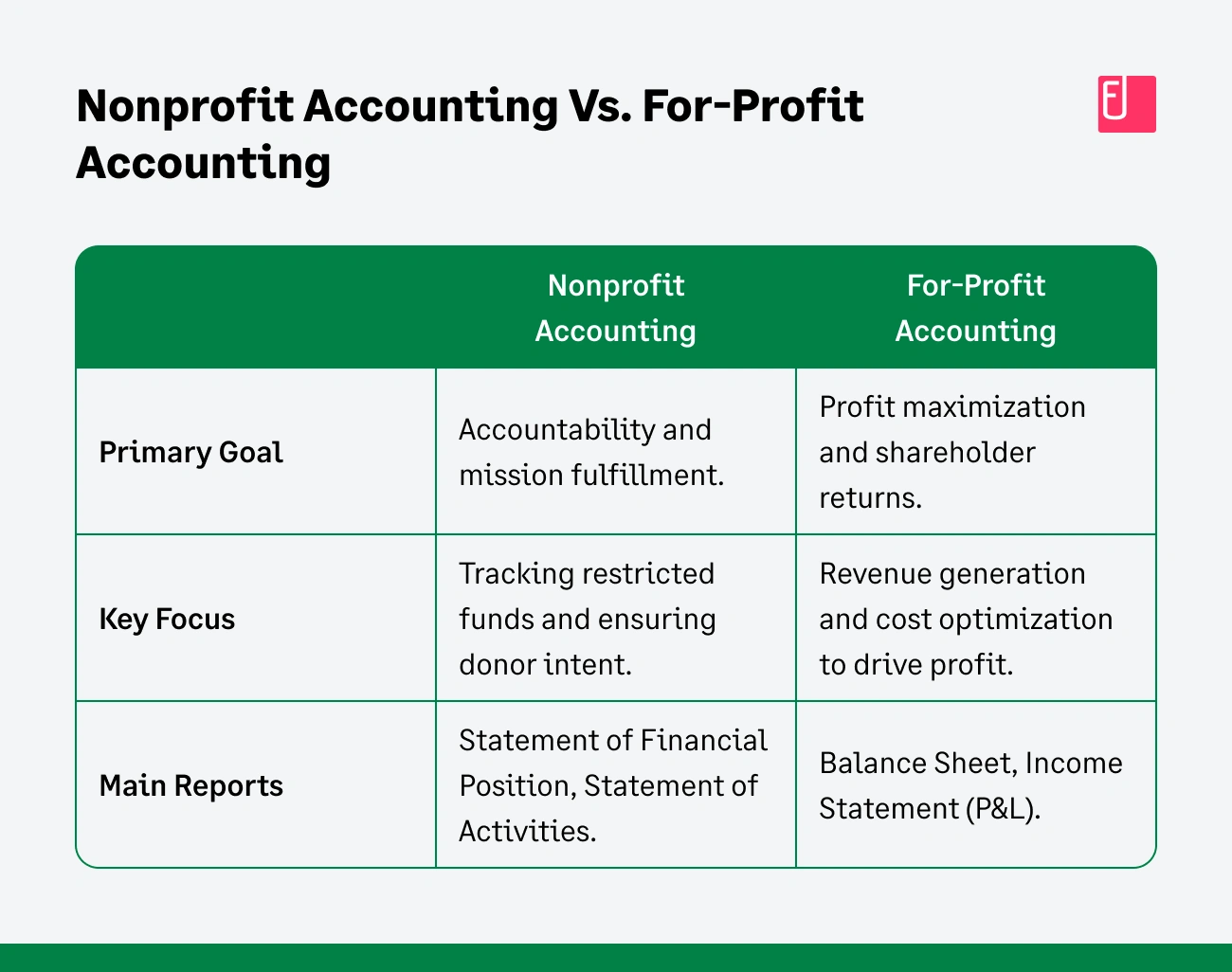

Nonprofit Accounting Vs. For-Profit Accounting

Nonprofit accounting centers on accountability and mission fulfillment. It employs fund accounting to track restricted and unrestricted funds, ensuring compliance with donor intent. Its financial statements, comprising the statement of financial position, statement of activities, and statement of cash flows, align with this mission-driven approach.

For-profit accounting, on the other hand, prioritizes profit maximization, emphasizing revenue generation and cost optimization. Its financial statements, including the balance sheet, income statement, and cash flow statement, reflect this focus on profitability.

Do Nonprofits Have To Follow GAAP?

Yes. While smaller nonprofits can use cash-based accounting, which need not be GAAP-compliant, most nonprofits must be GAAP-compliant. Adhering to GAAP is a requirement for producing accurate financial reports that are essential for qualifying for various grants and other funding sources.

Getting Started with Non Profit Accounting

The primary focus of nonprofit accounting is accountability to stakeholders and donors rather than generating profits. Nonprofit organizations follow the same fundamental accounting principles as for-profit organizations but with a few key differences.

According to Alaina Mackin, CPA, CMA, an instructor in Southern New Hampshire University’s accounting program, and SNHU accounting instructor Dan Puhl, CPA, CMA, these nine basics of accounting are fundamental for a nonprofit organization to fulfill its missions and maintain long-term sustainability.

1. Open A Separate Bank Account

Establishing a separate bank account for your nonprofit distinguishes between your personal finances and the organization's funds. This separation enhances accountability, facilitates accurate record-keeping, and simplifies tax preparation.

Additionally, many banks offer business checking accounts specifically designed for nonprofits, often with waived fees or reduced transaction costs. These tailored accounts can provide valuable features, such as multiple signatories, online banking tools, and interest-bearing options, further supporting your nonprofit's financial management needs.

2. Picking An Accounting Method

To get started, it’s essential to choose whether your organization will use a cash or accrual-based accounting system.

- Cash-based accounting: You record income and expenses when cash is received or paid.

- Accrual-based accounting: You record income and expenses according to when the transaction occurs, regardless of when the cash was received or paid.

The cash-basis accounting method is easier to maintain and is often adequate for smaller nonprofits. However, if your organization plans to receive funds from more prominent donors, the accrual method might be worth looking into.

Some nonprofits use a modified accrual accounting system called “fund accounting,” which tracks income and expenses in separate accounts or funds representing their different revenue sources, like grants or donations.

It can also help nonprofit organizations measure their existing charitable goals against financial performance.

Also Read

3. Governance And Compliance

There are two types of governance for nonprofit institutions. Public nonprofits – such as a local jurisdiction or state university hospital – follow Governmental Accounting Standards, whereas non-governmental organizations, including private foundations and charities, fall under a modified version of the Generally Accepted Accounting Principles (GAAP) that for-profit organizations use.

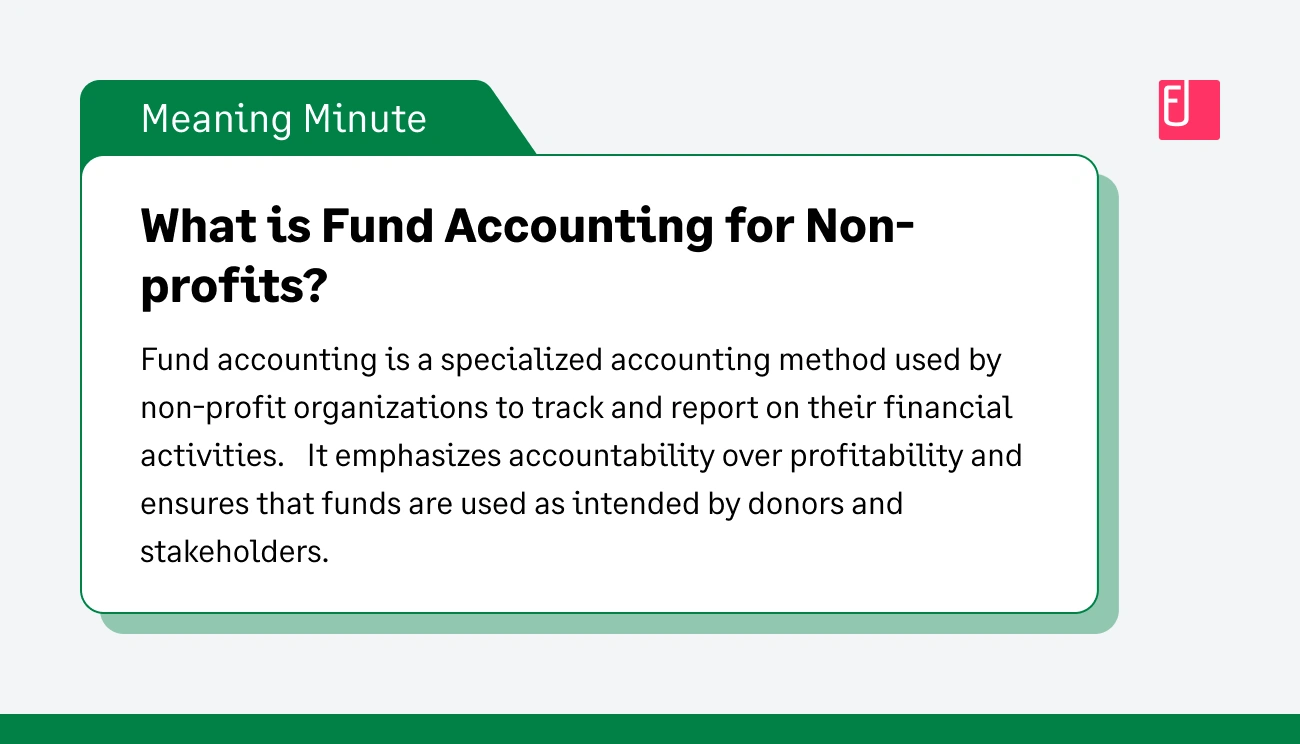

4. Fund Accounting for Nonprofits

Fund accounting is a specialized accounting method used by nonprofit organizations to track and report on their financial activities. It emphasizes accountability over profitability and ensures that funds are used as intended by donors and stakeholders.

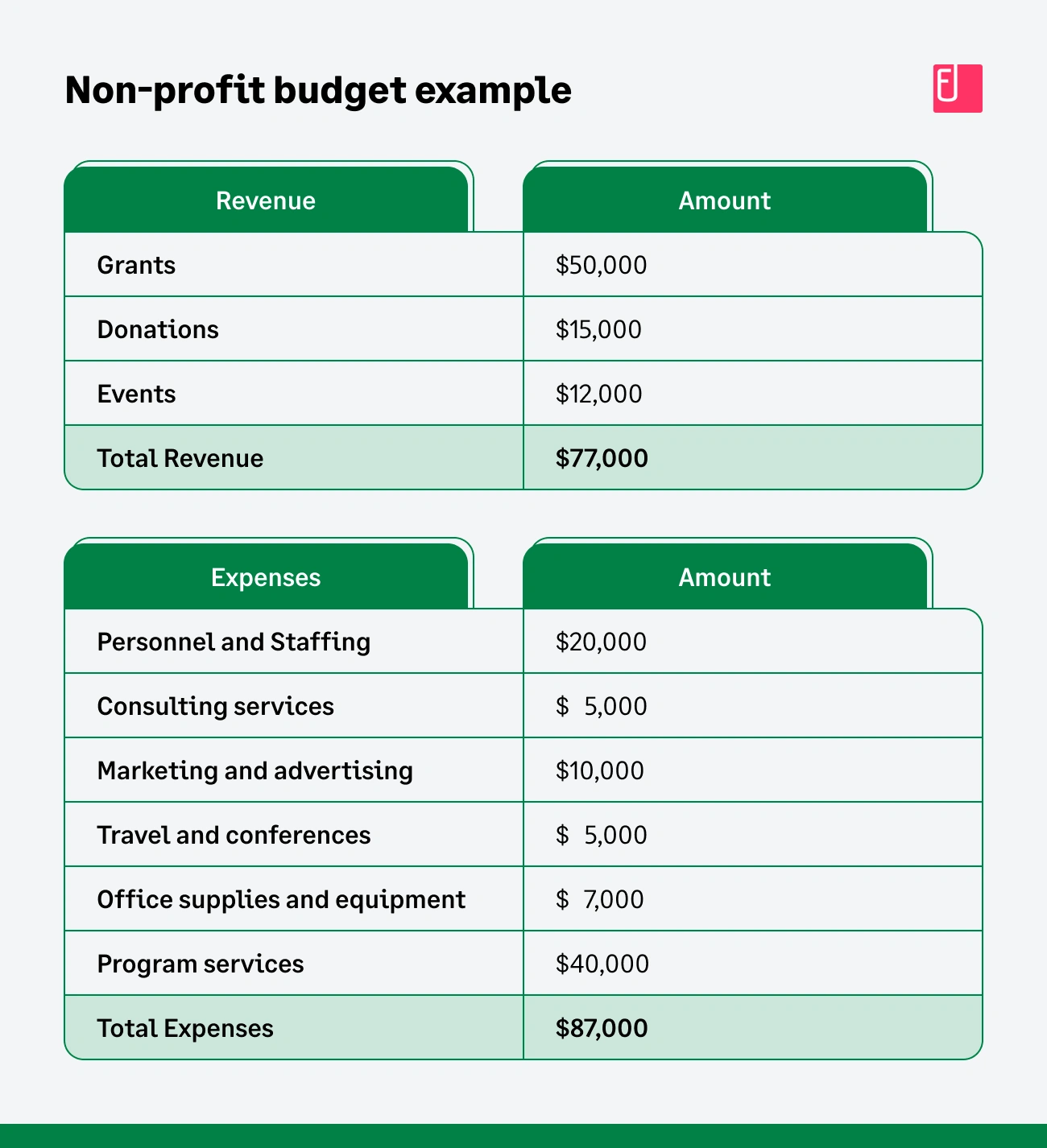

5. Budgeting and Reporting

Nonprofits should develop an annual budget that aligns with their strategic goals and mission. Regularly monitoring expenses and revenue against the budget allows for timely adjustments and ensures fiscal responsibility. Financial reports, including income statements, balance sheets, and cash flow statements, provide a snapshot of the organization's financial health.

Here are some other factors you can consider while budgeting for a nonprofit organization:

- Operating Revenue: List all income sources and consider all potential payment delays. Ensure you include federal grants, donations, and membership feeds when you project your budgets.

- Expenses: Cover all operating costs like rent, salaries, utilities, office supplies, and other overhead expenses while allocating funds.

- Program Costs: Ensure funds are earmarked to cover all necessary expenses such as program delivery materials, additional miscellaneous costs, training staff, etc.

- Contingency: Always have a reserve fund to cover unexpected costs or shortfalls so you don't have to depend on funds allocated for the program if an emergency expense arises.

- Fundraising: While planning fundraising events, ensure donations collected always exceed the cost of hosting such events.

6. Tracking Revenue and Donations

Accurate tracking of revenue and donations is at the heart of nonprofit accounting. The way you categorize and record incoming funds is a critical factor in ensuring compliance, building donor trust, and maintaining your tax-exempt status.

Contributions vs. Exchange Revenue

A contribution is a voluntary transfer of cash or property with no expectation of receiving anything of equal value in return. This includes donations, gifts, and bequests. In contrast, exchange revenue is a payment for goods or services a nonprofit provides, such as a fee for a conference or a ticket to a fundraising dinner.

A hybrid of these is a quid pro quo contribution, where a donor makes a payment that is partly a contribution and partly for goods or services.

What is a Qualified Contribution?

A qualified contribution is a donation to a qualified organization. These are typically tax-exempt organizations under Internal Revenue Code section 501(c)(3). This includes public charities, private foundations, churches, and other religious, educational, or scientific organizations.

To be considered a qualified contribution, the donation must be made to an organization that has been officially recognized as a tax-exempt entity by the IRS.

How Can Nonprofits Substantiate Contributions?

Nonprofits must maintain meticulous records of all donations, as donors need this documentation to claim their tax deductions.

- For Monetary Contributions: For cash contributions of any amount, a donor must have a bank record or a written communication from the charity showing the name of the organization, the date of the contribution, and the amount.

- For Donations of $250 or More: For any single donation (monetary or noncash) of $250 or more, the nonprofit must provide a contemporaneous written acknowledgment to the donor. This document must be provided to the donor before they file their tax return and must include:

- The name of the organization.

- The amount of the cash contribution.

- A description of any property contributed.

- A statement confirming whether the nonprofit provided any goods or services in exchange for the donation.

- If goods or services were provided, a description and a good faith estimate of their fair market value.

- For Noncash Donations: For donations of property with a claimed value over $500, the donor must file Form 8283. For noncash donations with a claimed value of more than $5,000, the nonprofit must also sign this form, verifying receipt of the property.

7. Internal Controls and Audits

Separation of duties, internal audits, and checks and balances can prevent and detect fraud or financial mismanagement. Ideally, a nonprofit organization should have a protocol in place for external audits by independent auditors. These audits objectively assess their financial statements, compliance, and internal controls.

8. Technology

Leveraging technology can streamline accounting processes and enhance financial management for nonprofits. Accounting software and expense management tools designed for nonprofits can automate fund tracking, reporting, and donor management tasks. Cloud-based solutions facilitate collaboration, data security, and accessibility.

9. Ethics and Transparency

Maintaining the trust and confidence of stakeholders and donors is essential for nonprofit organizations. Nonprofits should uphold high ethical standards in financial practices, ensuring transparency and accountability. Clear communication of financial information and disclosure of financial statements and annual reports to stakeholders are imperative to demonstrate responsible financial stewardship.

Nonprofit Accounting Financial Statements

Nonprofit organizations use financial statements to ensure transparency and accountability in reporting so that relevant stakeholders, donors, and other agencies can evaluate the organization’s financial health. Listed below are the four critical financial statements needed for nonprofit accounting.

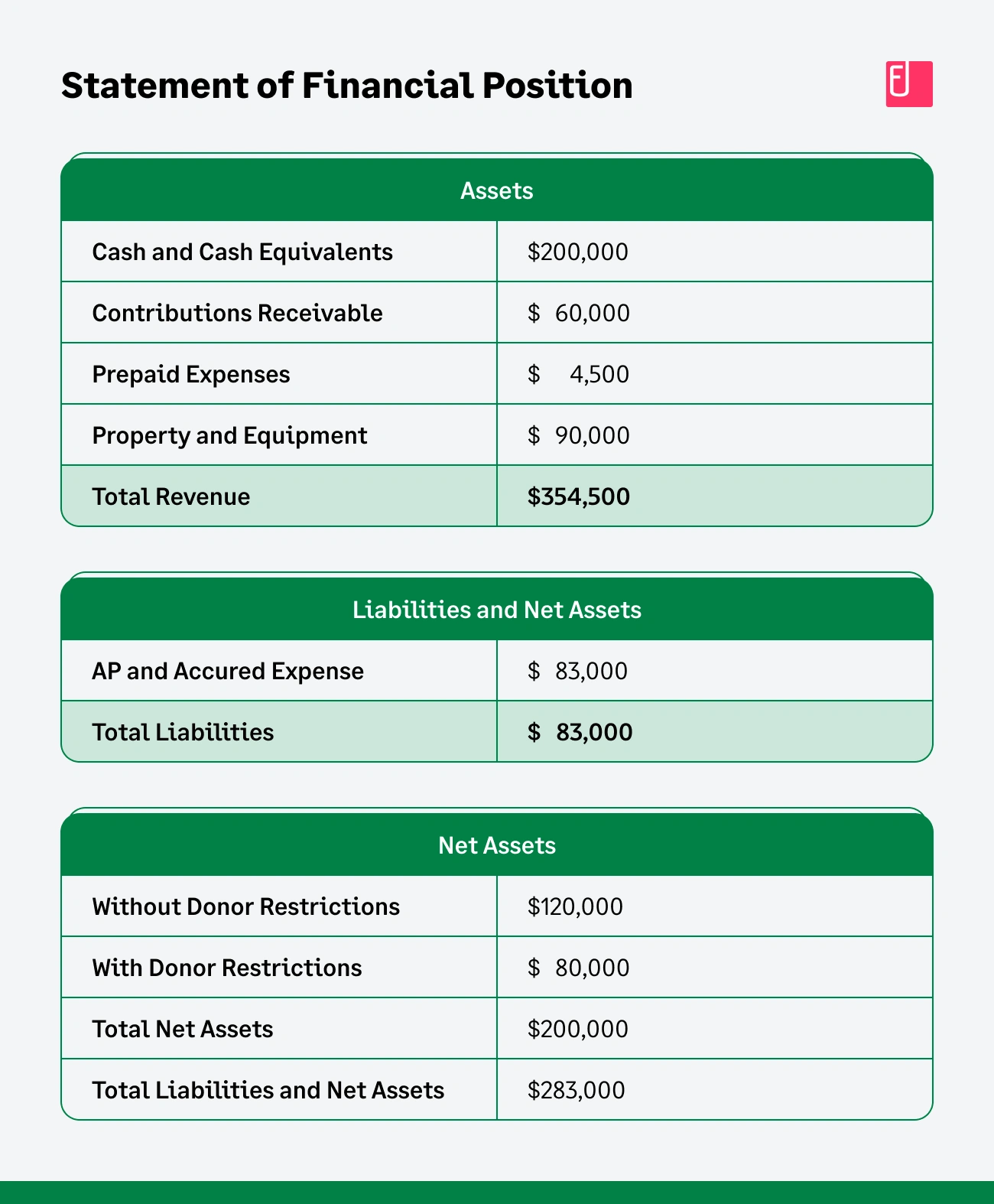

1. Statement of Financial Position (Balance Sheet)

The statement of financial position, also commonly known as the balance sheet, is a document nonprofits can use to track their liabilities, assets, and net assets. Typically, it’s calculated with the following formula:

Net Assets = Assets - Liabilities

The point of the balance sheet is to help you determine whether the organization meets its financial goals or has enough funds to continue operating or organizing new programs.

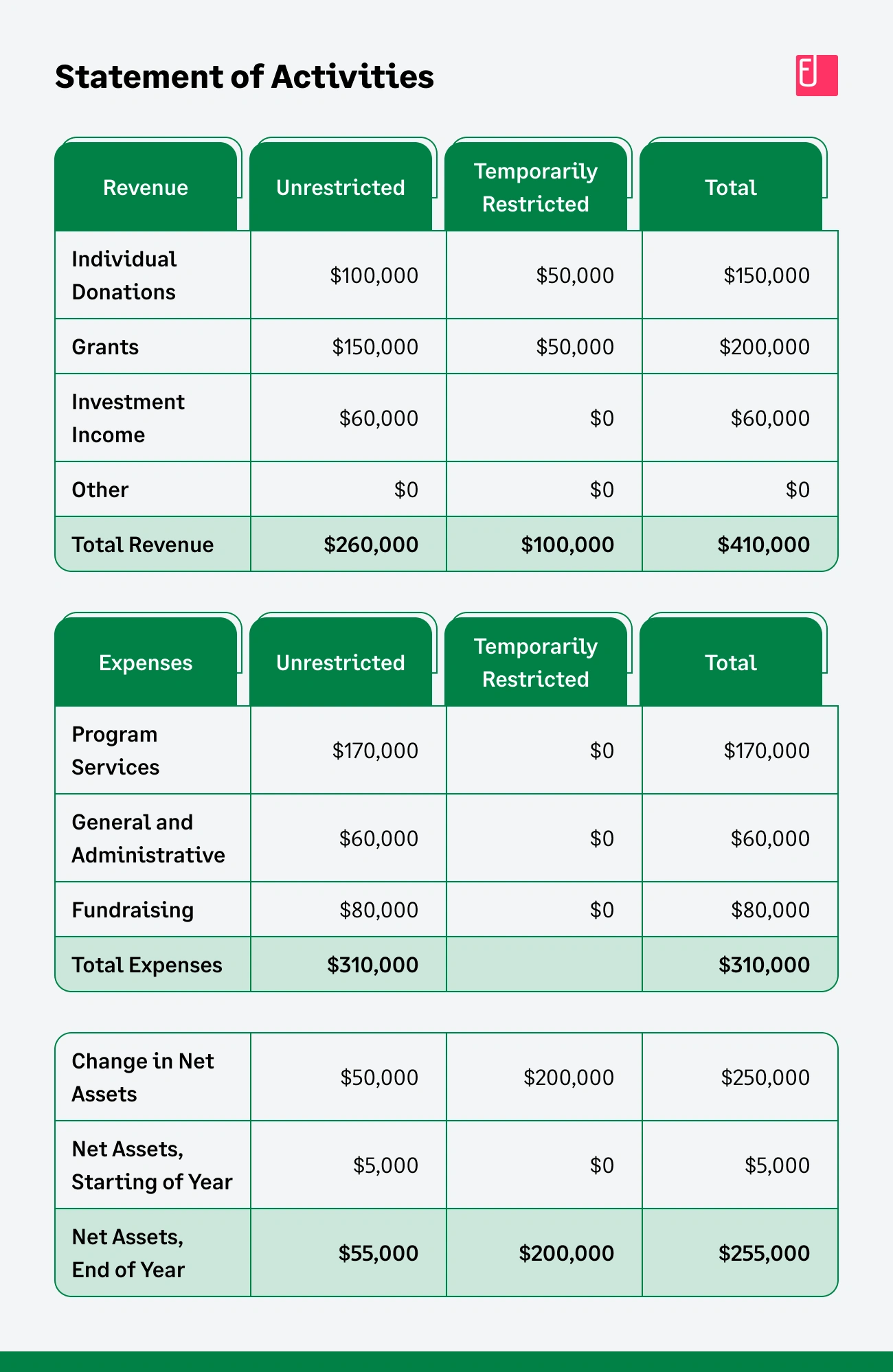

2. Statement of Activities (Income Statement)

The statement of activities is a document that shows a nonprofit’s revenues, expenses, and net assets for a specific period. It is similar to a for-profit income statement but instead of showing profit or loss, it shows the change in the organization’s net assets over a given period.

It also classifies expenses by function, showing how much money was spent on programs, fundraising, and administrative costs.

Net Income = Total Revenue - Total Expenses

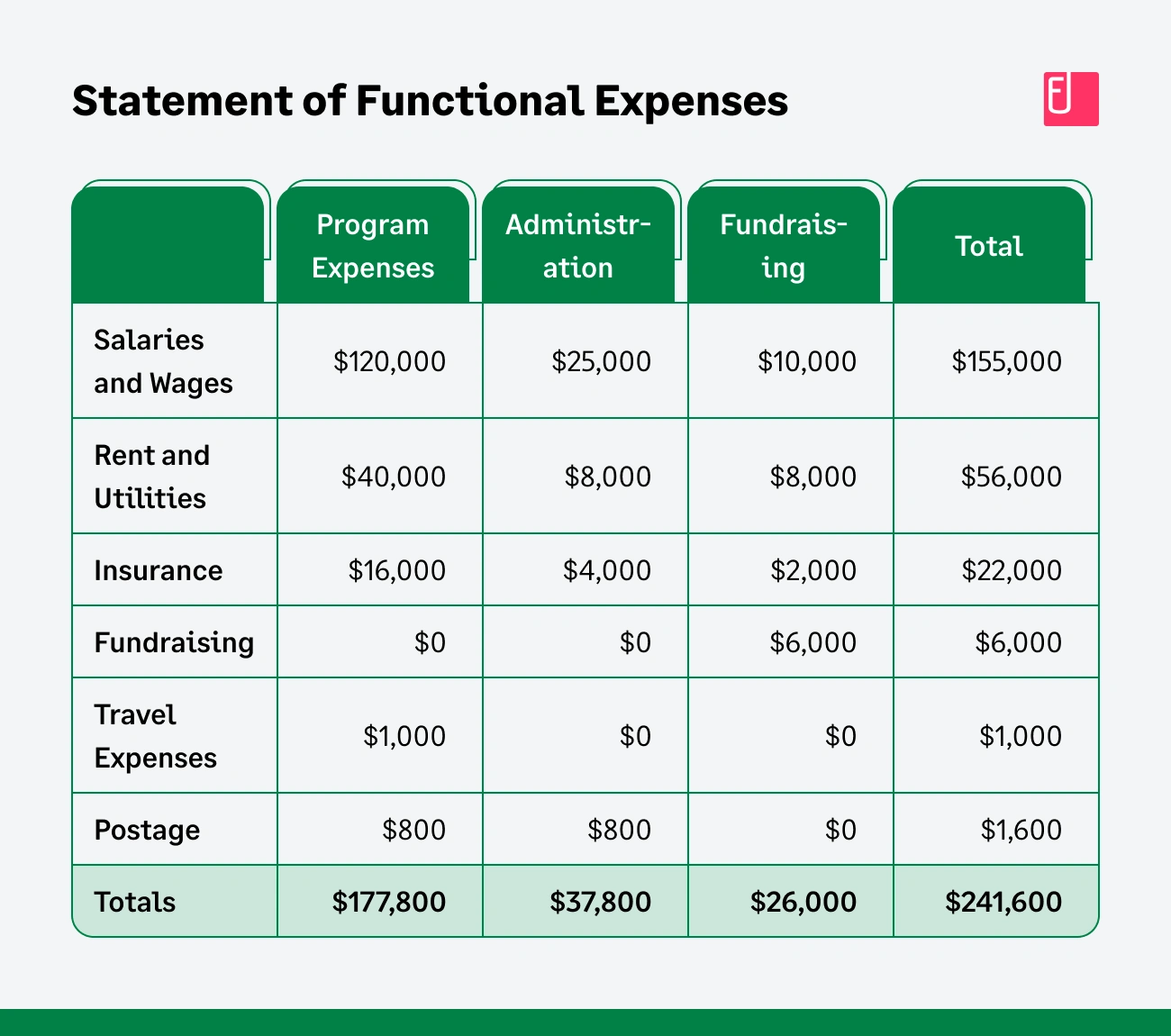

3. Statement of Functional Expenses

A statement of functional expenses in nonprofit accounting is a financial statement that shows an itemized list of expenses according to their purpose. It provides detailed information on where resources have been allocated within the organization.

Typical categories in a statement of functional expenses include:

- Program services

- Management and general

- Fundraising

- Other sources of income

This statement is commonly used to assess the usage of funds, track the efficiency of operations, and make decisions regarding the future.

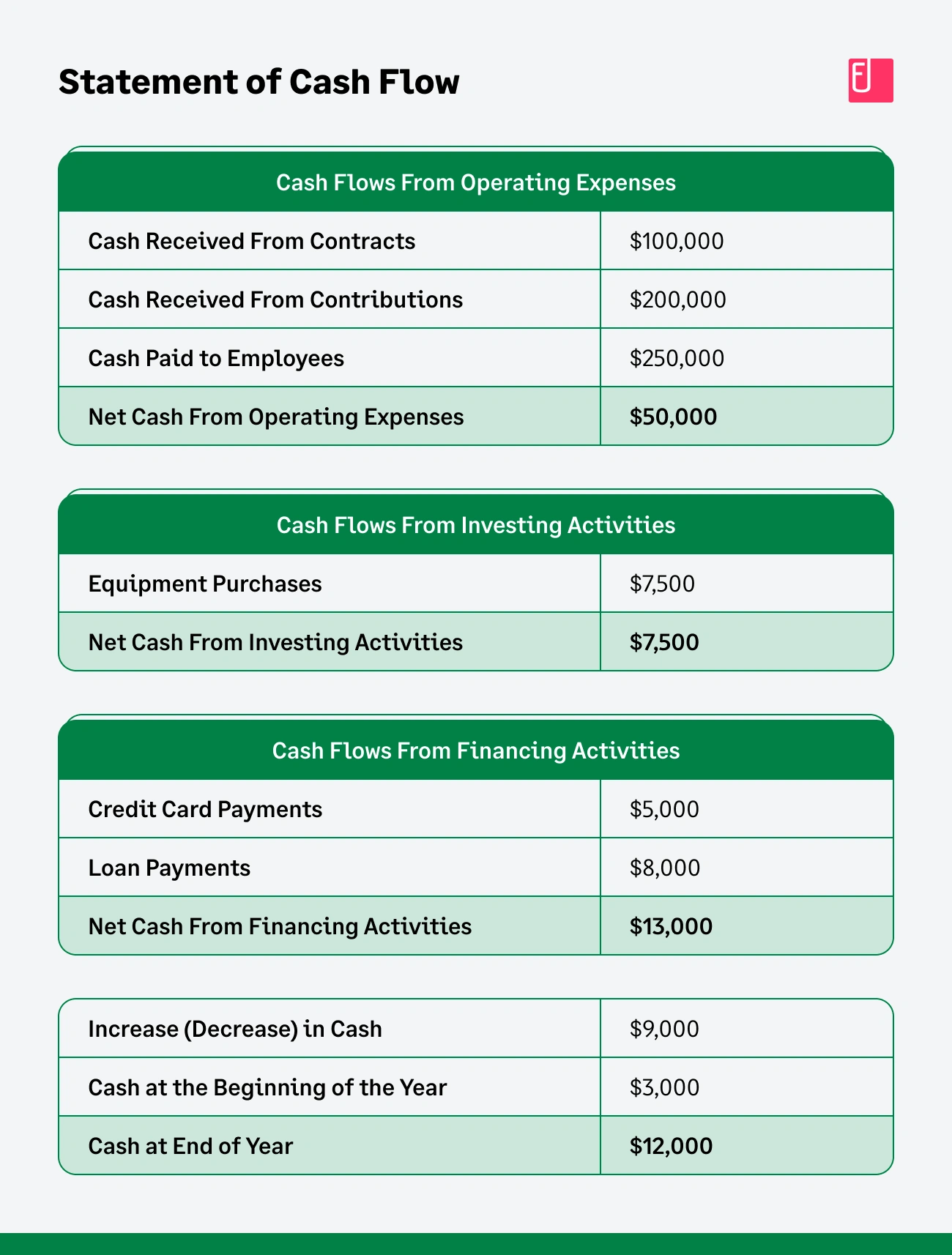

4. Cash Flow Statement

A cash flow statement for a non-profit organization is a financial report that summarizes the inflow and the outflow of cash during a specific period. It provides insights into the organization's ability to generate money from its operations and how it manages its cash resources.

The statement is divided into three sections:

- Operating activities: cash inflows and outflows from operational activities (donations, grants, employee salaries, supplies, administrative grants, etc)

- Investing activities: Cash inflows and outflows from investments

- Financing activities: Cash inflows and outflows from financing sources (loan payments and repayments)

Nonprofit Accounting Compliance Requirements

IRS Form 990

What is the Purpose of IRS Form 990?

Each year, a nonprofit organization must submit Form 990 to the IRS. This document contains information about your nonprofit's annual revenue and expenses. You must track invoices, receipts, and bank statements throughout the year to accurately report all income and expenses.

"Tax filings require the breakdown of funds used by the program, so accounting systems (charts of accounts) must be designed to effectively provide reports for managers to keep close track of funds used, and for tax reporting purposes," CPA Dan Puhl said.

Form 990 is the only federally required annual statement for nonprofits. However, the laws governing nonprofit organizations can vary from state to state. Other financial statements may be required in your state.

Also, remember that your annual tax form, while publicly accessible, doesn't go directly to donors or stakeholders. Creating a comprehensive yearly report is a way to thank donors, engage with your stakeholders, and provide transparency.

Form 990 Breakdown and Filing Requirements

The IRS Form 990 is a comprehensive annual reporting form that most federally tax-exempt organizations must file. It provides the IRS and the public with information about the organization's mission, programs, and finances.

Here’s a breakdown of the key sections:

- Part I: Summary - Provides a snapshot of the organization’s mission, significant activities, and key financial data.

- Part II: Signature Block - Requires the signature of an officer, under penalty of perjury, confirming that the form is accurate.

- Part III: Statement of Program Service Accomplishments - Details the organization's accomplishments for the year and how they relate to its mission.

- Part IV: Checklist of Required Schedules - Determines which additional schedules the nonprofit must complete.

- Part V: Statements Regarding Other IRS Filings and Tax Compliance - Ensures compliance with various other IRS filing requirements.

- Part VI: Governance, Management, and Disclosure - Focuses on the organization's governance structure, policies, and practices.

- Part VII: Compensation of Officers, Directors, Trustees, Key Employees, Highest Compensated Employees, and Independent Contractors - Requires detailed reporting on compensation.

- Part VIII: Statement of Revenue - Breaks down the organization’s income sources.

- Part IX: Statement of Functional Expenses - Categorizes expenses by function (e.g., program services, management, and general fundraising).

- Part X: Balance Sheet - A snapshot of the organization’s assets, liabilities, and net assets.

- Part XI: Reconciliation of Net Assets - Reconciles the organization's financial activities with changes in net assets.

State Reporting Requirements

Each non-profit organization is expected to comply with their state’s reporting requirements. To ensure that it stays in good standing, a nonprofit must meet all its state's informational, reporting, and filing requirements. Failure to comply with these requirements can result in penalties and, worse, the loss of a nonprofit status.

Nonprofit organizations must provide the state with a copy of the IRS Form 990 or an equivalent. For instance, States like Virginia and North Carolina accept audited financial statements. At the same time, North Dakota requires an annual report, so it's best to check your state's requirements to ensure what’s needed.

Is Form 990 Required to be Publicly Disclosed?

Yes, the entire completed Form 990, excluding certain contributor information on Schedule B, must be made available to the public. This is a requirement both from the IRS and potentially from state governments to satisfy state-specific reporting obligations.

Who Must File Form 990?

Organizations exempt from income tax under section 501(a) must file Form 990 if they meet either of the following thresholds:

- Gross Receipts: Equal to or greater than $200,000.

- Total Assets: Equal to or greater than $500,000 at the end of the tax year.

This includes organizations described in section 501(c)(3) (except private foundations) and others under different subsections of 501(c).

What if an Organization's Receipts Are Below the Threshold?

If an organization’s gross receipts are usually $50,000 or less, it can submit Form 990-N, a simpler “e-postcard” version, instead of Form 990 or 990-EZ. Organizations with gross receipts under $200,000 and total assets under $500,000 at the end of the tax year can opt to file Form 990-EZ, a shorter form.

Are There Organizations Exempt from Filing Form 990?

Certain organizations are not required to file Form 990 or 990-EZ, even if they meet the gross receipts or asset thresholds. These include:

- Certain Religious Organizations: Churches, church-affiliated schools, and mission societies primarily operating abroad.

- Certain Governmental Organizations: State institutions and government units.

- Certain Political Organizations: Local political party committees and caucuses of state or local officials.

- Organizations with Limited Gross Receipts: Organizations with gross receipts normally $50,000 or less.

However, some of these organizations may still be required to file Form 990-N.

What Happens if an Organization Fails to File Form 990?

Failure to file Form 990 on time can result in significant penalties. The organization may be charged $20 per day, up to a maximum of $12,000 or 5% of gross receipts, whichever is less. For larger organizations with gross receipts exceeding $1,208,500, the penalty increases to $120 per day, with a maximum penalty of $60,000.

For a more detailed breakdown, go through Instructions for Form 990 Return of Organization Exempt.

What is Unrelated Business Income (UBI)?

UBI is income from a trade or business that is regularly carried on by a tax-exempt organization but is not substantially related to the performance of its tax-exempt purpose. For example, if a museum (a tax-exempt organization) runs a gift shop, the income from the gift shop sales is UBI. A nonprofit must pay taxes on UBI, just as a for-profit business would.

What is the Difference Between a Public Charity and a Private Foundation?

The IRS makes a clear distinction between a public charity and a private foundation. A public charity receives support from a broad base of donors. A private foundation, however, typically receives funding from a single source, family, or corporation. Because of their concentrated funding, private foundations are subject to stricter rules and additional taxes on investment income.

Nonprofit Accounting Best Practices

To ensure your accountants make informed financial decisions, they should understand some basic accounting principles. Below are some of the best nonprofit accounting practices accountants can follow to handle their finances better.

1. Remember: Nonprofits Have Overhead

While there are differing public opinions on this, it’s essential to remember that nonprofit organizations operate similarly to for-profit businesses. Overhead expenses include anything nonprofits use to cover their internal expenses, administrative costs, and marketing their mission for fundraising–activities that help the nonprofit organization grow.

In a nutshell, overhead expenses are the costs that nonprofits incur for anything not directly related to their mission.

It also becomes more accessible to qualify and maintain the status of a nonprofit with the IRS by monitoring overhead. For instance, the IRS requires every nonprofit to maintain a certain percentage of revenue spent on programs.

2. Check In With the Budget Regularly

Check in with your budget regularly, preferably bi-weekly or monthly, comparing your budgeted revenue and expenses against your actual income and expenses. This will ensure that your organization is on track to achieve its goals.

Additionally, checking in with your budget one or more times a month will enable you to adapt to change more quickly. For instance, projects can be discontinued, and funding could fall through or increase. Still, with regular check-ins, you’d be able to address these issues and adapt your strategy accordingly.

3. Implement Checks and Balances Internally

A system of checks and balances in nonprofit accounting is crucial for safeguarding financial resources and ensuring transparency. Here are key steps to establish such a system:

- Segregate Duties: Assign different financial tasks to different individuals to prevent one person from having complete control over any critical process.

- Implement Dual Control: Require two or more individuals to approve and execute sensitive transactions, such as check-writing or bank reconciliations.

- Conduct Independent Reviews: Engage external auditors or internal review committees to assess financial records and procedures periodically.

- Reconcile Accounts Regularly: Compare bank statements, donor records, and other financial accounts to ensure accuracy and identify discrepancies.

- Implement Expense Authorization Policies: Establish clear guidelines for expense reimbursement and require proper documentation for all expenditures.

4. Audit Finances Regularly

Nonprofit audits ensure sound financial health and accuracy in the organization’s financials. Here are some reasons why it can be crucial to audit your finances regularly:

- Financial Accuracy and Compliance: Audits ensure that financial statements are accurate and compliant with accounting standards and donor regulations.

- Error and Fraud Detection: Audits help identify errors, irregularities, or potential fraud that could harm the organization's financial health.

- Transparency and Accountability: Audits enhance transparency by providing independent verification of the organization's financial activities, fostering trust with donors, grantors, and the public.

- Improved Decision-Making: Audits provide valuable insights into the organization's financial performance, enabling better decision-making and resource allocation.

- Risk Management: Audits identify and assess financial risks, allowing the organization to implement preventive measures and mitigate potential losses.

Regular audits are crucial for safeguarding nonprofit assets, maintaining financial integrity, and upholding the organization's reputation.

How Sage Expense Management(Formerly Fyle) Can Help Nonprofit Accounting

The Sage Expense Management platform is the perfect partner for nonprofit accounting, providing the automation and accuracy needed to simplify financial life. The unique challenges of nonprofit finance—from managing multiple grants to ensuring every donation is meticulously documented—demand a solution that goes beyond basic spreadsheets.

It's designed to streamline these complexities, giving your team back the time and resources needed to focus on what matters most: your mission.

The "Receipt Chase" Stops Here

One of the biggest pain points in any finance department is the constant struggle to get employees to submit receipts. This problem is amplified for nonprofits, where every expense, big or small, must be tied to a specific funding source for compliance.

Our platform solves this by automating receipt collection at the source. Employees receive a real-time text notification after swiping their card. They can reply with a picture of the receipt via text, eliminating the need to manually track paper slips and freeing up finance teams from the endless "receipt chase".

Gain Unparalleled Visibility and Control

A lack of real-time visibility into spending is a common complaint among financial controllers. Without it, you can’t know if you're on track with your budget or if a project is overspending until weeks after the fact.

The Sage Expense Management CoPilot feature provides a live dashboard that offers an instant and clear overview of all company-wide spending. This visibility enables you to track expenses across various projects or grant funds, allowing you to make more informed, proactive decisions that ensure your funds are always utilized as intended.

Audit-Ready Records and Flawless Compliance

Nonprofits face intense scrutiny from donors, boards, and regulatory bodies like the IRS. A strong audit trail is non-negotiable.

Our platform helps you create this by ensuring every expense is a secure, unalterable digital record with the receipt and all required documentation securely attached. This provides peace of mind and saves countless hours during an audit, as all your financial data is centralized, searchable, and always ready for review.

This is crucial for demonstrating that you have met your compliance and record-keeping obligations.

Eliminate Manual Reconciliation and Data Entry

The manual reconciliation of credit card statements and re-entering expense data into your accounting software is a significant time drain.

We seamlessly integrate with popular accounting software like Sage, Sage 300, QuickBooks, and Xero eliminate this manual effort entirely. Once an expense report is approved, it’s automatically and instantly synced to your accounting software, ensuring your general ledger is always up-to-date with accurate, clean data.

This enables your finance team to allocate more time to high-value, strategic work and less to tedious data entry.

FAQs around Non-Profit Accounting

How Is Nonprofit Bookkeeping Different?

Nonprofit bookkeeping refers strictly to the process of recording and tracking financial transactions. This is a lower-level position and carries no decision-making responsibilities.

To become a bookkeeper, knowledge of basic financial accounting and experience with financial software, such as QuickBooks, are required. Then, you'll receive much on-the-job training for your specific tasks.

In contrast, accounting requires an advanced knowledge of the organization's goals and structure. An accountant will have decision-making responsibilities and perform financial analysis, making financial projections, recommending financing options, and evaluating internal controls. A nonprofit accountant may do all the above – including bookkeeping – depending on the organization's size.

"While there is only one type of bookkeeper, there are many types of accountants," Mackin said. "Accountants may specialize in an industry, such as manufacturing, or a field, such as taxation or auditing. Bookkeeping refers strictly to recording the organization's daily transactions and creating some reports."

Also Read:

What are "Quid Pro Quo" Contributions?

A quid pro quo contribution is a donation where a donor receives goods or services in exchange for their contribution. The donor’s tax deduction is limited to the amount of the contribution that exceeds the fair market value of the goods or services received. For any single payment over $75, the nonprofit must provide a written disclosure statement to the donor, outlining the fair market value of what they received.

How are Non-Cash Donations, like Vehicles, Handled?

Noncash donations, such as a vehicle, are a special type of contribution with strict rules. The deductible amount for the donor is generally limited to the gross proceeds from the sale of the vehicle if the charity sells it. If the charity uses the vehicle for its mission, the donor may be able to deduct the fair market value. The nonprofit must provide a written acknowledgment to the donor and may be required to file Form 1098-C.

What Skills Are Required For Nonprofit Accounting?

A bachelor's degree in accounting is the standard to become a nonprofit accountant. Most university accounting programs offer a nonprofit accounting course combined with government accounting. Although not required, additional education is usually required if you want a CPA license or other certification, such as a Certified Management Accountant (CMA) or Certified Fraud Examiner (CFE).

In addition to solid GAAP accounting skills, you'll need an understanding that money coming into the organization is generally difficult to obtain, so it must be spent wisely. That means not only must you understand the nuances of nonprofit accounting vs. net-income-focused accounting, but you must be able to employ solid management accounting practices across the board.

"In my experience with nonprofits, most executives are not experienced with accounting fundamentals and the use of accounting information, so accountants must be counselors and teachers. Soft skills, to be a non-threatening partner, are essential," Puhl said.

How Much Do Accountants in Nonprofit Organizations Typically Earn?

On average, nonprofit accountants earn around $61,000 annually. However, this figure can fluctuate significantly based on which state they work in. (Source: ZipRecruiter)

States with the Highest Salaries for Non-Profit Accountants

- Alaska tops the list, with nonprofit accountants earning an average of $71,844 annually ($34.54 per hour).

- Oregon follows closely, where accountants earn around $71,797 annually ($34.52 per hour).

- North Dakota is another state where nonprofit accountants are well-compensated, with an average salary of $71,532 annually ($34.39 per hour).

States with the Lowest Salaries for Non-Profit Accountants

- At the lower end of the spectrum, Florida has the lowest average annual salary for nonprofit accountants, at $44,880($21.58 per hour).

- West Virginia also ranks low, with an average salary of $46,671 annually ($22.44 per hour).

- Louisiana and Georgia are also among the states where nonprofit accountants earn less, with average annual salaries of $50,682 and $50,712, respectively.

Some interesting insights

- States like California and New York, known for their high cost of living, surprisingly fall into the middle range, with average salaries of $60,803 and $65,963, respectively.

- Washington and Massachusetts, with higher living costs, offer competitive salaries of $70,360 and $71,431, respectively, reflecting the demand for skilled nonprofit accountants in these states.

What Financial Statements Must A Nonprofit Organization Prepare Annually?

Nonprofit organizations must prepare four core financial statements annually–the statement of financial position, statement of activities, statement of cash flow, and statement of functional expenses.

In Conclusion

If you’re a nonprofit seeking to streamline your finances and optimize resource allocation, consider exploring expense management software like Sage Expense Management, which automates expense reporting and provides real-time spending insights, thereby enhancing efficiency and transparency to ensure every dollar has a positive impact.