.webp)

Reimbursement is more than a administrative task; it is the bridge between an employee’s out-of-pocket spending and the company’s financial health. When handled correctly, it ensures that people aren't acting as zero-interest lenders for their employers while keeping the business safe from the scrutiny of an audit.

In this guide, we walk through the mechanics of travel expense reimbursement, the strict boundaries set by the IRS, and how moving away from the "shoebox of fading receipts" can protect your bottom line.

What Is Travel Expense Reimbursement?

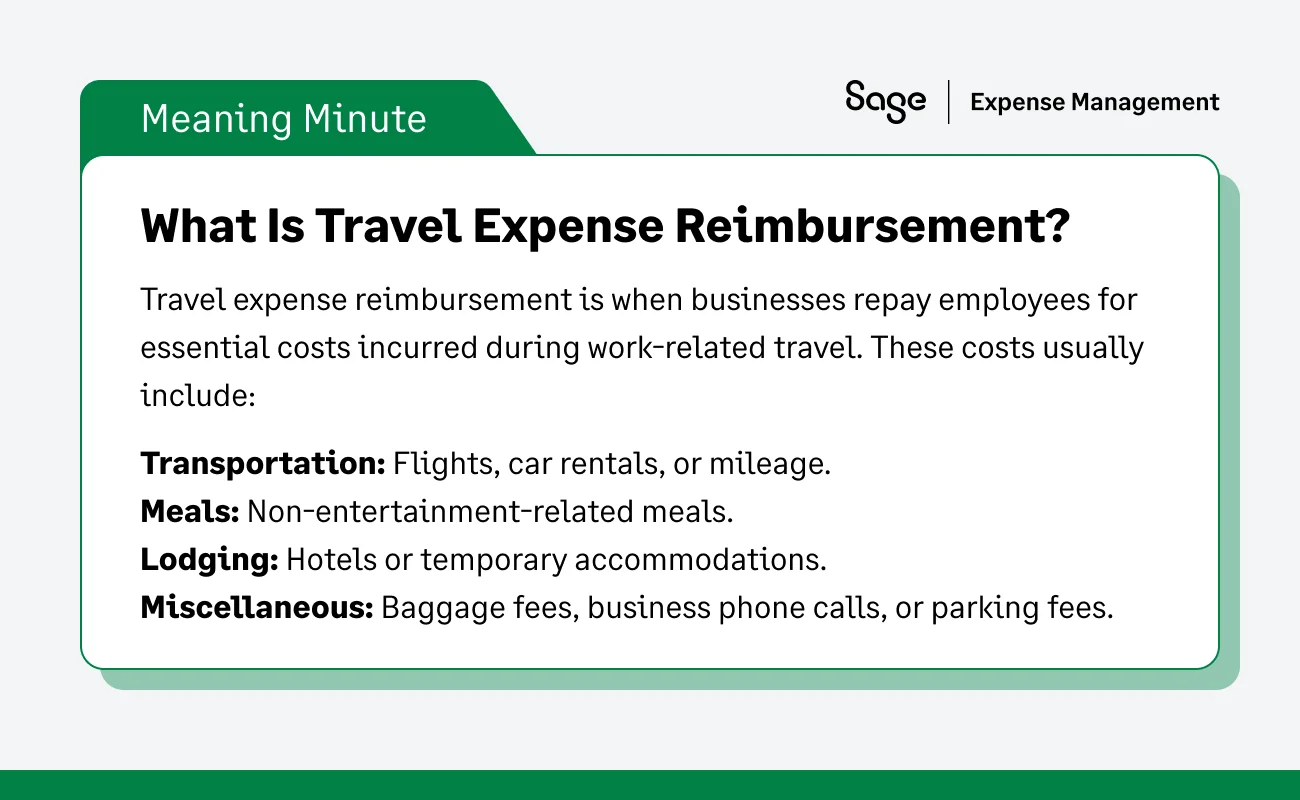

Travel expense reimbursement is the process of compensating employees for reasonable and necessary costs incurred while traveling away from home for work. This typically covers transportation, lodging, and meals.

A clear policy removes the guesswork for the employee and ensures the finance team isn't left chasing missing data weeks after a trip has ended.

The "Tax Home" Concept

The IRS defines your "tax home" as the entire city or general area where your main place of business or work is located. You are only considered to be "traveling away from home" if you are leaving this area for a period substantially longer than an ordinary day's work and require sleep or rest to meet the demands of your job.

If you live in Dallas but work in Houston, Houston is your tax home. This means you cannot be reimbursed tax-free for travel between Dallas and Houston, as the IRS views this as a personal commuting expense.

What Travel Expenses Can You Reimburse?

You can reimburse employees for ordinary and necessary expenses incurred while away from home on business.

- Transportation: This includes airfare, train, or bus tickets between your home and the business destination.

- Lodging: Overnight stays are reimbursable, though companies typically set caps based on the destination's cost of living.

- Meals: These are reimbursable if the trip requires a "sleep or rest" period.

- Local transportation: This covers taxis, rideshares, or rental cars used to get between the hotel and the business site.

- Miscellaneous expenses: Necessary costs like baggage fees, laundry on trips lasting more than a few days, and business-related phone calls.

Example Scenario

If an employee drives from Dallas to a conference in Houston and stays overnight, they incur $60 in gas, $150 for lodging, and $40 on meals. The company reimburses the $150 hotel and uses the IRS standard mileage rate for the drive (rather than just gas) to ensure the employee is covered for vehicle wear and tear. Since meals are generally subject to a 50% deduction limit for the business, the company tracks this carefully for tax filing.

IRS Rules Around Travel Reimbursements

The IRS guidelines are designed to distinguish between legitimate business support and "disguised" taxable income.

Following these rules not only helps businesses stay compliant, but also prevents issues during audits, and ensures employees are reimbursed for legitimate business expenses.

Here’s a closer look at the key IRS rules businesses should follow:

Actual Cost vs Standard Meal Allowance

Employees can claim the actual cost of every meal, but this requires keeping every single physical receipt. For a frequent traveler, this often leads to the "shoebox problem"—where paper receipts are lost or become unreadable before they can be processed.

Standard Meal Allowance Method

The IRS offers a simplified "per diem" approach. Instead of tracking every coffee and sandwich, employees claim a set daily amount for meals and incidental expenses (M&IE).

- Standard rate: For 2026, the standard meal allowance is $68 per day for most U.S. locations.

- Who can use it: Both employees and self-employed individuals can use this to simplify their recordkeeping.

- Benefits: It eliminates the need to collect small meal receipts and provides a predictable cost for the finance team.

High-Low Substantiation

To make per diems even easier, the IRS provides a "High-Low" method. This allows businesses to use one rate for "high-cost" localities (like NYC or San Francisco) and a lower rate for everywhere else. This prevents the need to look up a different GSA rate for every single city an employee visits.

Travel Inside vs Outside the U.S.

The rules change once an employee crosses an international border.

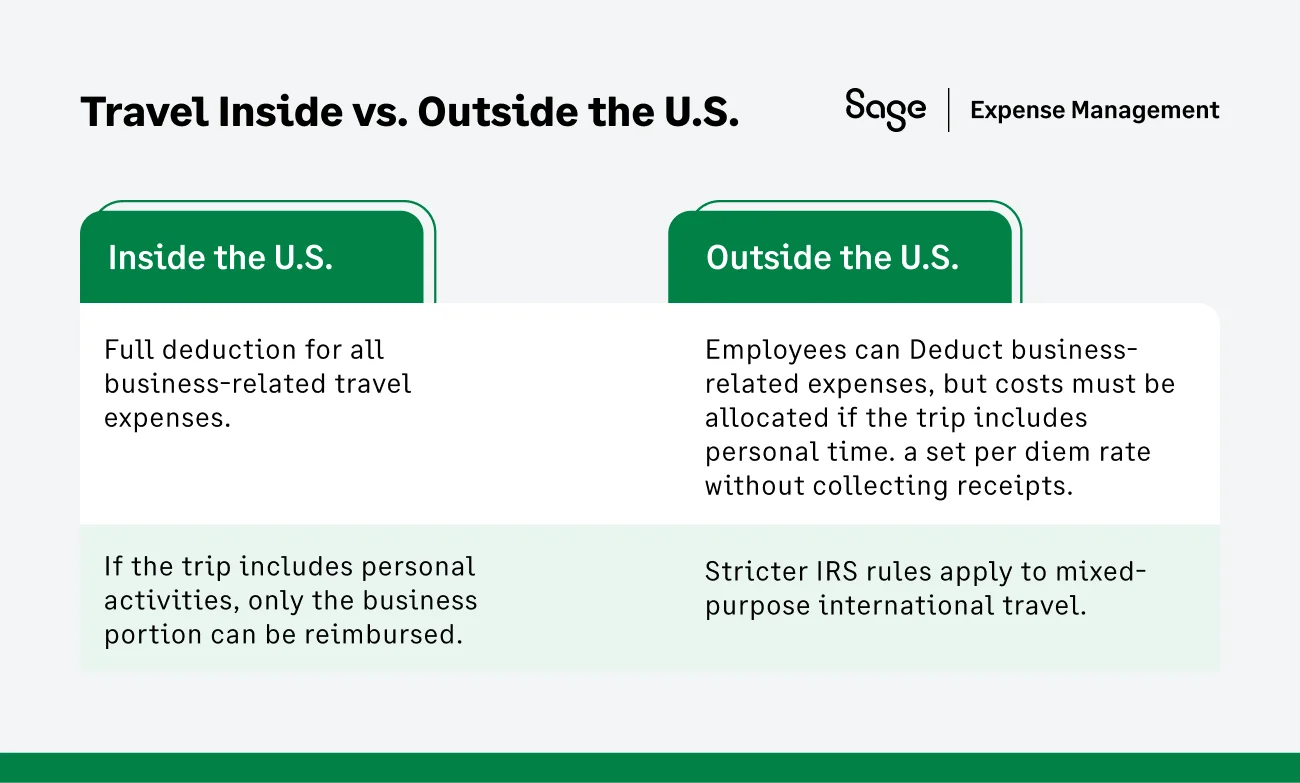

Rules for Travel Inside the U.S.

If the trip is entirely for business, all transportation costs are deductible. If the trip is primarily for vacation but includes some business, none of the transportation costs are deductible—only the specific expenses related to the business activities.

Personal Activities During Business Travel

If an employee combines business travel with personal activities (e.g., a vacation), only the expenses related to business can be reimbursed. Personal expenses, such as sightseeing tours or meals during non-business days, are not deductible.

Example: An employee travels to Los Angeles for a 5-day business conference but decides to stay an extra 3 days for personal vacation. The company can only reimburse travel, lodging, and meal expenses for the 5 business days. The costs incurred during the 3 vacation days are personal and not reimbursable.

Multi-Purpose Trips

If the purpose of the trip is primarily personal, with only a minor business component, the trip’s travel expenses cannot be reimbursed as business-related costs.

Rules for Travel Outside the U.S.

International rules are stricter. If the trip is for more than a week and at least 25% of the time is spent on non-business activities, you must allocate your travel expenses between business and personal time. If you spend 4 days on business and 4 days on vacation in London, only 50% of your airfare is deductible.

Primary Purpose of Travel

If the primary purpose of the trip is business, the cost of getting to and from the destination is fully deductible. If the trip is mainly for personal purposes, even if some business activities are conducted, travel expenses are not deductible.

Allocation of Costs

For mixed-purpose trips, businesses need to allocate costs between business-related and personal expenses. Only the portion related to business can be reimbursed or deducted.

Example: An employee flies to London for a week-long business meeting but spends 3 extra days vacationing in Paris. The cost of the airfare to and from London can be deducted, but the cost of traveling to and staying in Paris is personal and not reimbursable.

Conventions and Business Meetings

Expenses related to attending business-related conventions or meetings can be reimbursed. However, certain conditions apply:

Establishing a Business Purpose

The convention must directly relate to the employee’s job or the business’s operations. For instance, attending an industry-specific conference that offers skill development or business insights would qualify.

Rules for Family Members

If an employee brings a family member (such as a spouse or child), their travel expenses are not deductible unless the family member is also an employee with a bona fide business purpose for attending.

Example: If an employee travels to a technology conference in New York and brings their spouse, the company can reimburse the employee’s flight and hotel costs, but the spouse’s expenses (e.g., additional airfare and meals) are not reimbursable unless the spouse has a legitimate business role in the trip.

Meals and Entertainment

The IRS has specific rules on the deductibility of meals and entertainment expenses. Changes in recent years have tightened the ability to deduct entertainment-related costs.

Meals

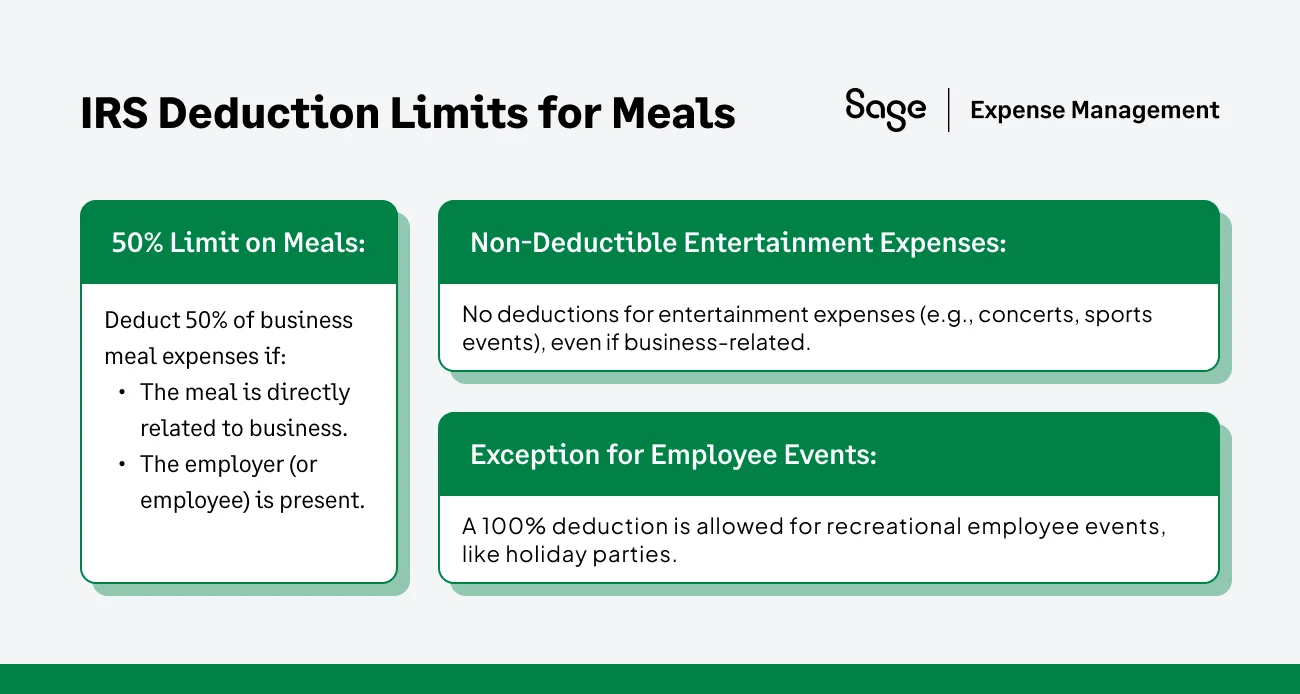

Businesses can deduct 50% of the cost of meals, provided they meet the following conditions:

- The meal is directly related to business or associated with a business activity.

- The meal is not lavish or extravagant under the circumstances.

- The employer (or their employee) is present during the meal.

Example: If an employee takes a client out for lunch during a business meeting, the company can deduct 50% of the meal cost.

Entertainment

Since 2018, the IRS has disallowed deductions for most entertainment expenses. This includes costs associated with attending concerts, sporting events, or other recreational activities.

However, businesses can still deduct 50% of the cost of meals provided at such events as long as they meet the IRS criteria for a business meal.

Exceptions to the Entertainment Rule

Some specific types of entertainment-related expenses are still deductible, including:

- Entertainment treated as compensation: If the company treats entertainment as employee compensation (e.g., company-provided tickets to a sporting event that are included in an employee’s taxable wages), these expenses may still be deductible.

- Employee events: Recreational expenses for employee-only events, such as holiday parties or company picnics, are fully deductible.

Record-keeping and Documentation

The IRS requires businesses to maintain adequate records of travel-related expenses. Proper documentation ensures compliance with IRS rules and helps businesses defend their deductions during audits.

Receipts

For expenses over $75, businesses must maintain receipts or other documentary evidence (e.g., hotel bills and flight itineraries). However, small expenses (under $75) and certain transportation costs may not require receipts.

Records Must Include

- The amount, date, and place of the expense.

- The business purpose of the expense.

- The name and title of the individuals involved in the business meal or meeting (for meals and entertainment).

For more information, please refer to IRS Publication 463 (2023), Travel, Gift, and Car Expenses

How Can You Create a Travel Reimbursement Policy?

A well-defined travel reimbursement policy clarifies what expenses your company will reimburse and sets clear expectations for employees. This ensures responsible spending and simplifies the reimbursement process. Here’s how to create one:

Define Reimbursable Expenses

Start by specifying which types of expenses are reimbursable. Common categories include:

- Business travel: Clarify what transportation, meals, and lodging costs you will cover. Include limits, like mileage rates or daily allowances for meals.

- Business entertainment: If you reimburse entertainment expenses, such as meals with clients, outline the justification required.

- Other business expenses: List professional development, home office supplies, or other expenses that may be reimbursable, along with any spending limits.

Expense Reporting Procedure

- Method: Specify how employees should submit expense reports (paper forms, spreadsheets, or expense software).

- Documentation: Require valid proof (e.g., receipts) for each expense type.

- Deadlines: Set clear deadlines (e.g., submit reports within 14 days of a trip).

Communication and Enforcement

- Employee education: Ensure employees are aware of the policy through regular training.

- Approval process: Define who can approve expenses based on the amount.

- Consequences: Detail potential penalties for violating the policy, such as non-reimbursement or disciplinary action.

Critical IRS Compliance Questions

Do I Need Receipts to Reimburse an Employee?

Generally, businesses require receipts to substantiate travel expenses. However, there are exceptions:

- Small expenses: Receipts aren’t required for expenses under $75 or for transportation expenses where receipts are not readily available.

- Per Diem allowance: If employees are reimbursed via a per diem (standard daily rate for meals and lodging), they do not need submit receipts for those expenses.

Employees should keep detailed records of expenses, including the date, amount, and purpose of each expenditure, even if receipts are not needed.

Are Travel Reimbursements Taxable?

Most travel reimbursements under an accountable plan are non-taxable. This means that if employees properly account for their expenses and return excess reimbursements, the company does not have to report these amounts as income, and employees do not pay taxes on them.

Under a non-accountable plan, reimbursements are considered taxable income. In this case, the company would include the reimbursement amount on the employee’s W-2, and the employee would pay taxes on it.

Temporary vs. Indefinite Assignments

A "trip" stops being a trip once it lasts too long.

- Temporary: If the assignment is expected to last one year or less, it is considered travel.

- Indefinite: If the assignment is expected to last more than one year, that location becomes the employee's new "tax home." At that point, all reimbursements for lodging and meals become taxable income for the employee.

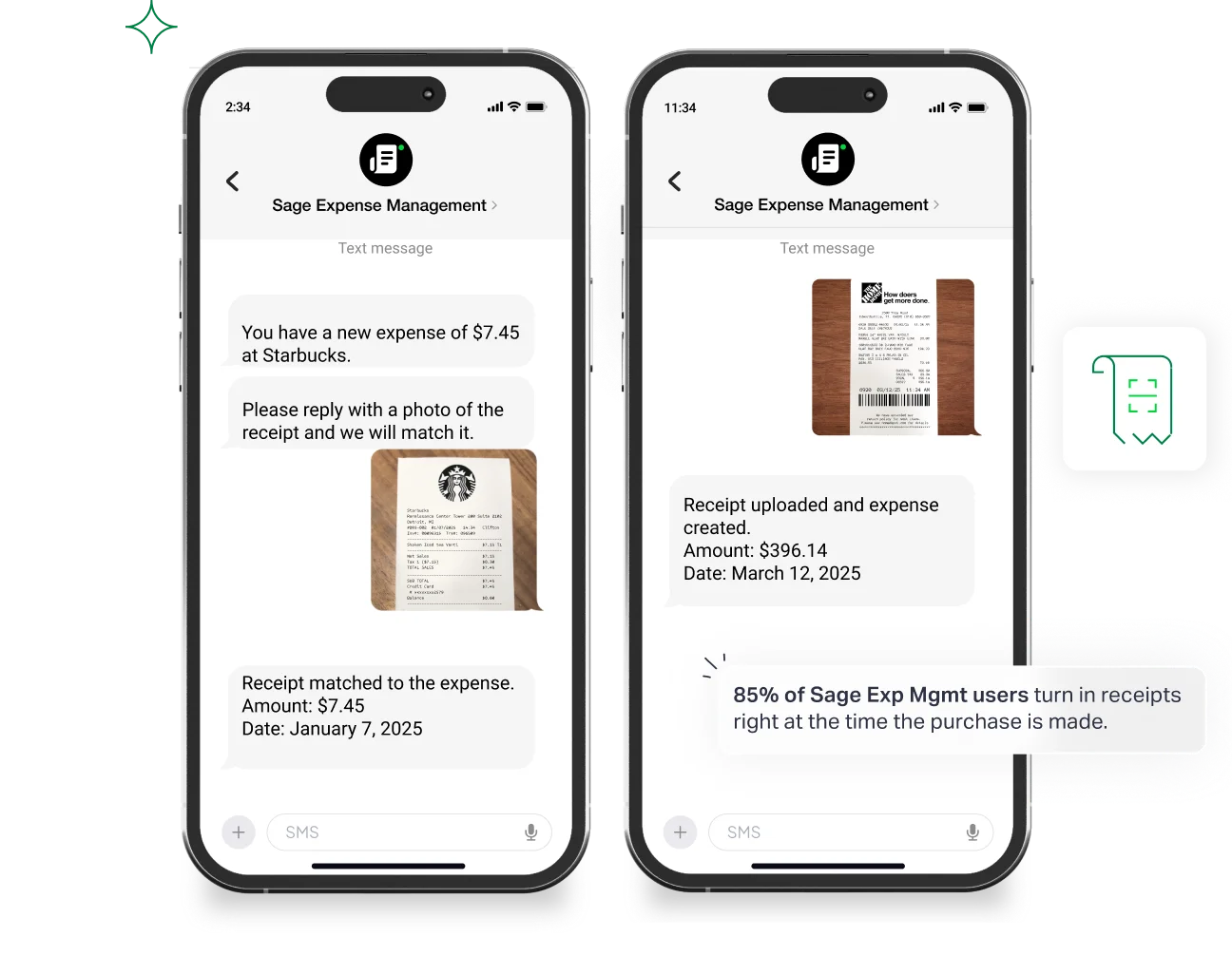

How Sage Expense Management Can Help with Travel Reimbursements

Sage Expense Management provides a powerful solution to simplify and streamline the travel reimbursement process. Here's how:

- Real-Time credit card feeds: Employees are notified instantly when business credit cards are swiped. Receipts can be submitted via text message, making reconciliation automatic and efficient.

- Track receipts: Employees can submit receipts using text message, the mobile app, Gmail/Outlook, or even Slack.

- Mileage and Per Diem tracking: It enables accurate mileage and per diem tracking, accommodating different currencies, employee levels, and locations.

- TravelPerk integration: It integrates seamlessly with TravelPerk to reconcile trip-related expenses and automate travel expense reporting.

- Virtual Cards for Travel: Businesses can issue American Express virtual cards for employee travel expenses, ensuring real-time spending tracking.

- Real-Time compliance: Its system automatically monitors and enforces compliance, ensuring that all expenses meet policy standards before reimbursement.

- Direct Reimbursement via ACH: It supports direct reimbursements via ACH, streamlining payments to employees.

FAQs around Travel Reimbursements

What if an employee loses a receipt for a $100 hotel stay?

The IRS requires documentary evidence for all lodging, regardless of the amount. The employee may need to provide a "Missing Receipt Affidavit" and secondary proof like a bank statement, but the IRS can still disallow the deduction without the original folio.

Can we reimburse for "Bleisure" (Personal days) tax-free?

No. You can only reimburse the business portion tax-free. If an employee stays through the weekend for vacation, the Saturday and Sunday hotel and meals are considered personal and are not reimbursable under an accountable plan.

Is a credit card statement enough to prove a business meal?

No. A credit card statement only proves a transaction occurred. You need an itemized receipt to prove what was purchased (e.g., to show that no non-deductible entertainment or lavish items were included).

Does the "Sleep or Rest" rule apply to a 14-hour day trip?

Generally, no. If you can complete the work and return home without needing a substantial period of sleep or rest, the IRS does not consider you to be "traveling away from home." This means lunch on a day trip is typically not a deductible travel meal.

How do we handle reimbursements for international currency fluctuations?

Automation tools like Sage Expense Management automatically calculate the exchange rate based on the transaction date, ensuring employees are reimbursed accurately without manual math.

{{reimbursement="/cta-banners"}}