The expense recognition principle is a fundamental concept in accounting that ensures expenses are recorded in the same period as the revenue they help to generate. This principle aligns with the accrual basis of accounting, making it essential for accurate financial reporting.

By understanding how to recognize expenses appropriately, businesses can maintain consistency and clarity in their financial statements, which is crucial for decision-making, tax reporting, and stakeholder communication.

Foundational Concepts in Expense Recognition

Before diving into the how we need a shared language for the different ways expenses sit on your balance sheet.

- Matching principle: The core rule requiring expenses to be recorded alongside the revenue they support.

- Accrued expenses (Liabilities): Costs you have incurred but haven't paid for yet, such as a tent rental for a company event where the invoice hasn't arrived.

- Prepaid expenses (Assets): Payments made in advance for services you’ll receive later, like a six-month software maintenance contract.

- Amortization: The process of gradually expensing the cost of an intangible asset, like a software license, over its useful life.

- Depreciation: Allocating the cost of a tangible asset, like a delivery truck, across the years it is actually in service.

- Deferred expenses: Costs incurred now but recognized in later periods to align with future revenue generation.

- IBNR (Incurred But Not Recorded): An estimate used in fields like insurance to account for the time lag between an event occurring and a claim being filed.

What Is the Expense Recognition Principle?

The expense recognition principle, also known as the matching principle, requires that businesses record expenses in the same period as the related revenue. This principle contrasts with the cash basis of accounting, where expenses are only recorded when cash is paid.

By adhering to this principle, companies achieve a clearer picture of their financial health and profitability for each accounting period.

Example: If your team spends $5,000 on a marketing campaign in December that triggers a massive sales spike in January, recognizing that full $5,000 in December makes the month look artificially expensive while January looks artificially profitable. The matching principle fixes this "profit distortion" by ensuring the cost of the sale is recognized when the sale actually happens.

Why is the Expense Recognition Principle Important?

Beyond basic compliance, this principle acts as the "north star" for financial integrity. It is important because:

- Prevents profit distortion: Without it, a business might look incredibly profitable one month (because they didn’t pay bills) and bankrupt the next (when all the bills come due), even if their actual operations were steady.

- Investor confidence: Investors look for a clean matching of costs to revenue to understand the true burn rate and gross margins of a company.

- Tax accuracy: Ensuring expenses are recognized in the correct tax year prevents overpayment or underpayment of taxes, which can lead to costly audits.

- Facilitates better forecasting: When you know exactly what it costs to generate a dollar of revenue in a specific timeframe, your future projections become significantly more reliable.

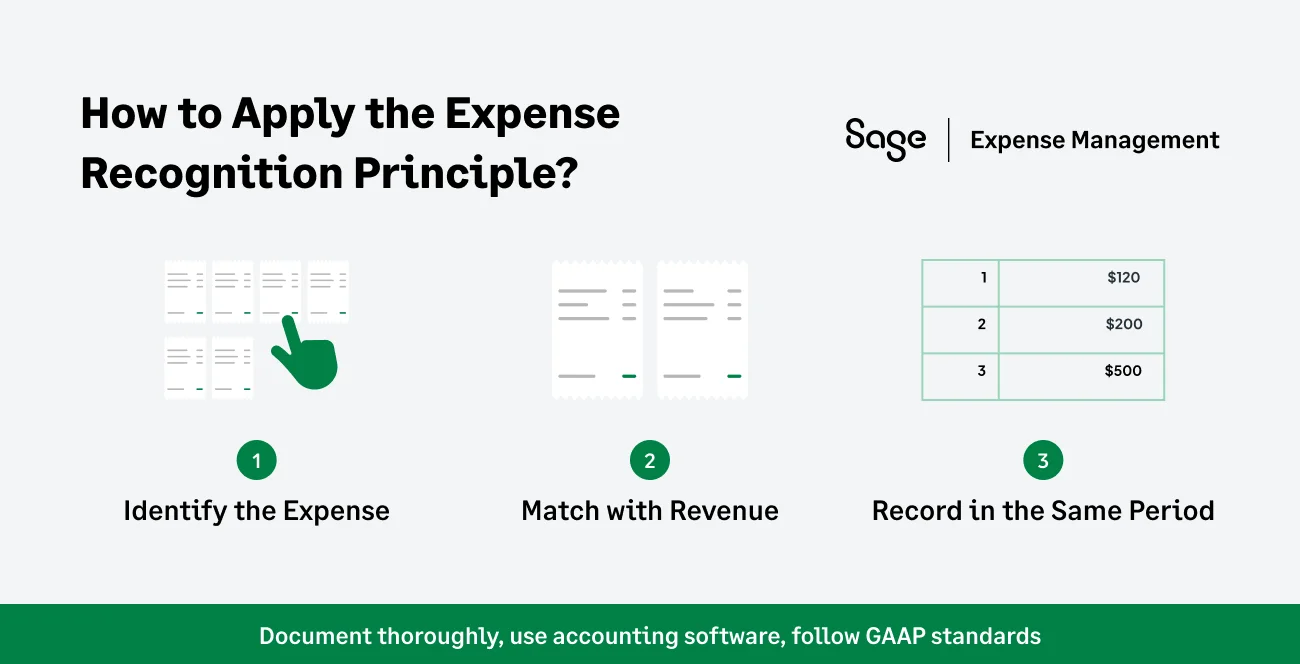

How Does the Expense Recognition Principle Work?

To follow the expense recognition principle, a business should follow a structured workflow:

- Identify the Expense: Understand the cost incurred (e.g., a $10,000 annual software subscription).

- Match with Revenue: Link the expense to the revenue it helped generate (e.g., the software is used for 12 months to serve clients).

- Record in the Same Period: Ensure both are documented within the same timeframe (e.g., recognizing $833.33 per month rather than $10,000 in January).

This method is particularly useful for ensuring accuracy when dealing with long-term expenses, such as depreciation or prepaid expenses.

When Should I Use the Expense Recognition Principle?

The expense recognition principle is essential for any business using accrual accounting and aiming for GAAP compliance. It’s particularly valuable for:

- Transparent Financial Reports: Stakeholders and investors require accurate financial insights to make decisions.

- Precise Financial Analysis: Matching revenue and expenses provides a true view of a business’s profitability.

- Scaling Businesses: As operations grow more complex (e.g., hiring more staff or taking on debt), the cash basis of accounting fails to reflect economic reality.

How the Expense Recognition Principle Helps Accrual Accounting

Accrual accounting relies on the matching principle to present a more accurate financial picture. Instead of only recording when cash changes hands, accrual accounting records when transactions are earned or incurred. This approach provides greater clarity on business performance and cash flow.

Some key points around accrual accounting:

- Aligns revenue and expenses for accurate financial reports.

- Helps businesses manage cash flow better by revealing obligations and income.

- Enables comparison of income and expenses to track profitability.

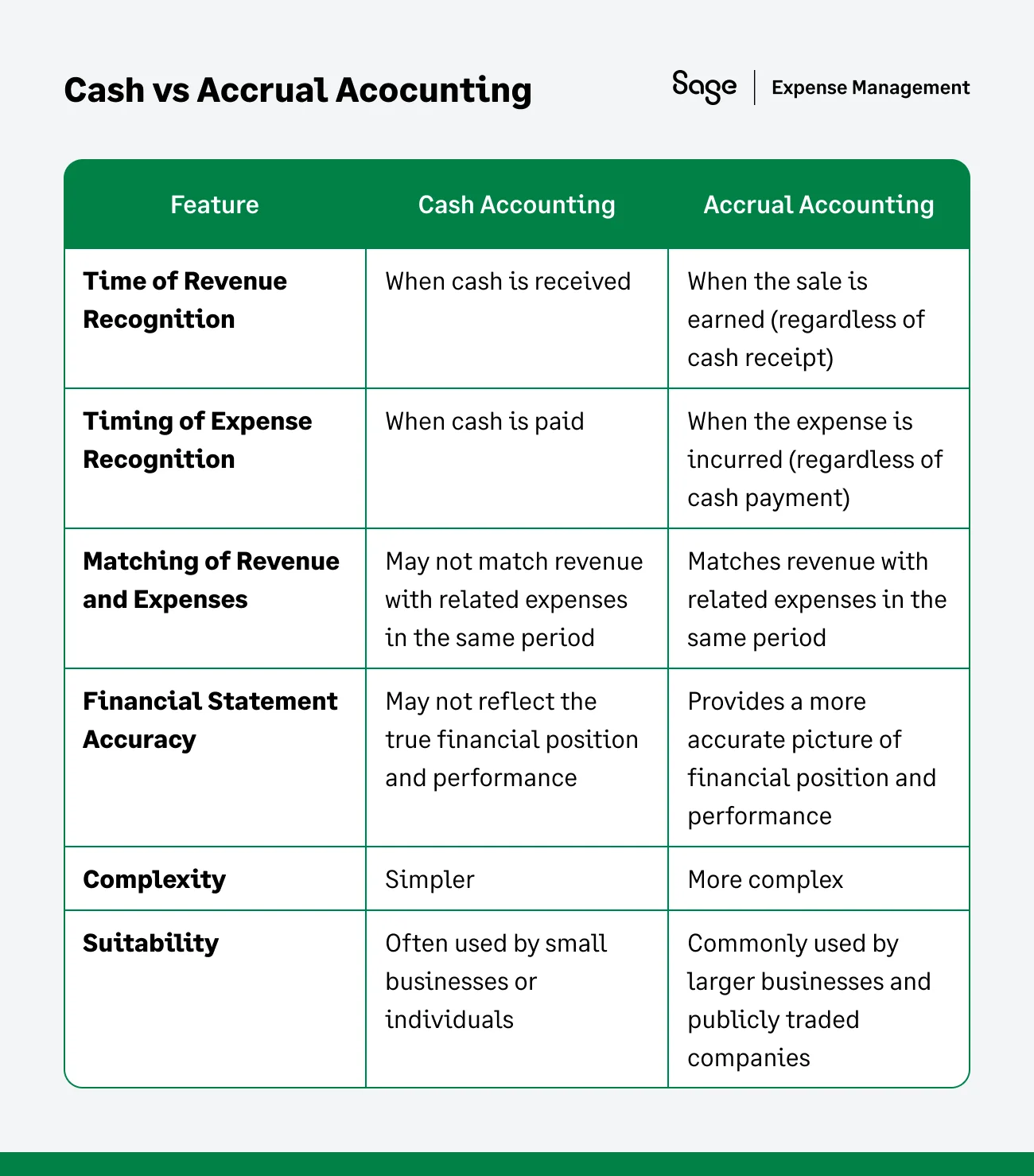

Cash Accounting vs. Accrual Accounting

The two primary accounting methods, cash and accrual, differ in their treatment of income and expenses. Here’s a breakdown:

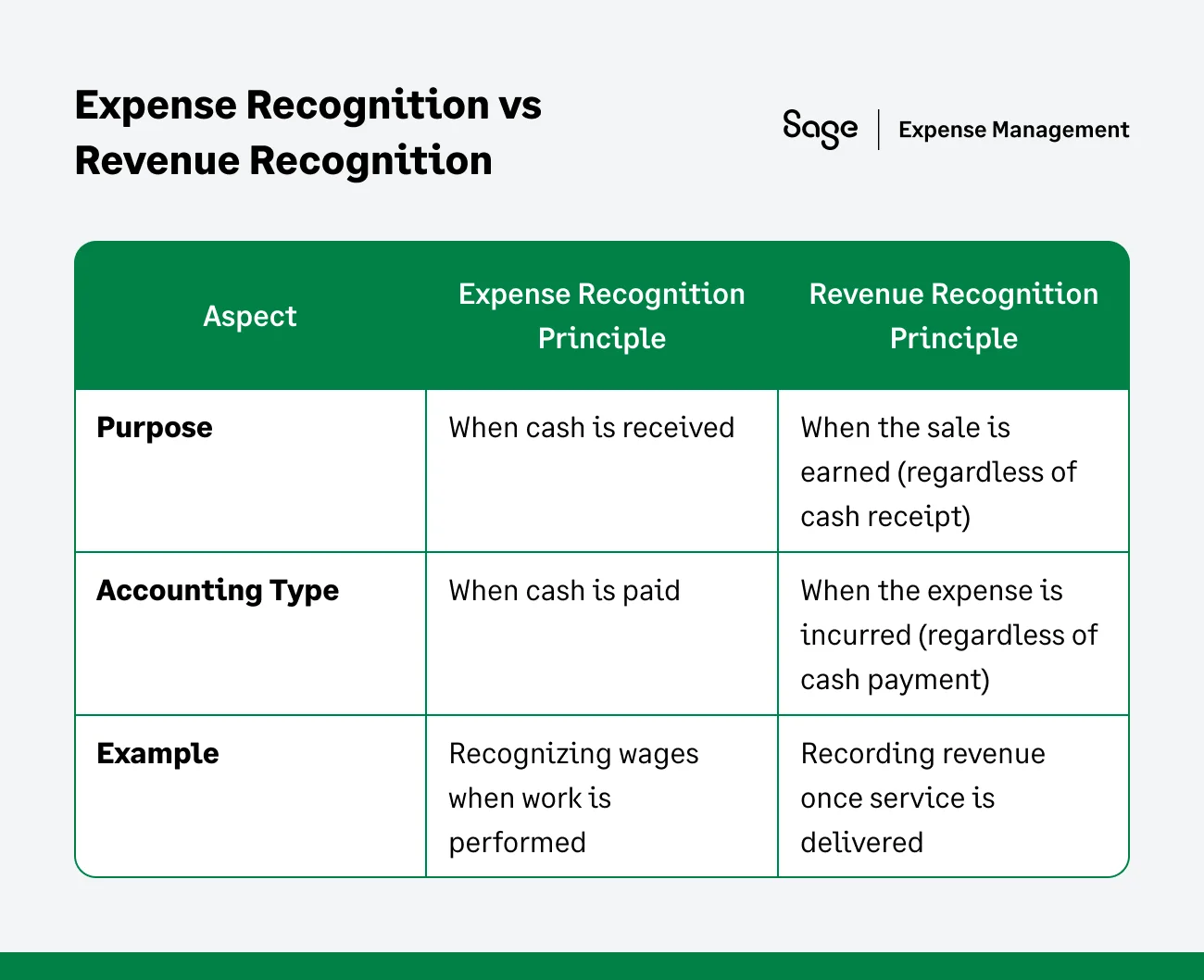

Expense Recognition vs. Revenue Recognition Principle

While the expense recognition principle deals with expenses, the revenue recognition principle governs when to record revenue. Both are essential for accurate financial reporting, as they work together to represent a company’s performance in a given period.

They are two halves of the same whole; for the books to be accurate, the "trigger" that recognizes revenue must also trigger the recognition of the associated expenses.

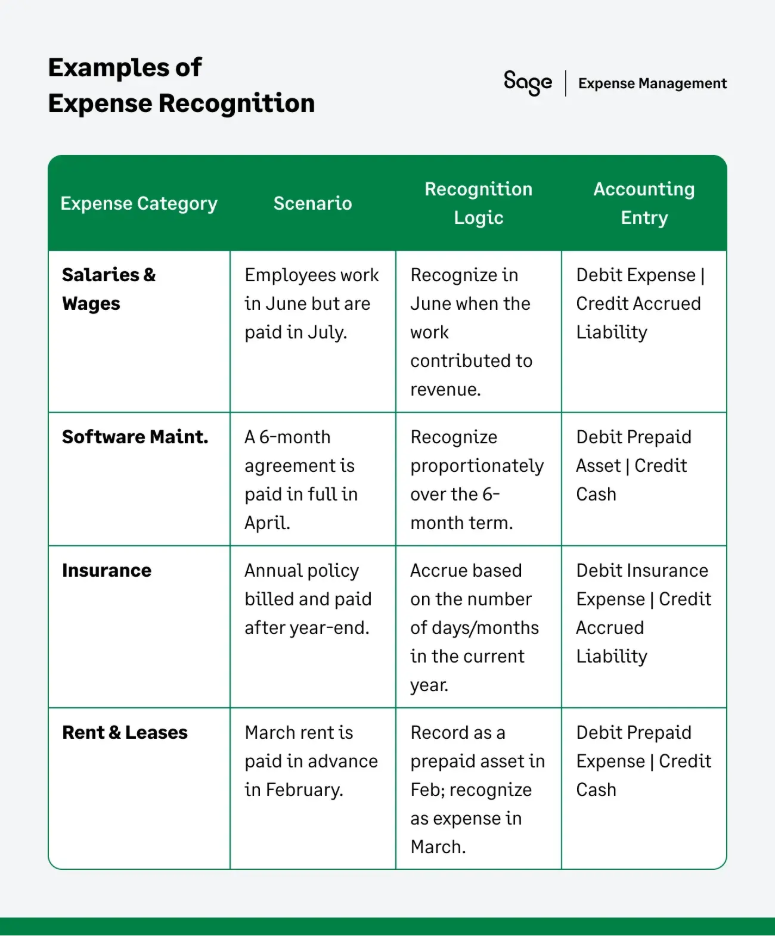

Examples of Expense Recognition

To understand how the expense recognition principle works in practice, let’s look at several expense categories and how they align with revenue:

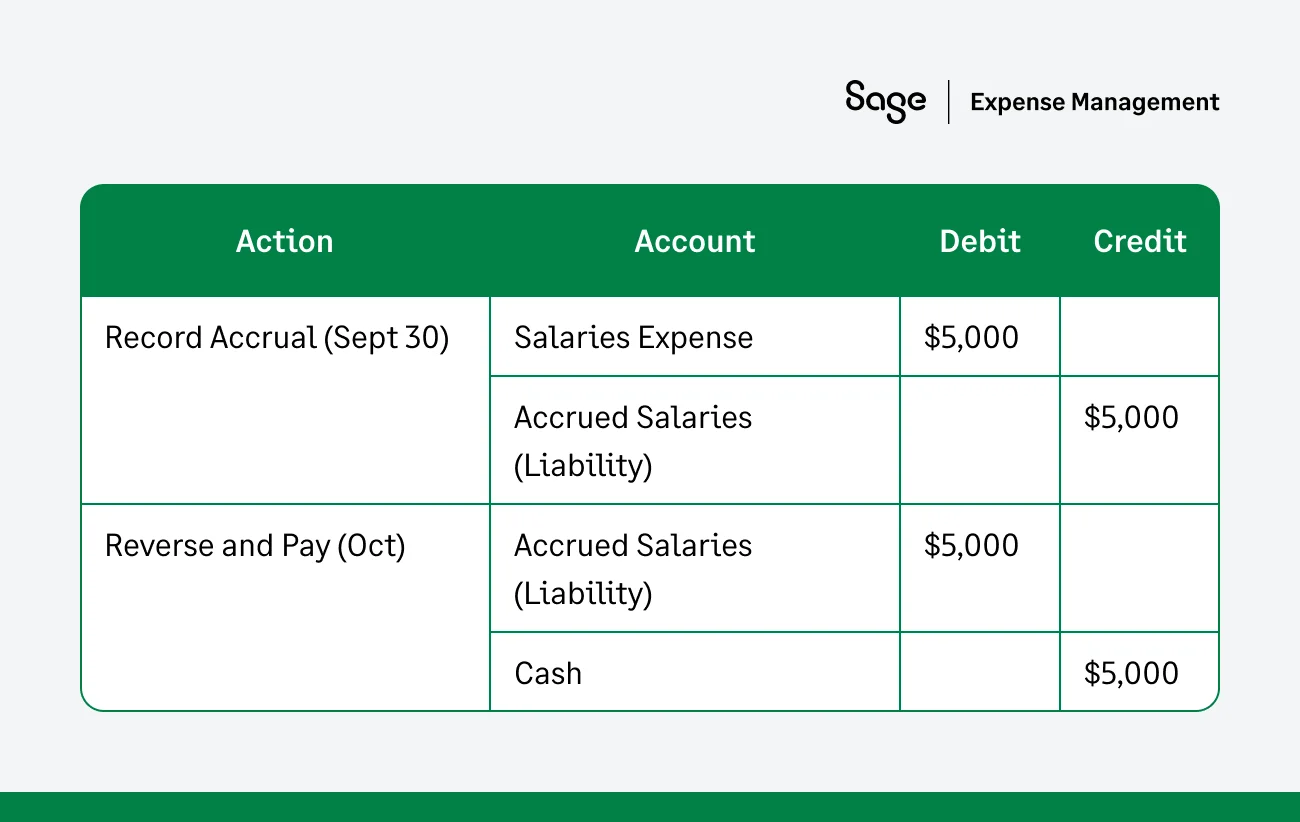

Salaries and Wages

If your team works the last week of September but isn't paid until October, the labor cost must be recorded in September to reflect when the work contributed to your business.

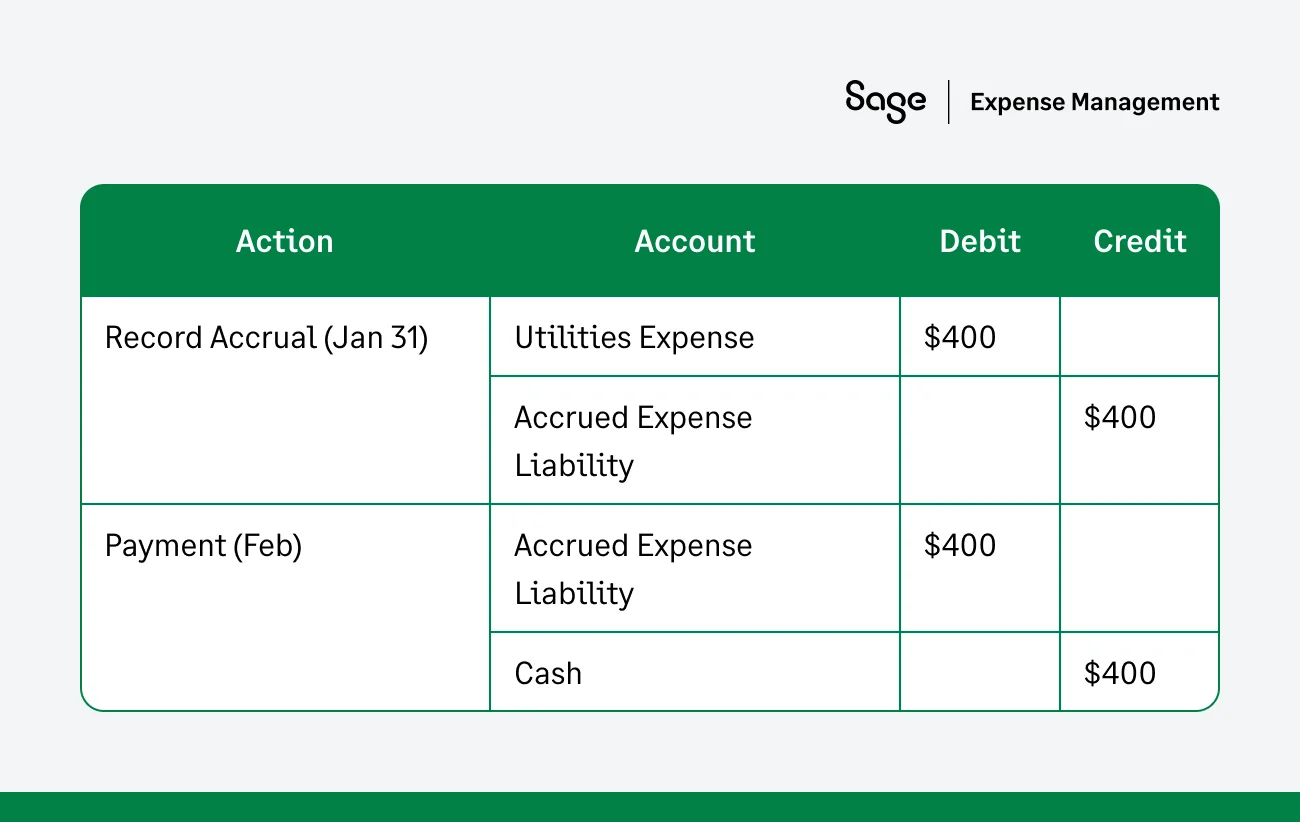

Utilities

Utility expenses should be recorded in the month they are used. January’s electricity bill, even if paid in February, is recognized in January because that is when the resource was consumed to keep the business running.

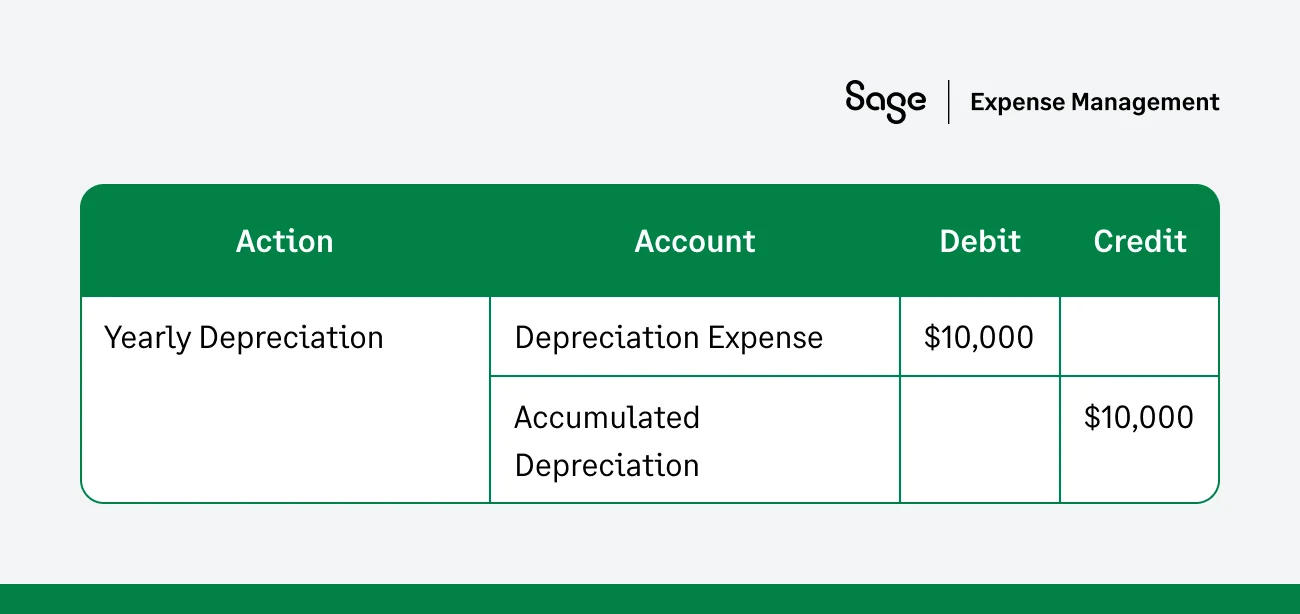

Depreciation Expenses

If a company buys a $50,000 machine that lasts 5 years, they recognize $10,000 as a depreciation expense each year. This expense allocation aligns with the revenue the machine generates over time, reflecting the gradual wearing out of the asset.

Marketing and Advertising

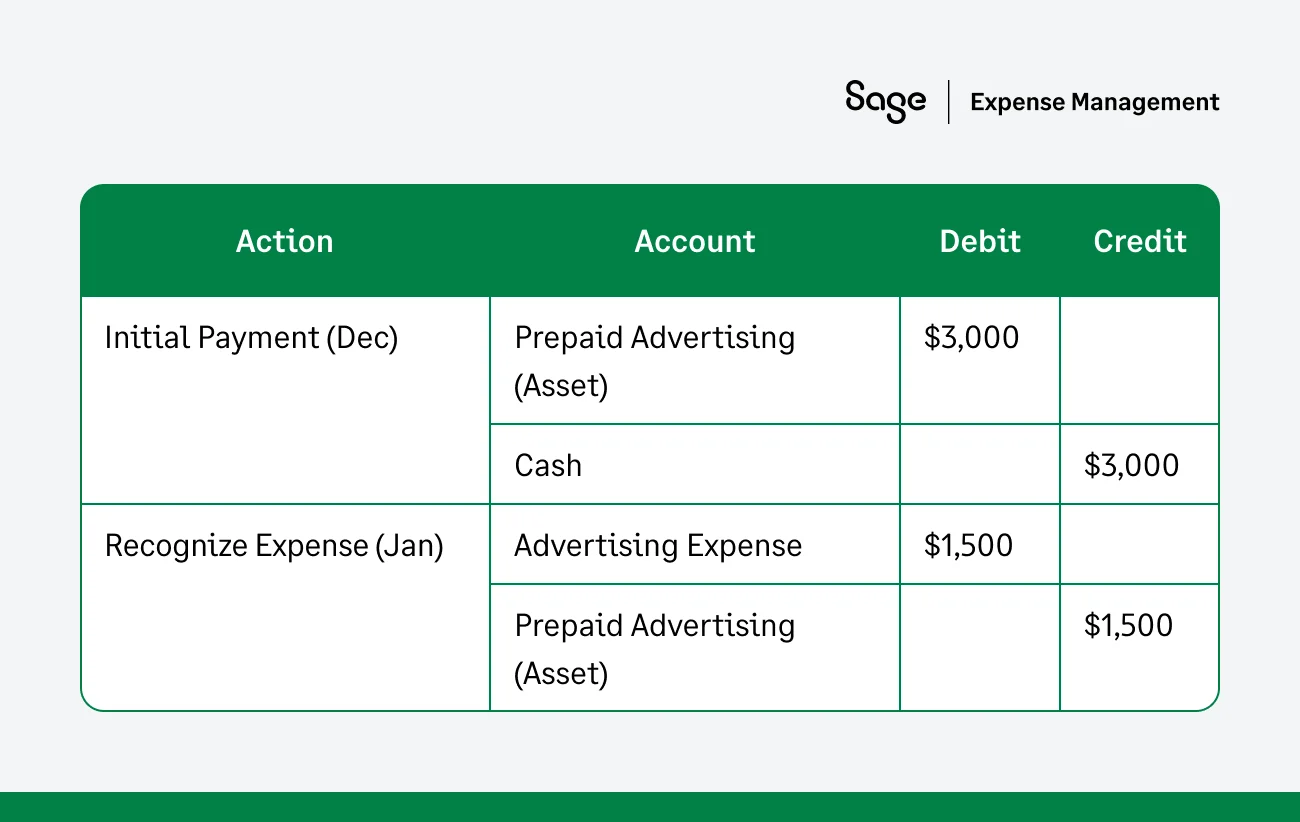

An advertising campaign run in December might be designed to drive sales during a January peak. By allocating the cost to the months where the sales actually happen, you get a clear view of your actual profit margins.

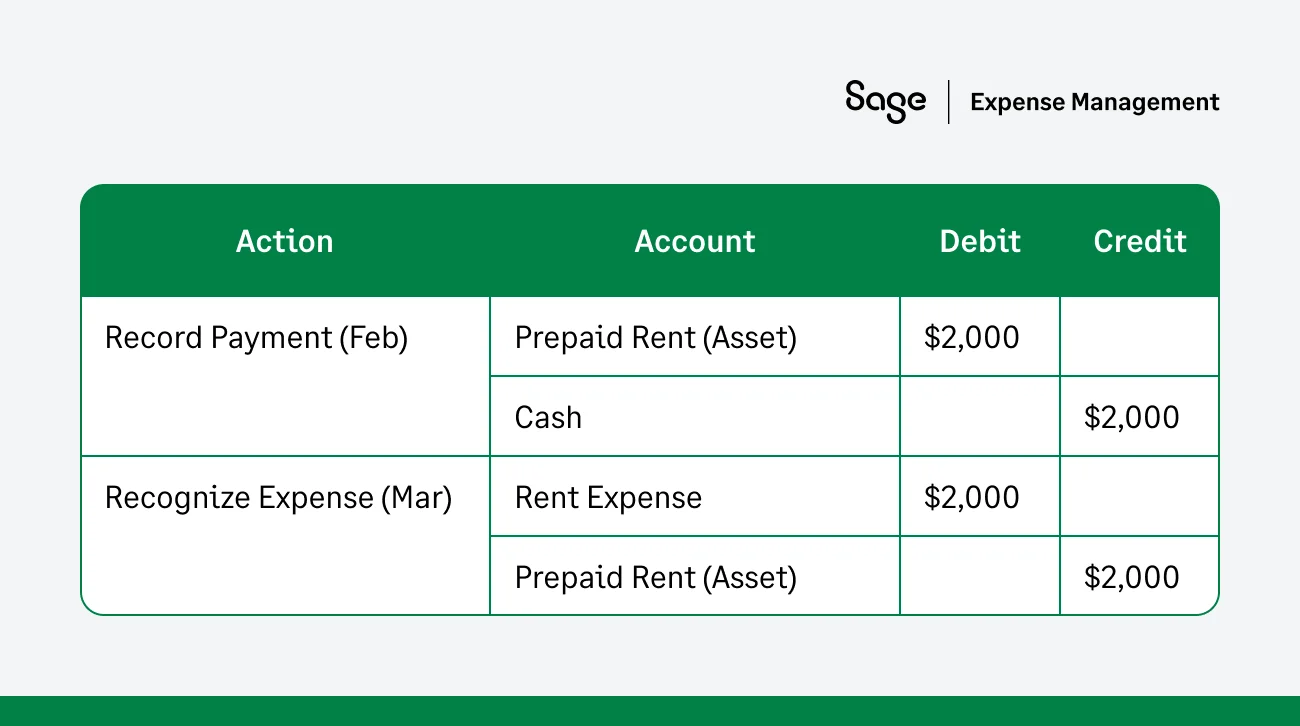

Rent Expenses

If you pay March rent in late February, you are essentially holding an asset - the right to use that space in the future. The expense only becomes "real" on the income statement once March actually begins.

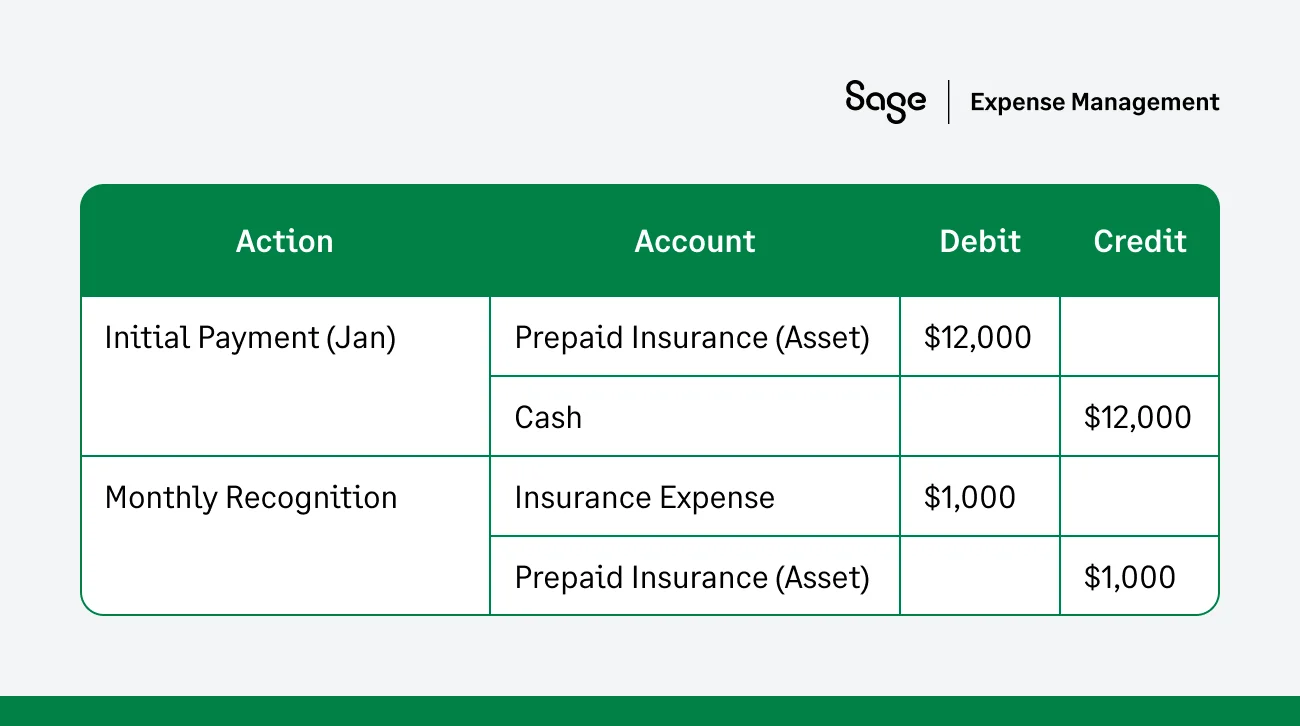

Insurance Premiums

Let’s say you pay $12,000 in January for a 12-month insurance policy. Instead of recording the full amount in January, you recognize $1,000 per month to ensure one large payment doesn't skew your monthly profitability reports.

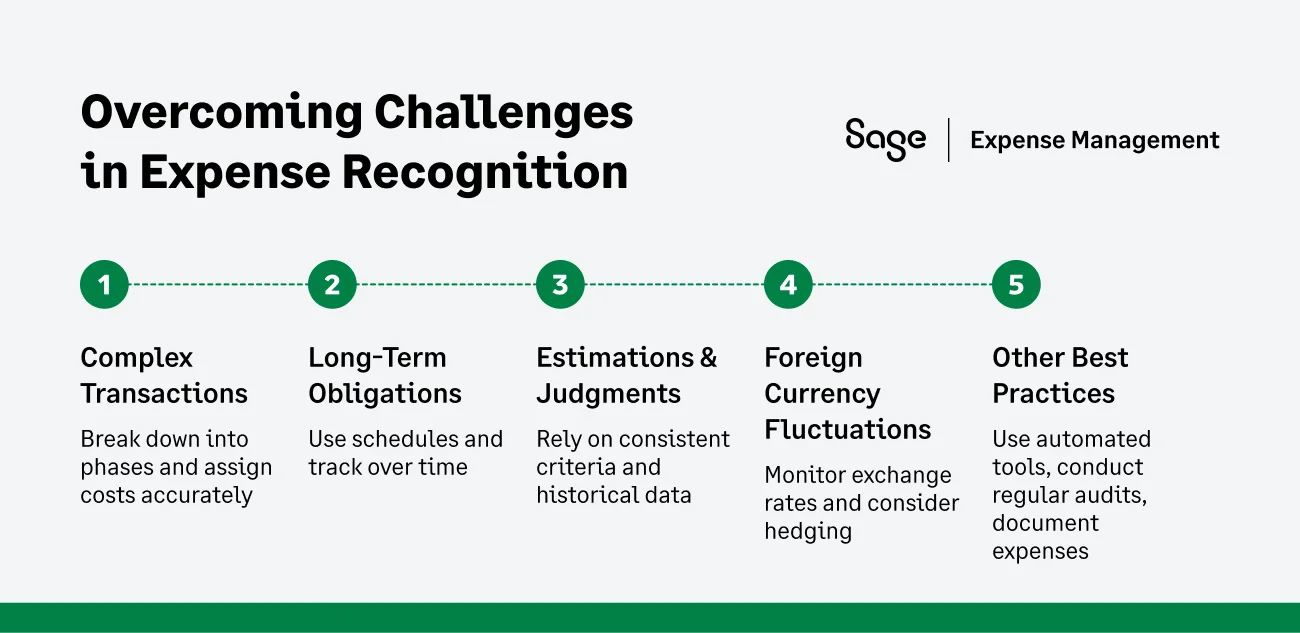

Challenges in Expense Recognition

While the theory is simple, the execution can be complex, particularly for companies dealing with multi-period projects or international operations.

Estimations and Judgments

Businesses often have to make estimations for uncertain future obligations, such as warranty claims. This reliance on judgment makes it crucial for businesses to have clear, documented policies to ensure consistency.

Foreign Currency and Exchange Rate Variability

For companies dealing with international expenses, changes in exchange rates between the time an obligation is incurred and when it is paid can lead to variances in expense recognition.

Revenue and Expense Misalignment in Seasonal Businesses

A seasonal business may incur significant costs (like hiring or inventory) in low-revenue periods to prepare for high-revenue seasons. Recognizing these expenses only when paid can misinterpret financial performance.

Complexity of Transactions

Long-term construction or software implementation projects involve various phases, making it difficult to allocate costs to a single period.

How to Overcome These Challenges and Ensure Expense Compliance

Effectively applying the expense recognition principle requires strategies that reduce human error and maintain a clear audit trail.

Protecting your financial integrity requires moving away from manual work and toward automated precision.

- Utilize automated solutions: Software like Sage Expense Management can automate the pro-rating of long-term costs, significantly reducing human error.

- Adopt accrual-at-source: Capture the date of purchase via a digital receipt the second it happens. This ensures the date of service, not the date of payment, is the primary record.

- Implement multi-level approvals: Use automated workflows to route expenses through multiple reviews, ensuring correct categorization before they hit the general ledger.

- Use object codes for clarity: Establish a clear system for mapping assets (e.g., Code 0540 for Prepaids) vs. liabilities (e.g., Code 2191 for Accruals) to ensure the balance sheet is always audit-ready.

- Ongoing finance training: Ensure your team understands the distinction between Termination Costs (accrued only if notice is given) and Regular Payroll.

How to Avoid Misalignment of Revenues and Expenses

To ensure your costs and income stay in sync, consider these tactical shifts:

- Use accrual-at-source: Capture the date of service or purchase immediately via a receipt, not just the date the invoice is processed or paid.

- Shorten the monthly close: The faster you close your books, the less likely expenses will leak into the wrong month.

- Use amortization schedules: For any expense over a certain threshold (e.g., $5,000), automatically create a schedule to spread the cost over its useful life.

How Sage Expense Management Can Simplify Expense Reporting

Sage Expense Management provides a comprehensive suite of tools designed to streamline the recognition process and ensure compliance with the expense recognition principle.

- Effortless Receipt Tracking: Users can submit receipts through Text, Gmail, Outlook, or Slack. It extracts, codes, and tracks expense data in real-time, ensuring the date of the expense is captured accurately for matching.

- Real-Time Credit Card Expense Tracking: Users are notified of business card spend via text in real-time. This allows finance teams to see liabilities as they happen, rather than waiting for a bank statement at month-end.

- AI-Powered Compliance: Sage’s AI checks if expenses align with preset business rules before submission, flagging potential fraud or misclassifications automatically.

- Seamless Sync with Accounting Software: SEM’s accounting integrations with QuickBooks Online, Xero, Sage Intacct, and NetSuite, ensure fully coded expense data syncs automatically to your general ledger.

In Conclusion

The expense recognition principle is vital for accurate financial reporting, helping businesses align expenses with revenue for a clear view of profitability. By following this principle, companies can maintain transparency, support growth, and comply with regulatory standards.

Tools like Sage Expense Management simplify this process by automating tracking and ensuring every dollar spent is matched to the right period, making your financial management consistent and accurate.

{{streamline-expense-tracking="/cta-banners"}}